ON DECK FOR TUESDAY, FEBRUARY 7

KEY POINTS:

- Markets await Fed's Powell

- A$ leads the pack...

- ...after the RBA hikes and guides more to come

- BoC Governor Macklem to speak...

- ...during protracted pause...

- ...and ahead of inaugural 'minutes'

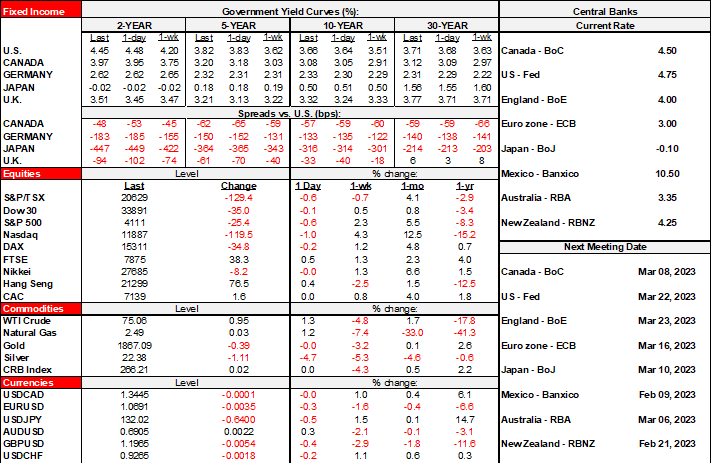

The main overnight development was the RBA’s hawkish stance. That drove a sharp cheapening across shorter term Australian government bonds and A$ appreciation. They hiked 25bps as generally expected, but left the door open to more hikes instead of providing pause guidance that would have built upon December’s signal. Stronger than expected Q4 and December inflation reports and the China rebound narrative likely drove some of the stance, while the RBA emphasized it is closely watching wages.

There are two main developments on deck for today.

1. Fed Chair Powell: He will be interviewed before the Economic Club of Washington starting at 12pmET. How did nonfarm affect his thinking including revisions? What did he think of market conditions during and immediately after his press conference? Since nonfarm? I don’t think he’ll be all that aggressive and do a full 180 from his soft performance during the press conference and given the magnitude of the market moves since payrolls. For one thing, fed funds futures are now priced closer to 5.25% as per the December dots. If he says he’d lean toward taking the terminal rate higher in the March dots than what they had in December, then that would be incrementally hawkish. Boston did so yesterday, while Daly on Friday said she thought December’s dots were still valid. I suspect Powell is likely to say that payrolls was just one report and to repeat that they will get another payrolls and a couple of inflation prints before their next decision.

2. BoC Governor Macklem speaks about ‘how monetary policy works” in Quebec City. It has a primer feeling to it with emphasis upon uncertain lags. Text will be available by 12:30pmET and then there will be a press conference at 2pmET. The BoC releases its inaugural ‘summary of deliberations’ tomorrow and so Macklem might front-run them somewhat given it is a first for them. I wouldn’t go into it thinking this will be the BoC’s version of detailed minutes that will be highly revealing. It’s more of a PR exercise at the behest of the IMF. The BoC has sent a clear message they are on hold for some time now as multiple rounds of data are evaluated and so I’m not expecting much from him on rates. At some point they will have to address QT from a pace standpoint but it’s likely too soon.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.