- Inflation increased by more than expected. Again.

- It wasn’t just due to base effects. Again.

- Don’t dismiss higher inflation due to possibly transitory factors…

- ...as key sectors may be temporarily soft

Canadian CPI, m/m / y/y %, May:

Actual: 0.5 / 3.6

Scotia: 0.4 / 3.5

Consensus: 0.4 / 3.5

Prior: 0.5 / 3.4

Canadian core CPI, y/y % change, May:

Average: 2.3 (prior 2.1%)

Weighted median: 2.4 (prior 2.3%)

Common component: 1.8 (prior 1.7%)

Trimmed mean: 2.7 (prior 2.3%)

Here are three things you are probably getting used to hearing by now:

- Inflation increased by more than expected.

- It wasn’t just due to base effects.

- Don’t dismiss it because of possibly transitory upsides because there may also be transitory factors that are holding inflation back.

On the first point, inflation was a tick faster than expected in month-ago (+0.5% m/m NSA) and year-ago (3.6% y/y) terms. That’s less of an upside surprise than the prior month, but not by much in seasonally adjusted terms as total prices increased by 0.4% m/m in May after a 0.6% rise in April. The BoC’s old CPIX8 measure of ‘core’ inflation also climbed by 0.4% m/m SA after a 0.7% gain the prior month.

Core inflation also climbed again to 2.3% y/y from 2.1% the prior month using the average of the three measures of core inflation that the BoC has tended to emphasize. Chart 1 shows this acceleration.

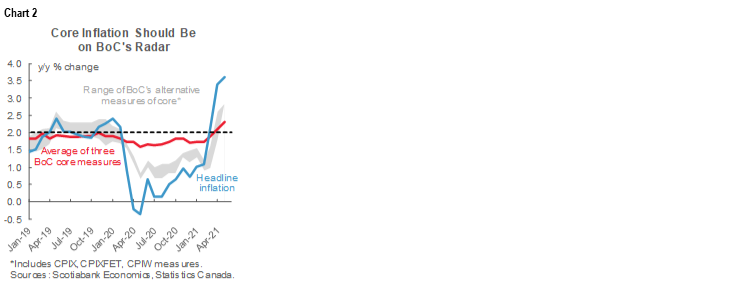

Chart 2 shows that all of the main core inflation gauges are accelerating so it’s not just headline inflation that is doing so.

Several points can be made regarding base effects. First, the acceleration of average core inflation from a bottom of 1.6% y/y in May of last year to 2.3% now is about more than just base effects given this measure only decelerated by a few tenths of a percentage point from just before the pandemic into the thick of the shock. Therefore, core price weakness through the heart of the pandemic was not actually that big of a deal. The speed of acceleration since then is outpacing the early disinflationary impact of the pandemic.

Furthermore, the BoC knew the base effect starting point for prices in real time when it was forecasting inflation in successive Monetary Policy Reports over the past year but persistently lowballed actual inflation (chart 3). Even its April MPR forecast reset is getting surprised higher. Where the BoC has been surprised should be expressed in terms of greater than expected resilience of the monthly price changes through 2020 into early 2021 and then the recent month-over-month acceleration. That’s even truer for the camp that was arguing deflation risk from the start and has been wrong.

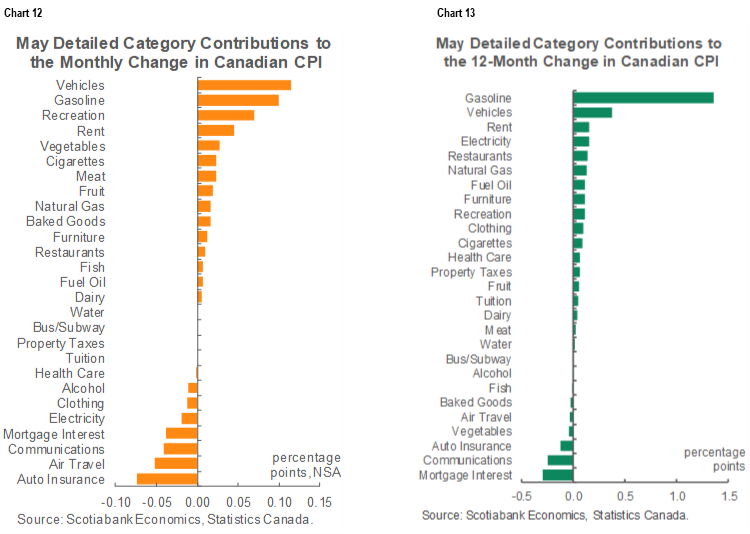

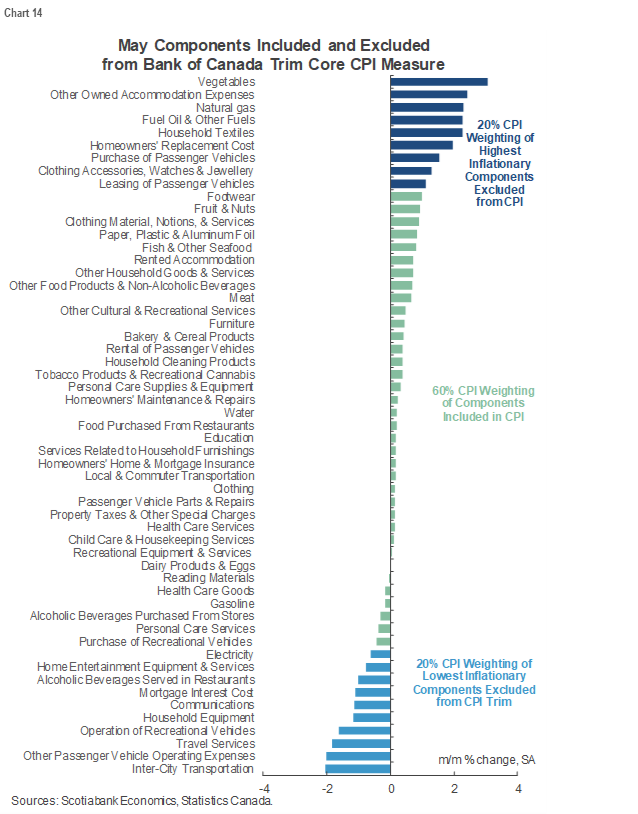

Regarding transitory factors, there is a whole lot of cherry-picking going on by the camp that says this is all just a flash in the pan. Some categories that could be transitory upsides right now include items like gasoline price inflation that is already turning lower (chart 4). Then again, what if gas price inflation eventually returns with rising mobility in reopening economies over time and more ‘normal’ future summer driving seasons? Electricity prices (chart 5), furniture prices and some of the other hot items in charts 12–13 (page 4 due to their sizes) that contributed the most to the year-over-year rise in CPI on a weighted basis are other examples of what might be transitory upsides.

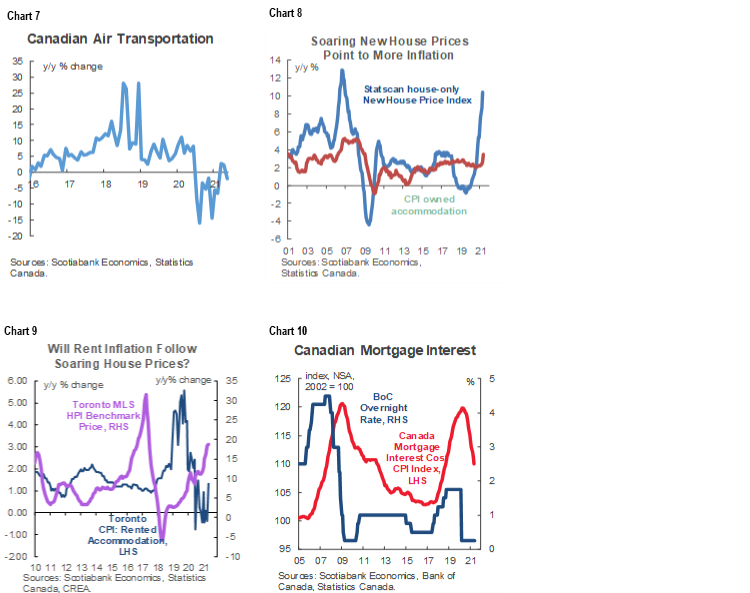

But then we have items that may be temporarily soft and poised for cyclical upsides going forward. The obvious first candidate is broad goods versus services price inflation (chart 6). Right now inflation is mostly about accelerating goods price inflation as the availability of goods has been less impaired by social distancing given online ordering and delivering and curbside delivery. Goods price inflation may persist as recoveries unfold around the world and as supply chain issues may persist for a long time.

But what if services price inflation really begins to accelerate as the economy reopens? Some types of services are starting to do so while others remain weak and are more dominant in restraining broad service prices. Some prices like restaurant food never really saw material disinflation despite the fact many of them have spent the better part of a year shut! Various support programs for rent and wages insulated against some of the disinflationary shock. One point I’d emphasize is that this is going to be a longer term full cycle debate to see what happens to inflation and not just rooted in seeing whether price inflation ebbs over, say, the next 6–12 months as central banks tend to emphasize.

As for specific examples, will airline pricing power always be weak or will vaccinations and a gradual return to travel perhaps restore airfare inflation (chart 7)? Are we capturing the full lagging effects of soaring new house prices on the replacement cost component of housing within owned accommodation CPI just yet (chart 8)? Will soaring new house prices put upward pressure upon rents again given a volatile but generally lagging relationship as impaired housing affordability may tend to then make the rental market look more attractive to some (chart 9)? Mortgage interest costs are still disinflationary because it takes a while for the BoC’s rate cuts last year to finish moving through the mortgage renewals pipeline but that effect should stabilize into next year (chart 10).

The point of the exercise here is to illustrate that inflation risk needs to consider the possibility that we’re not just seeing firmer inflation because of year-ago base effects and we can’t just focus upon price inflation in areas that may be transitory. Central banks are supposed to be risk managers and risk managers are supposed to focus upon upside and downside risks. All I’ve heard coming from too many of them are references to downside risk in a nearer term sense which makes me feel like they are clinging too long to justifying the actions that drove massive stimulus in the early stages and perhaps remain too slow to change the narrative around. The BoC may be different, however, in its references to inflation risks being “roughly balanced” going forward despite some of its tendency to dismiss inflation as a base effect phenomenon.

The second purpose to the points above is to complement a top down view on inflation that is rooted in a Phillips curve approach. As the US eliminates spare capacity and closes its output gap later this year in our forecasts and Canada does so by early next year, the lagging influences of eliminating spare capacity should keep inflation at or above target over central bank forecast horizons. Labour market influences upon inflation are uncertain because we don’t know where the full employment level of the unemployment rate may rest going forward which depends upon matters like how many of the lost jobs may really come back, retirements, the impact of slow immigration etc. This top down view always benefits from more colour provided by a bottom up view as important inflationary developments often driven by idiosyncratic factors can otherwise be missed. Then we can also have a debate on whether the structural forces of the past that kept inflation low will repeat in future. Alternatively, factors like demographics, trade policy and technological change through pricing power exerted by big tech may offer marked changes from the past.

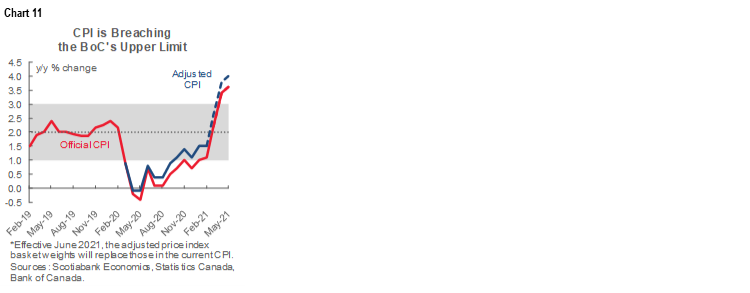

In any event, it is getting progressively more difficult for the BoC to talk through rising inflationary pressure. Chart 11 gets the final word here. After tacking on the coming pandemic-weights adjustment, inflation is at about 4% y/y. That’s way past anything the BoC has forecast to date as shown back in chart 3. Why it keeps saying inflation is just a base effect phenomenon that will magically and permanently go away including at its latest press conference remains a tough narrative to believe. Speeding up the exit from its GoC bond purchase program and getting on with guiding borrowers to expect rate hikes should be getting more attention over the duration of the year.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.