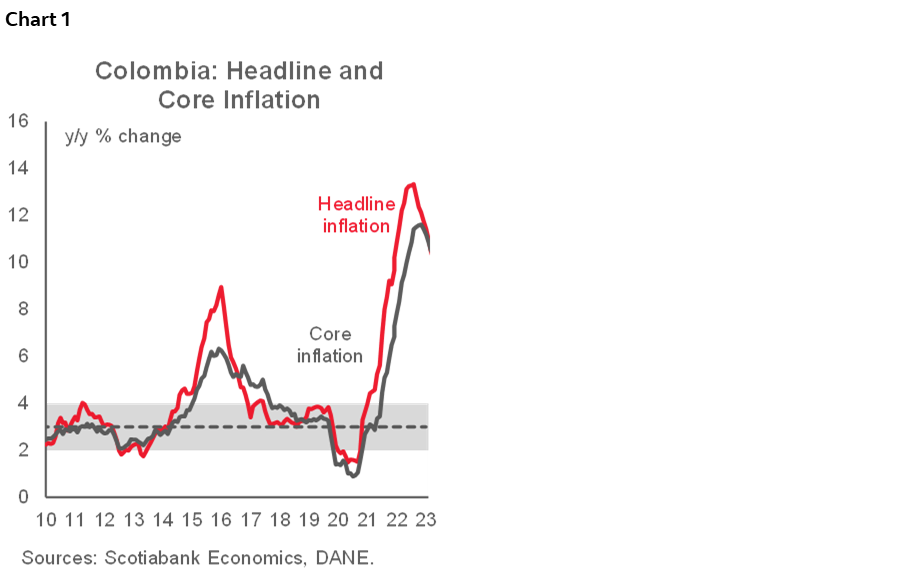

- Headline inflation fell to single digits for the first time since mid-2022. Food prices were the main source of disinflation in 2023.

Monthly CPI inflation in Colombia stood at 0.45% m/m in December, according to DANE data released on Tuesday. The result was below economists’ expectations of 0.64% m/m in the latest BanRep survey, but it was closer to our forecast of 0.47 % m/m. Year-on-year headline inflation declined for the eight month in a row, from 10.15% in November to 9.28% in December (chart 1), returning to single digits for the first time since June 2022.

Core inflation (ex-food) decreased from 10.61% y/y in November to 10.33% in December, while inflation excluding food and energy prices stood at 8.81% y/y. Core inflation metrics are reflecting a disinflation trend, especially in durable goods where the 16.10% y/y recorded in Dec 2022 turned into a 3.24% y/y record in Dec 2023. This could be attributed to the COP’s appreciation and weaker domestic demand. In the case of services inflation, we observed an acceleration from 7.35% in late-2022 to 9.33% in late-2023 as a result of indexation effects in labour-intensive services. Still, overall core inflation will continue decreasing in 2024 as indexation effects will be more moderate than in 2023.

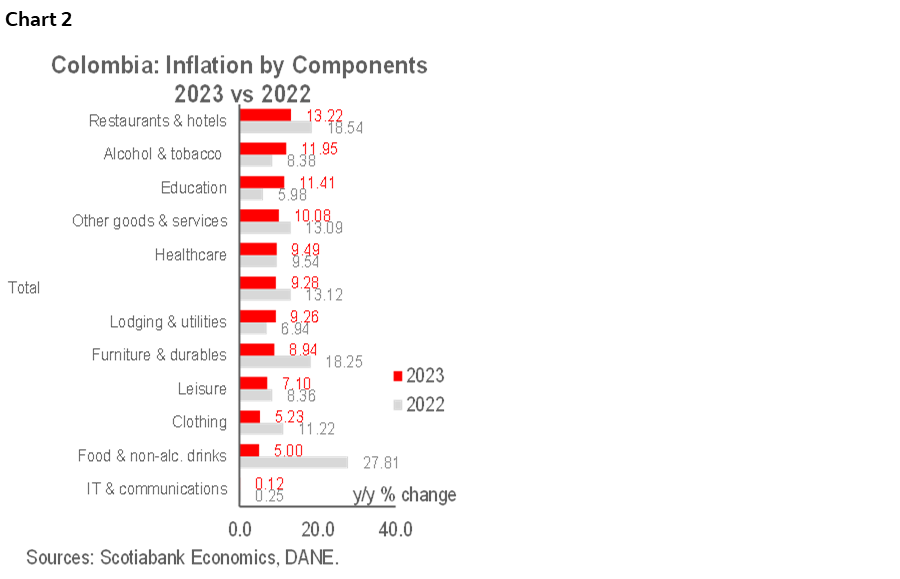

In 2023, three groups accounted for 66% of headline inflation: Housing and utilities contributed 2.84 ppts, Transport added +1.96 ppts, and Restaurant and Hotels contributed 1.38 ppts. In 2023, seven out of the twelve inflation groups decelerated (chart 2), but the main source of disinflation was food: its contribution to headline inflation was 0.99 ppts in 2023 (5,0% y/y), well below its 33% share of 2022 inflation (4.88 ppts recording 27.81% y/y). On the other hand, Housing & Utilities and Transport groups accelerated versus 2022. Housing reflected high indexation effects but also a spike in utility fees, while in the transport group, the increase of more than 50% y/y in gasoline prices contributed the most. We expect indexation effects to decelerate in 2024 due to lower minimum wage increment (+12% in 2024 vs +16% in 2023) and lower year end inflation in December 2023 (9.28% y/y) versus 2022 (13.12% y/y), which is a relevant reference for setting rent fees. Therefore, we think annual inflation will decelerate further, especially during the first half of the year.

All in all, 2023 inflation reflected mixed effects, a disinflationary contribution from good-related items, not only food but also tradable goods. On the other hand, services inflation remained sticky, reflecting indexation effects.

We think that reaching the single-digit mark again is good news for the central bank, and it maintains a potential rate cut between 25 and 50 bps on the cards. The next BanRep meeting will be on Wednesday, January 31st. We expect the central bank to continue the easing cycle probably at a moderate pace; however, as stressed before, we do expect inflation will continue going down at a faster pace, especially in the 1Q-2024 amid significant statistical base effects in food inflation, but also because of lower indexation compared with 2023. In that sense, we think the central bank could speed up the easing cycle between March and June since, by this period, inflation could go below the 7% mark. Economic activity numbers also affirm the base case scenario for BanRep continuing the easing cycle in 2024. We expect the monetary policy rate to close in 2024 at 7%.

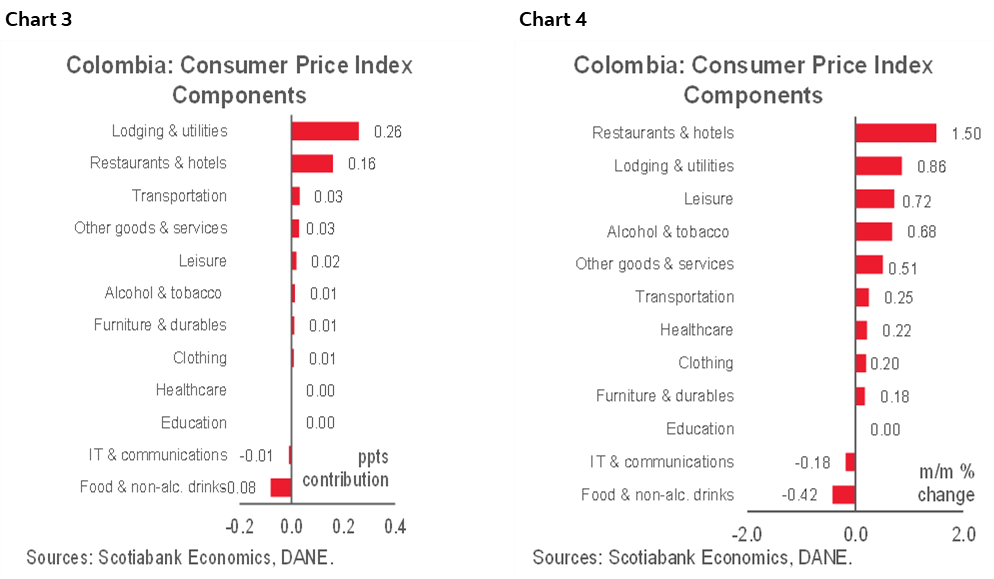

Looking at the December figures in detail, food inflation is the group that applied the greatest downside pressure on inflation during the month (charts 3 and 4).

OTHER HIGHLIGHTS:

- The lodging and utilities group was the main contributor to monthly inflation. The group recorded +0.86% m/m inflation and +26 bps contribution. Rent fees continued reflecting the impact of indexation, while in terms of utilities, electricity fees increased moderately. In 2024, rent fees will be allowed to increase up to 9.28% y/y, which is a significantly lower indexation versus 2024 (13.12% y/y), we anticipate this phenomenon to be one of the main source of disinflation in 2024.

- The second main monthly contributor was restaurants and hotels (+1.50% m/m with a contribution of 16 bps), reflecting the usual year-end high demand for those services. However, it is worth noting that in 2023, this group was the third main contributor to headline inflation, and one reason for that was indexation to the minimum wage increase. This indexation will continue in 2024. However, it will be lower compared with what we observed in 2023.

- Food recorded a -0.42% m/m inflation and subtracted to the headline eight bps. Food inflation posted an atypical behavior given the holiday season. However, some price correction is fueled by the lower FX. During 2023, we saw some normalization in some food prices. The most significant deceleration was in products such as milk, fruits, meat, and chicken.

- Regarding price reductions (negative inflation), the leading products were bananas, onions, cooking oil, and potatoes. All the previous products have something in common: they need imported inputs for their production, or in fact, some are imported. In that sense, normalization in international food prices, fertilizers, and lower effects are helping to see significant disinflationary pressure. In 2024, we expect food inflation to normalize to the average inflation, which, in any case, will help to reduce headline annual inflation in the first quarter amid significantly high statistical base effects, while in the second half of 2024, the contribution to the disinflation will be moderate.

- Tradable goods are expected to contribute to disinflation in 2024. Durable goods inflation closed the year at 3.24% y/y, decelerating from the maximum recorded in March 2023 of 16.76% y/y. Weaker domestic demand and significant FX appreciation are pushing down some key prices, especially vehicles, and we expect part of this effect to continue in 2024. On the other side, services inflation has decreased moderately to 9.33% y/y in December from its peak of 9.51% in September 2023; part of this behaviour is explained by still decent demand for “lower-ticket services,” which allows indexation effects to transmit in final prices. Despite this indexation will continue in 2024, we expect this pressure to be more moderate compared with 2023.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.