ON DECK FOR MONDAY, MAY 27

KEY POINTS:

- Quiet markets with the US and UK on holiday

- BoJ officials jawbone imaginary progress…

- …perhaps because the alternative would torpedo the yen

- German business confidence is stable

- Canada quiet with an empty calendar, absent foreign participants

- The Top Five things to watch on the Global Week Ahead calendar…

- …with most of the macro risk focused upon Friday…

- ...when Canadian GDP, US core PCE, EZ CPI and China PMIs arrive

It’s a very quiet start to the week. The US is out for Memorial Day, the UK is out for another bank holiday and there are only minor macro developments mainly focused upon BoJ comments. Canadian markets will be quiet with nothing on the domestic calendar and with major foreign buyers out. I’ll highlight the week’s main macro expectations.

Comments from the Bank of Japan mildly reinforced sentiment toward further BoJ hikes this year despite the lack of a convincing case for doing so. DepGov Uchida said “the end of our battle is in sight” in reference to getting inflation expectations durably set at 2%. That—along with indirect comments by Governor Ueda—was taken as a further signal in favour of additional policy rate hikes this year. Markets have about 30bps of additional hikes priced by year-end.

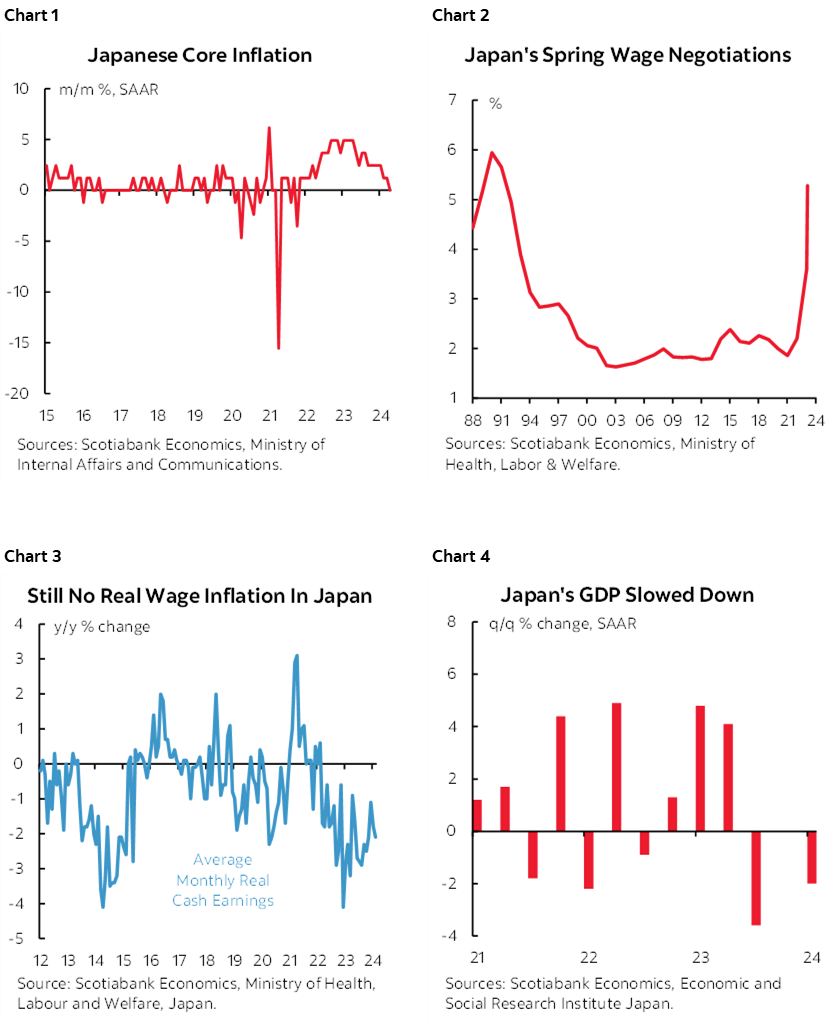

While year-over-year Japanese inflation is still over 2% it has been falling since the start of last year. That’s because month-over-month pressures on core inflation have waned and have hit 0% m/m SAAR in each of the past couple of months (chart 1). Further, Japan’s Shunto wage negotiations that struck strong gains last year and this year (chart 2) have yet to turn around falling real wages (chart 3) partly because those negotiations affect less then one-in-five Japanese workers. Japan’s economy is shrinking as evidenced by a 3.6% q/q SAAR decline in 2023Q3, a flat reading in Q4, and another 2% drop in 2024Q1 (chart 4).

So why are the BoJ officials seemingly whistling by the graveyard? Maybe because to do anything other than speak of hikes would further destabilize the yen that has depreciated from about 141 at the start of this year to about 157 now, bringing out government intervention around the end of April.

Other overnight developments only included German IFO business confidence during May that held unchanged as a slight downtick in the current assessment was offset by a slight gain in the expectations component.

There are no Canadian releases on tap today. Local market drivers this week will include bank earnings starting tomorrow with BNS and with GDP updates for Q1, March and the preliminary April reading on tap this Friday.

THE WEEK’S TOP FIVE DEVELOPMENTS

There is no Global Week Ahead article this week as I was away last week, but here are the key developments to watch out for this week.

Canadian GDP—Blowing the BoC’s Narrative?

GDP figures on Friday will be the final significant releases ahead of the BoC decision one week from Wednesday. Q1 GDP is widely expected to land somewhere between about 2% and 2½% q/q SAAR. There is significant uncertainty in both directions given that key components like parts of the services sector and inventory contributions are difficult to estimate in the absence of enough data. The BoC’s April MPR had forecast Q1 at 2.8% q/q SAAR which was a major upgrade from its view in the January MPR when they forecast basically no growth (0.5% q/q SAAR).

More important than Q1 could be the estimate for March GDP relative to Statcan guidance on April 30th that it was “essentially unchanged,” plus the advance ‘flash’ estimate for April. I wouldn’t be surprised to see a slight dip in March GDP. April GDP could get a solid lift from drivers like a large 0.8% m/m SA jump in hours worked after the prior -0.3% drop, given that GDP is hours times labour productivity. Tracking also points to gains in retail and manufacturing sales volumes but a slight slip in housing starts during April. Overall, I wouldn’t be surprised to see April’s preliminary estimate land at a similar rate to the 0.4% gain in February that itself was the hottest print since May of last year.

If so, then Q2 GDP could have a running head start with over 1% q/q SAAR growth baked in just based on the Q1 average and April estimate while assuming no change in May and June solely in order to focus the math on the effects of what may be known come Friday. So, after Q4 surprised the BoC by about a percentage point higher than they had forecast and if Q1 is around 2–2.5% and Q2 has a running head start, then these are material upside surprises to the BoC’s more dovish narrative earlier in the year that H1 would be peak pain for the Canadian economy.

Eurozone CPI—The Last One before the June ECB

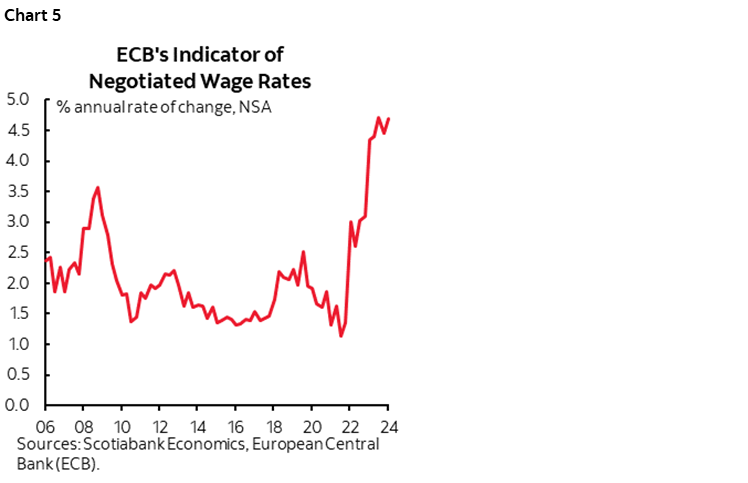

The last inflation print before the June 6th ECB decision lands on Friday and it would probably take a big surprise to knock them off course from a largely priced cut. Consensus is expecting a reading around 0.2% m/m NSA that would keep the y/y rate floating around 2½% y/y and with core at about 2.7%. What’s more likely is that any surprise in either direction could impact pricing beyond the June meeting. Last week’s negotiated wage figure of 4.7% q/q at an annualized but seasonally unadjusted rate (chart 5) kept the figures toward the high end of the recent range and leans toward a very cautious path after next week if they do indeed decide to cut.

US PCE Inflation—Will it Follow Core CPI?

PCE inflation for April arrives on Friday and the key question is the degree to which the Fed’s preferred inflation gauge will follow CPI that was released on May 15th. Recall that CPI was up by 0.3% m/m SA with core CPI up 0.3%. Consensus is split between 0.2% and 0.3% m/m SA for core PCE. 0.2 could reinforce pricing for rate cuts this year, while 0.3% could push against such pricing.

The Q2 Canadian Bank Earnings Season

My employer BNS kicks off Q2 earnings releases tomorrow and will be followed by BMO and National Bank the next day, then RBC and CIBC on Thursday with Laurentian and Canadian Western Bank following on Friday. TD had already released last week and faced idiosyncratic challenges but the bank earnings season begins in earnest tomorrow.

China PMIs—Still Signalling Modest Growth?

Thursday evening (ET, Friday in China) will bring out the May readings for the state’s purchasing managers indices. They are expected to continue to showcase modest growth.

There are quite a few other global macro reports out this week that will be previewed and recapped in daily notes, but these are the main developments.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.