- Colombia: BanRep Survey—mixed inflation expectations, while consensus affirms expectations for a 75bps cut in September

Thin Asia trading with Japan and China closed for business followed by an uneventful European morning, with no data and few headlines, has given markets little to move on aside from FT and WSJ pieces calling for the Fed to start big this week. Fed cuts pricing for Wednesday’s meeting sits today 4bps higher at 38bps—or roughly a toss-up chance of a half-point cut—building on the late-week rally that followed a pair of speculative Fed dilemma articles (also from the WSJ and FT). There’s little on tap in the G10 to shake up global markets while in Latam we have the release of Colombian retail sales and industrial/manufacturing output data at 11ET.

Over the weekend, China released another set of disappointing macro figures, with retail sales missing in August at 2.1% vs 2.5% y/y expected while investment, industrial production, and unemployment rate figures also disappointed. The data led a couple of key US banks to downgrade their 2024 China growth projections to 4.7%, on track to miss the government’s 5% goal. With Chinese data weakness comes declines in key metals prices, as iron ore sheds 1.6% today and copper falls 0.3%, but oil holds up ~0.5%. All of Euro Stoxx and FTSE cash indices, and SPX/NDX futures are practically flat.

While the very front-end of the USD curve shows a 3/4bps bid, yield declines get smaller and smaller further out the curve, with 2s down 1.5bps and 30s unchanged; UK and European debt is flat to weaker. The lower US yields environment is supporting practically all major currencies against the dollar, with a 0.5% gain in the JPY a clear reflection (note that the cross fell below 140 this morning for the first time since July 2023). The MXN is lagging its key peers by virtue of being unchanged in the 19.20 area; note that on Sunday, Pres AMLO signed the judicial reform into law. Mexican markets are closed today for Independence Day.

Peru’s INEI released July GDP and August unemployment rate data on Sunday, with the former showing a much stronger than forecast rise in economic activity and the latter showing an expected uptick in the jobless rate. The 4.5% y/y jump in economic activity (vs 3.5% median) marked a massive turn from June’s 0.2% increase, with all sectors with the exception of agriculture showing positive y/y readings. Manufacturing output continued to benefit from a strong fishing season—and thus processing—going from a 0.2% y/y rise in June to a 11% increase in July. Construction printing a 7.1% y/y increase thanked a 34% jump in public projects spending. As for an obvious impact from pension fund withdrawals in late-June/July, the evidence is mixed as retail sales climbed by 3.9% but vehicles and parts sales fell 2.4%. The data reinforces expectations that the BCRP will hold at its next meeting. Note that on Friday, Peru’s government announced that they will take on the burden of Petroperu’s debt repayments over the balance of the year.

—Juan Manuel Herrera

COLOMBIA: BANREP SURVEY—MIXED INFLATION EXPECTATIONS, WHILE CONSENSUS AFFIRMS EXPECTATIONS FOR A 75BPS CUT IN SEPTEMBER

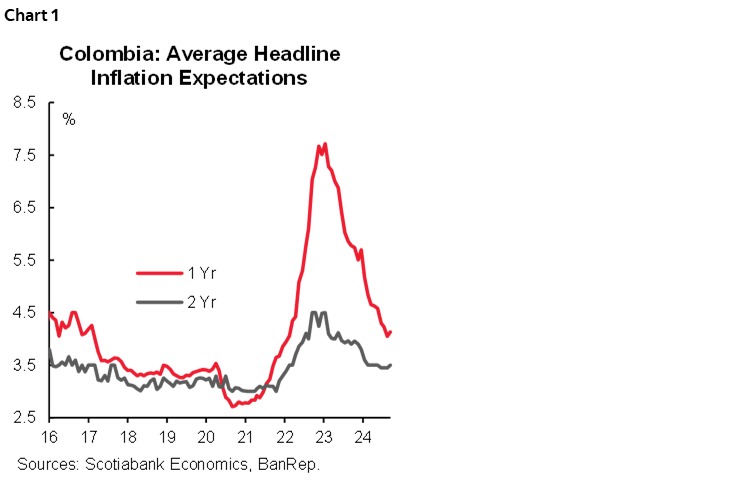

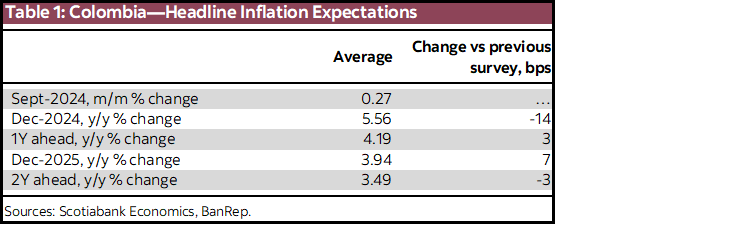

The central bank (BanRep) released a survey of economists’ expectations for September. Inflation expectations showed mixed behaviour; expectations for the year-end decreased, while in the medium-term, the change was mild on average. The one-year inflation expectation is at 4.19%, up by 7bps, while the two-year horizon (September 2026) decreased by 7bps to 3.94% (chart 1). As for short-term inflation expectations for September, the expectation is at 0.27% m/m, which could lead to inflation falling to 5.84% from the current 6.12%. Scotiabank Colpatria’s projection is 0.22% m/m and 5.84% y/y. Despite the truck drivers’ strike having an impact on food inflation, it is expected to vanish, while the rest of the items are expected to have moderate changes.

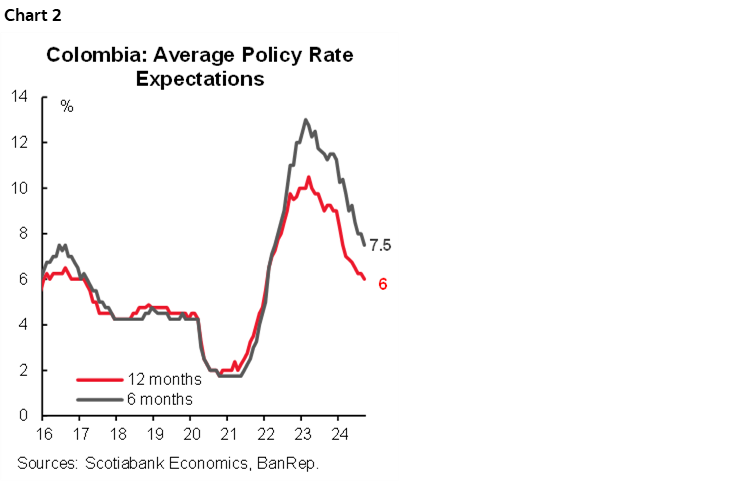

In the case of the monetary policy rate, consensus affirmed a 75bps rate cut as the base case scenario for the September 30th meeting. However, the year-end 2024 expectation increased by 25bps to 8.75%, and for Dec-2025, the expectation is 6%, while the terminal rate of 5.50% will be reached in Q3-2026 . At Scotiabank Colpatria, the projection is for three consecutive cuts of 75bps this year to close at 8.50%, while the terminal rate is expected to be 5.50% in H2-2025.

Ahead of September’s meeting, the central bank board will have plenty of arguments to debate about whether to accelerate the easing cycle or not. Economic activity is showing mixed behaviour in which traditional private activities such as commerce and industry remain weak, inflation has been in a consistent downward trend, inflation expectations show credibility in the disinflationary process, the current account deficit is very narrow and employment data is pointing to a stagnation. On the other side, the volatility in the FX has increased, however without reaching concerning levels to think about a huge impact on inflation. Having said that, at Scotiabank we maintain our expectation for a cut of 75bps to 10% at September’s meeting.

Key points from the survey :

- Short-term inflation expectations. For September, the consensus is 0.27% m/m, which implies an annual inflation rate of 5.84% y/y (compared to 6.12% in August). The maximum expectation is 0.27% and the minimum is 0.11%. Scotiabank Economics’ projection is 0.22% m/m and 5.79% y/y. Core inflation excluding food projected by analysts is 0.25% m/m.

- Medium-term inflation expectations improved. Inflation expectations for December fell by 14bps to 5.56% y/y (table 1). Similarly, expectations for the one-year horizon were 4.19% y/y (+3bps). The two-year inflation expectation fell by 3bps to 3.49%.

- Monetary policy rate. The median expectation points to a rate cut of 75bps at the September meeting, however for October the expectation is a 50bps cut, and in December a 75bps cut, which is a path that is not compatible with the traditional approach of the central bank. The 2025 expectation for the year-end remains at 6% (chart 2).

- FX. Projections for the US dollar exchange rate for the end of 2024 averaged 4,191 pesos (147 pesos above the previous survey). For December 2025, respondents, on average, expect an exchange rate of 4,075 pesos.

—Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.