DEPLOYING STRONG REVENUE GAINS TO FIGHT INFLATION

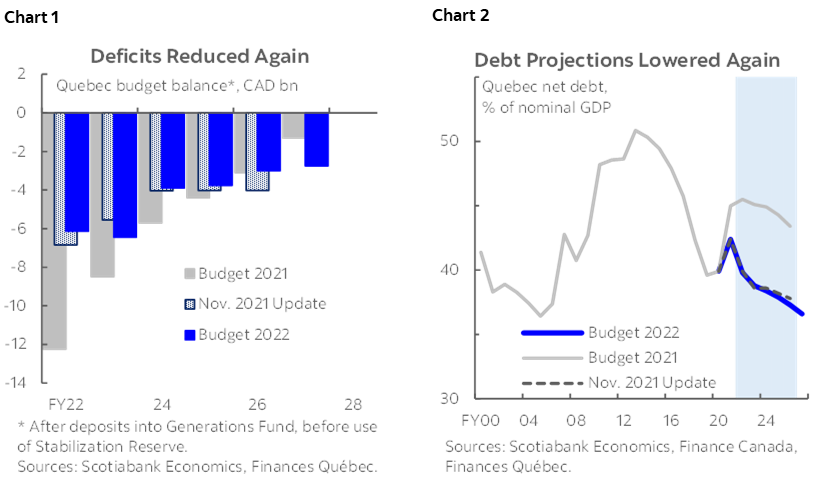

- Budget balances: -$7.4 bn (-1.5% of nominal GDP) in FY22, -$6.4 bn (-1.2%) in FY23, -$3.9 bn (-0.7%) in FY24, then eases to -$2.8 bn (-0.5%) in FY27, slightly lower than in mid-year fiscal update (all figures after Generations Fund deposits) (chart 1).

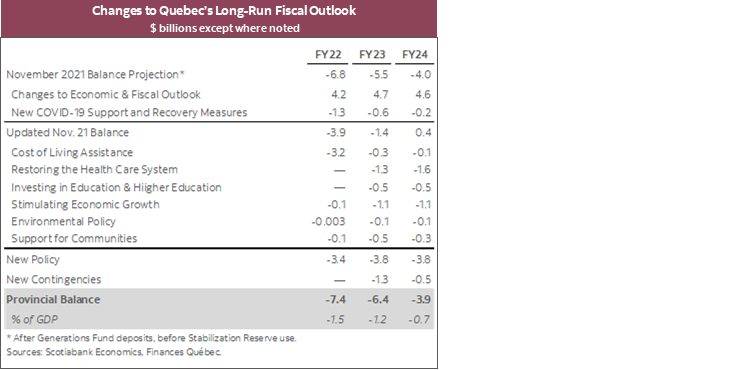

- Net debt: expected to decline gradually from 39.8% of nominal output in FY22 to 36.6% by FY27—also slightly lower than in the November 2021 update (chart 2).

- New policy: $3.4 bn in FY22, $3.8 bn in FY23, $3.8 bn in FY25, combined $22.3 bn over FY22–27 accounts for 0.7% projected GDP; measures are initially concentrated in pocketbook relief, then tilt towards health system capacity expansions.

- Infrastructure spending: increased by a combined $2 bn during FY23–25, capital outlays under the Quebec Infrastructure Plan (QIP) now expected to increase by 34% in FY22, then fall by 5% in FY23.

- Financing program: expected to reach $22.9 bn in FY22, $27.6 bn in FY23, $30.1 bn in FY24, and average $30.5 bn during FY25–27; projected FY22–26 total is about $3.8 bn lower than forecast in the November 2021 update.

The province’s fiscal position is marginally improved. Relative to the November 2021 mid-year update, own-source revenue projections were raised by $4.3–4.8 bn per year from FY22–24 following a stronger-than-forecast economic recovery. The province’s “structural deficit” (i.e. budget balance after deposits into the Generations Fund to pay down debt) has been reduced relative to mid-year projections. Before Generations Fund deposits, Quebec expects to balance in FY24—one year earlier than in the mid-year update. Net debt is forecast to converge to a slightly more modest share of GDP. Planned program spending increases are generally in line with expected population and inflation gains beyond FY22. Quebec’s debt levels are higher than those in many other provinces, but its success lowering that burden since the early 2010s is impressive.

There is some upside built into projections. Contingencies are significant at $2.5 bn in FY23 and $1.5 bn per year through FY27. Nominal GDP growth projections are in line with the private-sector mean for 2022, and incrementally below that average in the outer years of the plan. Supplementary estimates to the budget associate every 1 ppt in nominal GDP growth with $950 mn in own-source revenues in FY23. Incorporating these cushions into the plan is wise given economic uncertainty at the global level caused by the Russia-Ukraine conflict.

Budget includes $22.3 bn in new policy initiatives (0.7% of nominal GDP), evenly split over FY22–27. In FY22, the key measure is a one-time, $500 per person payment to Quebeckers earning $100k per year or less—with a price tag of $3 bn—to mitigate the effects of the global surge in inflation. Later, policy is dominated by gradually escalating health care spending, which includes funding to improve workflow and service delivery at health facilities, and money to improve health care system accessibility. Efforts to increase long-run economic growth include: a new $1.3 bn 2022–27 Research and Innovation Strategy to assist productive research and technology-oriented businesses; French language training for immigrants and support to attract them to regions in need; and stimulus for the tourism, accommodations, and cultural sectors, concentrated in FY23–24.

In line with the reduced deficit profile, Quebec’s financing program was reduced. The province now expects to borrow $22.9 bn in FY22, $27.6 bn in FY23, $30.1 bn in FY24, $33.8 bn in FY25, and $32.5 bn in FY26; the FY22–26 total represents a cut of $3.8 bn from November 2021 projections. To date in FY22, 37% of borrowing had been conducted on foreign markets—higher than the 24% average in the prior 10 years. Just over 63% of long-term borrowings were conducted in Canadian dollars in FY22; the majority of foreign currency issuance denominated in Euro. The average maturity of FY22 borrowings was 18 years. The province reiterated its commitment to green bond financing; six issues totalling $3.3 bn have been made since Quebec’s Green Bond program was launched.

Overall, Quebec’s budget aligns broadly with our expectations. The province’s economy continues to show momentum coming out of pandemic lockdowns and that has translated into stronger revenues; as indicated in the leadup to the plan, the government has targeted pocketbook relief in the near-term. While the signature cost-of-living assistance payment is broad-based and as such has the potential to stimulate demand and further price pressures, it is at least time-limited. Long-run economic growth initiatives will take time to bear fruit but appear appropriately targeted. For the coming months, risks to the economic outlook are real, but prudent planning assumptions and credible fiscal anchors should be reasonably well-received by the province’s creditors.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.