- Chile: Central Bank raises policy rate by 25 bps (to 0.75%); We forecast one more hike by Q4-2021

CHILE: CENTRAL BANK RAISES POLICY RATE BY 25 BPS (TO 0.75%); WE FORECAST ONE MORE HIKE BY Q4-2021

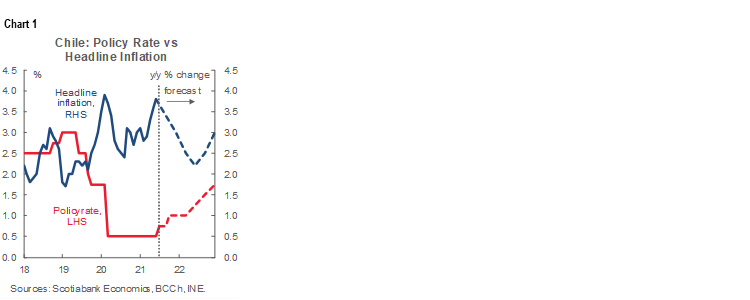

On Wednesday July 14, despite June’s surprise low inflationary record (0.1% effective versus 0.3% expected by the market), the Central Bank (BCCh) opted to start the normalization process earlier than anticipated, supported by a heterogeneous economic recovery and driven by private consumption, according to its monetary policy statement. In our opinion, although the process of raising the Monetary Policy Rate started earlier than we anticipated, we do not expect it to surpass our base scenario of 1.0% by December 2021 (chart 1). The next hike in the Monetary Policy Rate would occur at the October or December meetings. Taking this into account, we further expect the recent fall in bond rates to be accentuated.

In the local scenario, the BCCh reports GDP growth is being driven by greater consumption and commercial activity. We reinforce that this dynamism in consumption has been highly supported by the government’s fiscal supports and the added household liquidity allowed by pension withdrawals. Regarding employment, the central bank emphasized the recovery of formal salaried employment (a view that we share), which is an important measure of the normalization process. However, asymmetries remain, as labour participation remains subdued among a significant portion of the workforce consisting of the self-employed, informal workers and women.

In the external scenario, the BCCh slightly moderated its prospects for the world economy, recognizing the risk arising from the spread of new variants of Covid-19, as well as a significant lag in the advancement of the vaccination process in many emerging economies. The statement also highlighted that several central banks, mainly from commodities-exporter countries, have begun the process of normalizing their monetary policy.

We maintain our expectation of GDP expansion of 7.5% with an upward bias for 2021, but below the mid-range of the BCCh’s expectations (8.5 – 9.5%). Public spending would lose momentum towards the last quarter of this year, coinciding with an increase in precautionary savings for households, decreasing somewhat the strength of the dynamism of private consumption. This, in a context where the labour market (informal workers) will continue to have wide capacity gaps. In inflationary terms, we continue to expect inflation in 2021 to end at 3.5% y/y, yet another element that would contain aggressive increases in the Monetary Policy Rate during the second half of this year.

—Jorge Selaive, Anibal Alarcón, & Waldo Riveras

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.