- Chile: Central Bank confirms additional hikes in the MPR; We expect benchmark rate in the range 5.25–5.50% by March 2022

- Colombia: Ministry of Finance estimates lower fiscal deficit in 2021 due to better economic growth

CHILE: CENTRAL BANK CONFIRMS ADDITIONAL HIKES IN THE MPR; WE EXPECT BENCHMARK RATE IN THE RANGE 5.25–5.50% BY MARCH 2022

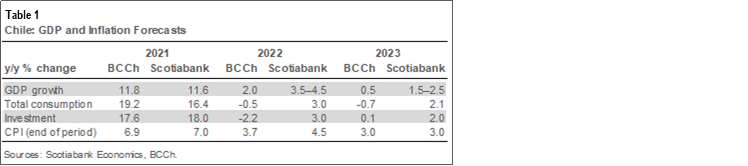

On Wednesday, December 15, the central bank (BCCh) released its quarterly Monetary Policy Report, which included updated forecasts for key macroeconomic indicators. In its Report, the central bank anticipates a GDP expansion of 11.8% for 2021 (range between 11.5% and 12%), in view of the strong performance of economic activity in recent months. For next year, the BCCh slightly increased its projection to 2.0% (range between 1.5% and 2.5%), which includes a contraction in both total investment and consumption. The BCCh’s baseline scenario is considering a technical recession in 2022, a view that we share in Scotiabank. According to the central bank, today’s level of economic activity is higher than the long-term level, which will imply a gradually deceleration in the GDP towards the end of the next year. Lastly, for 2023, the CB’s forecast was reduced by 1 percent point, to 0.5% (range between 0% and 1%) (table 1).

With regard to inflation, the central bank increased its forecast for the end of 2022, from 3.5% to 3.7%, below both the market and our expectations. The BCCh is expecting a deceleration in both core and non-core inflation since the second half of 2022, led by reversals in tourist packages and air-transportation fares. In our view, we could see those reversals during the first quarter of 2022, depending of the evolution of the Chilean peso (CLP). However, we keep our end of period inflation forecast for 2022 in 4.5%, due to a higher inflationary persistence than the estimated by the central bank.

The scenario described by the central bank considers new increases in the Monetary Policy Rate. According to different scenarios, the rate could increase by at least 100 basis points (bps) towards the second half of the next year. In a scenario with higher than estimated dynamism of consumption or investment, the rate could increase to 6.5% in the first half of 2022. As we commented in our Latam Flash earlier this week, we expect a 100 bps increase at the January meeting to reach a rate of 5.00% and another hike in March, of between 25–50 bps towards a rate of 5.25% or 5.50%.

—Jorge Selaive, Anibal Alarcón, & Waldo Riveras

COLOMBIA: MINISTRY OF FINANCE ESTIMATES LOWER FISCAL DEFICIT IN 2021 DUE TO BETTER ECONOMIC GROWTH

According to a local news agency, after a meeting with the Fiscal Rule Committee, the Ministry of Finance announced its new fiscal deficit estimation for 2021 at 7.6% of GDP, lower than the estimate in the earlier Medium-term fiscal framework (MTFF) in mid-June, which stood at 8.6% of GDP, and lower than the 2019 deficit (7.8% of GDP). The positive revision was made on the basis of better tax collection derived from a better-than-expected economic activity. It is worth noting that the Government revised up its forecast for economic growth in 2021 from 6% in MTFF-2021 to 8% and now to 9.7%.

In the same vein, the debt-to-GDP ratio is now calculated at 62.1% of GDP, 3pps lower than MTFF-2021 estimations, but still higher than the 2020 ratio of 60.4% of GDP. Either way, our take is positive and affirms the perspective of potential lower financing needs in 2022. Further information will be released early in 2022 in the Financing Plan. For now, we highlight that despite a challenging H1-2021 due to social protests amid a then-failed fiscal reform, we are now seeing some green shoots derived from the consolidation of economic recovery.

—Sergio Olarte & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.