ON DECK FOR TUESDAY, JULY 23

KEY POINTS:

- Markets are just passing time until the week’s key risks

- Kamala Harris could be much worse for markets…

- …than either Trump or Biden

- US earnings, home sales, Richmond on tap

- Turkey’s central bank remains hawkish

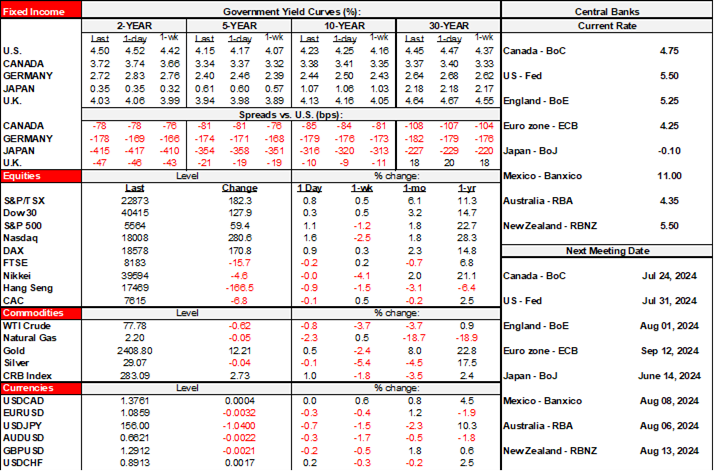

There is nothing consequential by way of fresh macro developments this morning. The back half of the week will spice it up with the BoC tomorrow and then US data arrives for GDP and the Fed’s preferred inflation readings.

The main focus will be upon US earnings with UPS, GM, GE etc in the pre-market and then Alphabet and Tesla in the after-market.

The US releases existing home sales for June (10amET) and the Richmond Fed’s manufacturing index for July (10amET).

The Central Bank of Turkey held its one-week repo rate unchanged at 50% as widely expected and the hawkish sounding statement emphasized several factors that “keep inflationary pressures alive.”

The Risks that Kamala Harris Poses

We know many of the risks that Donald Trump poses. But what does Kamala Harris stand for in terms of considerations that could impact markets and the economy? With the caveat that the Harris of today may be different than the one who was campaigning for Democratic presidential candidate in 2019, a patchwork of what she supported then and has supported since then points to some fairly extreme views aligned with the further left voices within the Dems. Her positions make her highly vulnerable in some key swing states. She will either need to clarify her stances in a rashly conceived election platform, or she will be pushed into doing so on the fly in debates and on the campaign trail. This is an unfortunate downside to her uncontested coronation given the late timing of Biden’s withdrawal. Overall, I’m of the view that several of her key policy stances are governed more by the heart than the mind. If I’m wrong with this assessment, then she needs to speak up and articulate a different plan soon.

Taxes:

- In her 2020 campaign, Harris said she would fully repeal the TCJA’s corporate tax rate cut from 35% to 21% by putting it back up to 35%. Her present stance is unclear but must be clarified as it would be highly destabilizing to markets.

- It’s unclear if she supports Biden’s proposal to deal with expiring TCJA provisions by ending some, but not hiking taxes on people making <$400k/year.

- Harris consistently supports higher taxes on upper income earners and a tax credit for lower income earners.

- In her 2020 campaign, Harris advocated taxes on stock (0.2%) and bond (0.1%) trades and a smaller tax on derivatives. The usual criticisms against a form of Tobin tax apply, not least of which being difficulties implementing one and pushing activity offshore. Here too her stance must be clarified or she risks only appealing to the far left.

- She has favoured raising estate taxes.

- Supports tax credits for renters and parents.

- She supports higher taxes for fossil fuel companies and pharma cos.

Climate:

- When she was a presidential candidate, Harris supported an eye-watering US$10 trillion climate plan that was multiples larger than Biden’s plan. How to pay for it and the macroeconomic consequences for considerations like inflation and markets were not addressed which is fairly typical of the most impractical and widest-eyed voices within the ESG crowd.

- She advocated a climate pollution fee and ending federal subsidies for fossil fuels.

- She was a key sponsor of a Green New Deal designed to achieve full reliance on ‘clean’ energy in ten years.

- She has previously proposed a ban on fracking.

- She appears to have since rescinded her support for a fracking ban and a costly Green New Deal but that may require clarification and these stances show her policy bias.

Trade:

- Harris opposes Trump’s tariff proposals. That’s the good news.

- The bad news? Unfortunately, she has a track record of opposing trade deals because of loosely defined ‘progressive’ considerations.

- She opposed the CUSMA/USMCA agreement when she was just one of 10 Senators who voted against it on environmental grounds. This could be a risk in upcoming negotiations. Canadians are gushing over her connections to the country, but her stance on trade agreements could well make her no friend to Canada.

- Harris also opposed Obama’s Trans-Pacific Partnership and once again because of concern about insufficient environmental and labour regs. Biden supported it, Trump killed it.

Geopolitical risk:

- Harris called for an immediate ceasefire in Israel earlier this year versus Biden’s support. She could be an unreliable ally to Israel.

- She backs unwavering US support for Ukraine.

Tuition and student debt:

- She supports forgiving student debt.

- In the past she has supported free college tuition.

Immigration:

- Harris advocates restrictions at the Mexico border. She supported Biden’s bipartisan border security deal that Trump led opposition against for purely political reasons. She is supportive of citizenship for immigrants in the US including so-called Dreamers. She is viewed as supportive of liberal immigration goals.

Health Care:

- Supported a “medicare for all” bill.

- Wishes to expand the child tax credit

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.