LARGE WINDFALLS BRING ANOTHER YEAR IN BLACK

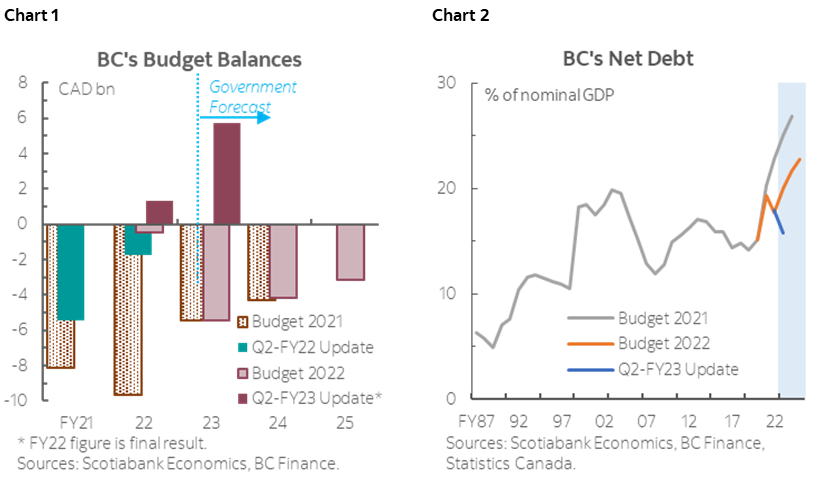

- Budget balance forecasts: $5.7 bn (1.5% of nominal GDP) in FY23, a turnaround from the -$5.5 bn (-1.5%) deficit projected in Budget 2022 (chart 1).

- Net debt: expected to decline from 17.9% of nominal GDP in FY22 to 15.8% in FY23—4.2 ppts lower than projected in Budget 2022 (chart 2).

- Real GDP growth forecast: nudged down slightly to 3.2% in calendar year 2022 from prior projection of 4.0% in the 2022 Budget; nominal GDP projection raised from 5.8% to 11.6% due to higher-than-anticipated inflation.

- Borrowing program: total borrowing requirement reduced to $7.1 bn for FY23 including a provision of $0.3 bn forecast allowance—a $1.9 bn reduction from the Budget estimate. Over 78% of borrowing requirement for FY23 completed as of November 25th, 2022.

- The largely improved fiscal trajectory outlined in the Update provides a better starting point for the upcoming fiscal years as economic headwinds mount. The spending profile was lifted only modestly, with half of the increase stemming from the affordability measures announced last week.

OUR TAKE

BC is on track to hit a second year in the black following a balanced book in FY22, as faster-than-anticipated nominal growth drives large revenue windfalls and puts the province on a stronger financial trajectory than expected in the 2022 Budget. The government revised its FY23 balance projection from a -$5.5 bn deficit to a $5.7 bn surplus, with revenues now tracking $12.5 bn higher than the budget estimate. Program spending is expected to rise slightly by $2.3 bn versus the Budget, largely due to costs of recently-announced affordability measures—totals $1.1 bn on the expense side of the ledger. The projection kept $5.1 bn in various contingencies and standard forecast allowances over this horizon, leaving room for upside.

The strong economic growth assumptions underpinning the revenue outlook seem reasonable. The Update acknowledges the weakening growth outlook in the province by nudging down its real GDP forecast to 3.2% for 2022 and 1.5% for 2023, respectively higher than the private-sector averages by 0.4% and 1%. The optimism is supported by stronger-than-anticipated 2021 tax revenues reported by CRA. Due to BC’s larger exposure to housing markets and hence high interest rates, we expect the province’s real growth to lag the national average this year and next—projected at around 3.2% this year and 0.6% in our latest forecast tables.

The province doles out part of the windfalls to expand its affordability measures, a major share of which will kick in over the following months. The big ticket item of FY23’s $2 bn cost-of-living measures is the Affordability Credit announced last week—which targets lower- to middle-income individuals and families and has relatively limited fiscal impact of about $1 bn (0.3% of nominal GDP) this fiscal year. Other measures focus on energy costs relief—including the gas rebate administered through ICBC ($395 mn) and the one-time BC Hydro bill credit ($320 mn).

The upgraded budget balance outlook also sent the province’s net debt to a much lower trajectory—the 15.8% taxpayer-supported debt-to-GDP ratio estimated in the Update is a material improvement from Budget 2022’s projection of an uptick in the ratio to close to 20% in FY23. The province also reduced its borrowing requirement to $7.1 bn for FY23, with $1.5 bn remaining to be completed as of November 25th, 2022.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.