- Peru: BCRP cuts rate for the sixth time, inflation under control

- Chile: January CPI increases 0.7% m/m (3.2% y/y)

- Mexico: Inflation accelerated for the third consecutive month owing to increasing food prices

PERU: BCRP CUTS RATE FOR THE SIXTH TIME, INFLATION UNDER CONTROL

The board of the Central Bank of Peru (BCRP) cut its key interest rate on Thursday, February 8th by 25bps, to 6.25%, in line with what was expected by market consensus, the Bloomberg median and our forecast at Scotiabank. In its statement, the BCRP emphasized that it forecasts that year-on-year inflation will continue its downtrend since the risks associated with climatic factors (El Niño) have been reduced. This view reduces the probability of any pause in the short term, although the BCRP was careful to keep that possibility open.

The BCRP highlighted that inflation is already at the upper limit of the target range (3%) and that core inflation (2.9%), as well as 12-month inflation expectations (2.6%), are within the target range (between 1% and 3%) for the second consecutive month. The statement reiterated that since June 2023, a more marked downward trend in inflation has been observed, as some of the transitory effects due to supply restrictions dissipate. The first inflation readings for February suggest that inflation would remain around the upper limit of the target range, after 32 months of remaining outside. At the risk level, the BCRP reiterated that risks associated with international conflicts remain and highlighted the adverse effects on fuel and freight prices.

The BCRP warned that the leading indicators showed mixed behaviour; while expectations about the economy recovered for the second consecutive month, although the majority remains in the pessimistic range. A recent BCRP survey reflects that the GDP growth forecast for 2024 stabilized for the third consecutive month, around 2.3%, reflecting a change in sentiment with respect to the downward trend observed in past surveys. The sea temperature anomaly continues to point to a weak El Niño scenario. In its statement, the BCRP stopped mentioning the risk associated with the lowering of China’s growth.

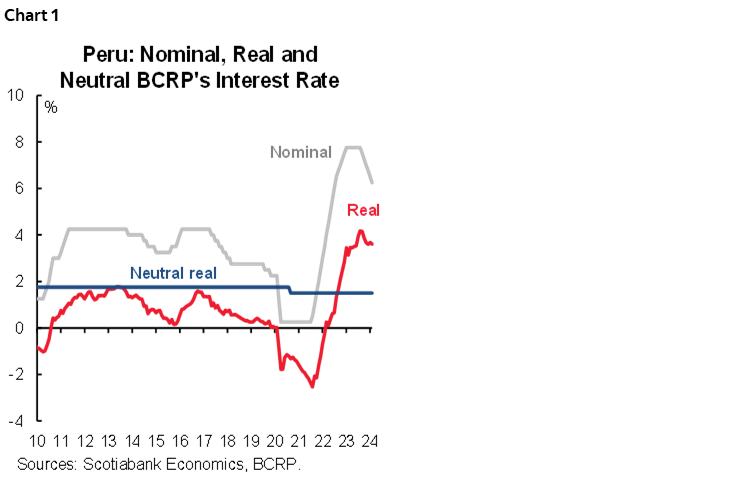

Despite the cut in the policy rate to 6.25%, the real interest rate went from 3.7% to 3.6% (chart 1), maintaining the restrictive stance of monetary policy, and still well above the neutral level (2.00%), accumulating 18 months of contractionary territory. The monetary policy stance was maintained by reaffirming that, “if necessary, it will consider additional modifications to monetary policy.” So far in 2024, monetary policy decisions are aligned with our vision, which is why we maintain our forecast of a 250bps cut throughout the year, up to 4.25%.

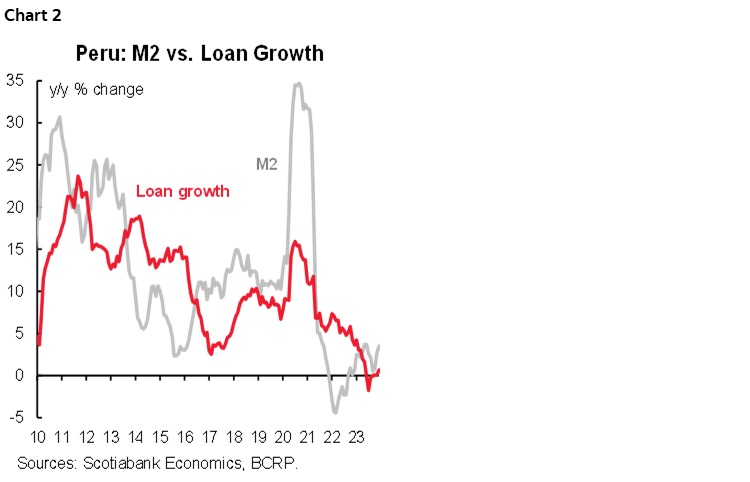

Our base case calls for recurring cuts of 25bps per meeting until Q4-24, when we expect a pause once the real rate approaches the neutral 2% level. The BCRP’s survey showed that the market continues to revise its key rate expectation downward for the year-end, going from 4.6% to 4.5%, getting closer to our forecast. Monetary conditions showed a more visible recovery in December. Liquidity accelerated its expansion (+1.9% y/y, for the second consecutive month in positive territory), with a slight acceleration in loans (from +0.1% to +0.7% y/y), see chart 2. Financial savings also showed an acceleration, for the seventh consecutive month, to 7.7% y/y. The unusual recent volatility of the FX market has prompted the BCRP to resume spot sales (US$ 125 million), not seen since October 2023.

—Mario Guerrero

CHILE: JANUARY CPI INCREASES 0.7% M/M (3.2% Y/Y)

- Despite the high CPI reading in January, the BCCh would arrive at the next meeting with inflation at or very close to the 3% target.

On Thursday, February 8th, the INE released January CPI, which rose 0.7% m/m, above what was expected in surveys (Economists Survey: 0.2%; Traders Survey: 0.3%), forwards and consensus (0.4%) and closer to our 0.5% m/m expectation. Although INE publishes a year-on-year variation of 3.8%, rather for index readjustment purposes, the accumulated inflation in the last 12 months with the new basket is only 3.2% y/y. Considering the above, the Board of the Central Bank (BCCh) would arrive at the April meeting with inflation at, or very close to, the 3% target. We reaffirm our expectation that the BCCh will quickly bring the benchmark rate to its neutral level, with a cut of no less than 100bps at the next meeting.

January’s CPI reveals an expected exchange rate pass-through of the recent peso depreciation, mainly on tradable products. Given the higher level of the exchange rate so far in February, we raise a note of caution on this month’s inflation, which could continue to reveal exchange rate pass-through on this type of product. Nevertheless, we estimate that the convergence of year-on-year inflation to the 3% target in March would not be compromised. We continue to consider that the exchange rate pass-through is limited given the weakness of domestic demand and an adequate level of inventories.

By divisions, January CPI was mainly explained by increases in the prices of food and non-alcoholic beverages (+1% m/m), among which chicken meat (+0.07 ppts), soft drinks (+0.04 ppts), tomatoes and avocados (+0.03 ppts respectively) stood out for their contribution. On the other hand, the transportation division showed a drop of 1.6% m/m, which was mainly explained by a reduction in international air transportation fares (-0.19 ppts).

—Aníbal Alarcón

MEXICO: INFLATION ACCELERATED FOR THE THIRD CONSECUTIVE MONTH OWING TO INCREASING FOOD PRICES

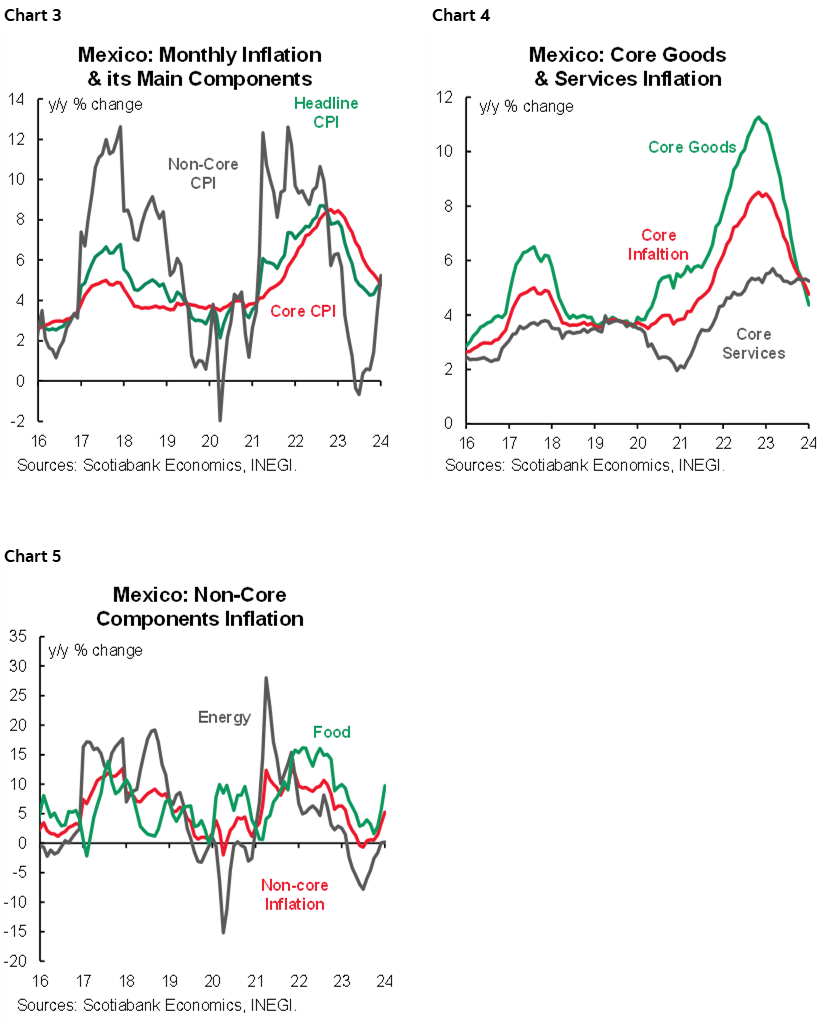

In January, headline inflation edged up to 4.88% y/y from 4.66% previously (4.85% consensus), as core inflation moderated to 4.76% y/y from 5.09% previously (4.73% consensus), derived from a slower pace in merchandise at 4.37% (4.89% previously), and services to 5.25% (5.33% previously). Non-core inflation rose 5.24% y/y from 3.39%. In its monthly comparison, headline inflation rose to 0.89% m/m (0.71% previous, 0.86% consensus), core inflation had a lower increase of 0.40% m/m (0.44% previously, 0.37% consensus), with a higher pace in merchandise. However, non-core inflation rose to 2.37% m/m (1.53% previously).

Non-core item (food and energy) have strongly rebounded from negative annual print in July 2023 to 5.23% in January, surpassing the core item pace and adverse climate events have become one the biggest risks for inflation in 2024, Banxico’s policy statement noticed. In this sense, this month, fruits and vegetables led the upsurge, reaching a 21.78% y/y increase (11.68% previously).

On the core side, stickiness remains, and it seems that the trend will not change in the short term, as demand for goods and services could put more pressure in prices in the upcoming months. We expect merchandises and services to remain sticky in the following months, with a very slow pace, and with some resistance from services as they stood above 5.0% for the last 18 months.

Looking ahead, we expect more setbacks in inflation during 2024, leading to a slower disinflation process. In line with the latest Citibanamex survey, year-end inflation consensus moved up to 4.11%, although with several possible scenarios as analyst responses are in a range of 3.50%–4.60%, signaling a still somewhat uncertain environment, which could lead to a slower pace of cuts, in case of adverse coming prices dynamics.

—Miguel Saldaña & Brian Pérez

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.