ON DECK FOR THURSDAY, JULY 11

KEY POINTS:

- Markets on tenterhooks ahead of US inflation

- US core inflation might reaccelerate

- UK macro beats drive slight gilts underperformance

US core CPI inflation will clearly dominate market attention today. Overnight developments were light and included solid beats by UK macro readings as GDP grew by 0.4% m/m, doubling consensus and thanks to services which pushed yields on gilts very slightly higher than elsewhere. Meh. The global market tone hangs on CPI.

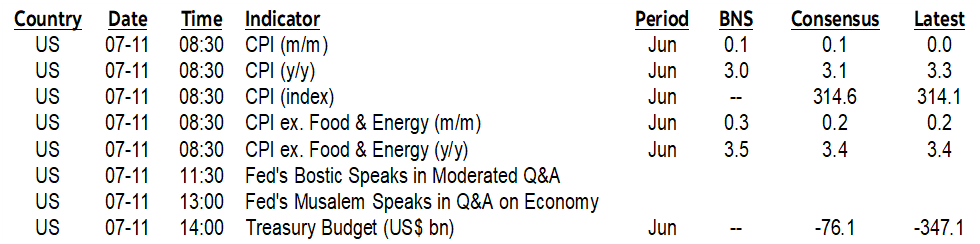

US Core CPI Expectations

US CPI for the month of June will be released at 8:30amET. Was the prior month’s sudden deceleration of core CPI to 0.16% m/m SA anomalous and poised for a rebound that could thwart rate cut prospects? Or the start of something beautiful that could pave the way to rate cuts? On its own, today's reading is unlikely to do either, but market volatility is all but assured. This is one of three CPI readings and two more PCE readings before the FOMC’s September 18th decision.

Estimates vary. Out of 70 forecasters (yes 70!), four think that core could land at 0.1% m/m SA, 12 of us are in the 0.3% camp including Scotia, and 54 are in the 0.2% bucket. I maintain that the sample is far too large.

There is a lot of uncertainty, but I like the reasoning behind why I went higher than others.

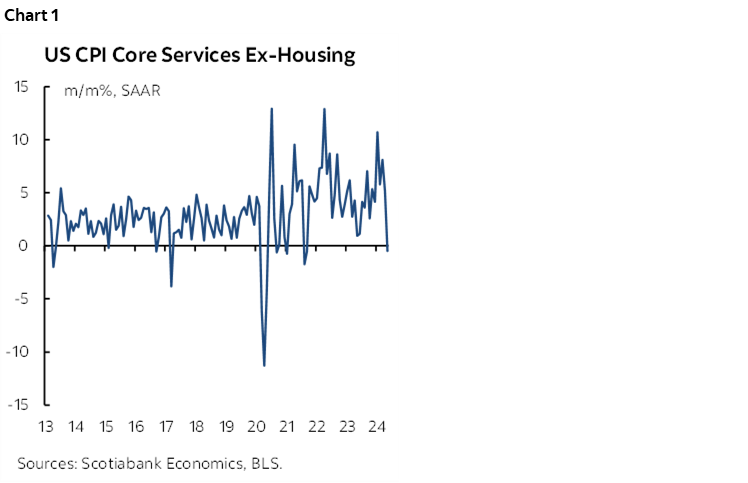

For starters, the prior month’s sudden deceleration was partly driven by the sudden collapse of core services inflation (CPI-services ex-energy services and ex-shelter) as shown in chart 1. Core services represent about one-quarter of the CPI basket and nearly one-third of the core CPI basket. There are two reasons why this might rebound.

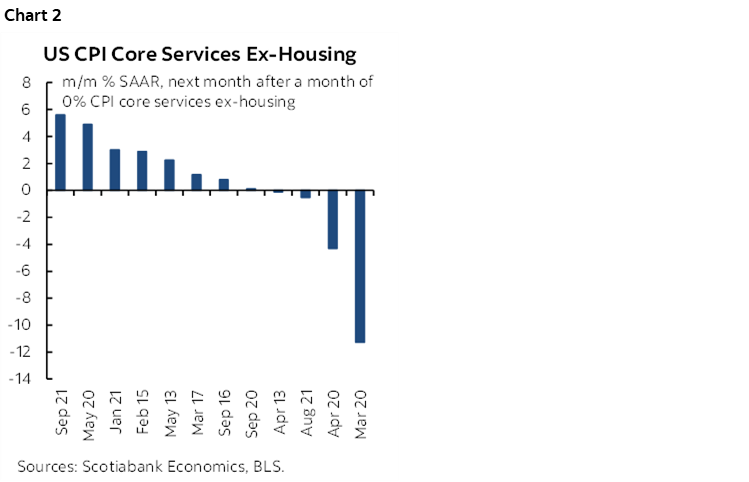

One is a statistical observation drawn from what has happened in the past that observes rebounds following sudden decelerations by a usually high and sticky measure with the only material exceptions being at the very start of the pandemic (chart 2).

The more substantive point is that sticky wage growth may motivate a rebound in core services prices because wages are a big cost component behind their delivery. Think car repairs, hair cuts, bar and restaurant tabs etc.

The second key is that shelter costs represent about 36% of the CPI index and 45% of core CPI. I expect shelter costs to continue to grow at around a 0.4–0.5% m/m SA pace.

So, all totalled, we have about 60% of the CPI basket and about three-quarters of the core CPI basket that could come on quite strong through core services and shelter.

In addition to the uncertainty around these estimates is the limited ability to track other components. Vehicle prices should be a minor influence. Gasoline prices could knock a tenth or so off of m/m headline CPI. Food prices will probably be a benign influence. Core goods inflation was flat the month before after prior declines and is an added risk today. For more on the estimates and reasoning see my Global Week Ahead article.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.