- January can be a difficult month, particularly in a cold, dark northern hemisphere winter, as the euphoria of the holidays fades, seasonal flues circulate, and a general malaise—the January “blues”—sets in.

- This January, the Latam region, along with the rest of the world, is bracing for the possible effects of the omicron variant. These could include a sharp slowdown in economic activity as workers remain at home sick or in accordance with public health isolation protocols. Further disruption to global supply chains could also extend supply-side price pressures, complicating the rebalancing of monetary conditions now underway.

- There is reason for guarded optimism that the effects of the latest variant will be contained. But that outcome is not assured and even if the latest wave of the pandemic is short-lived, the Latam region will be preoccupied fighting the January “flues.”

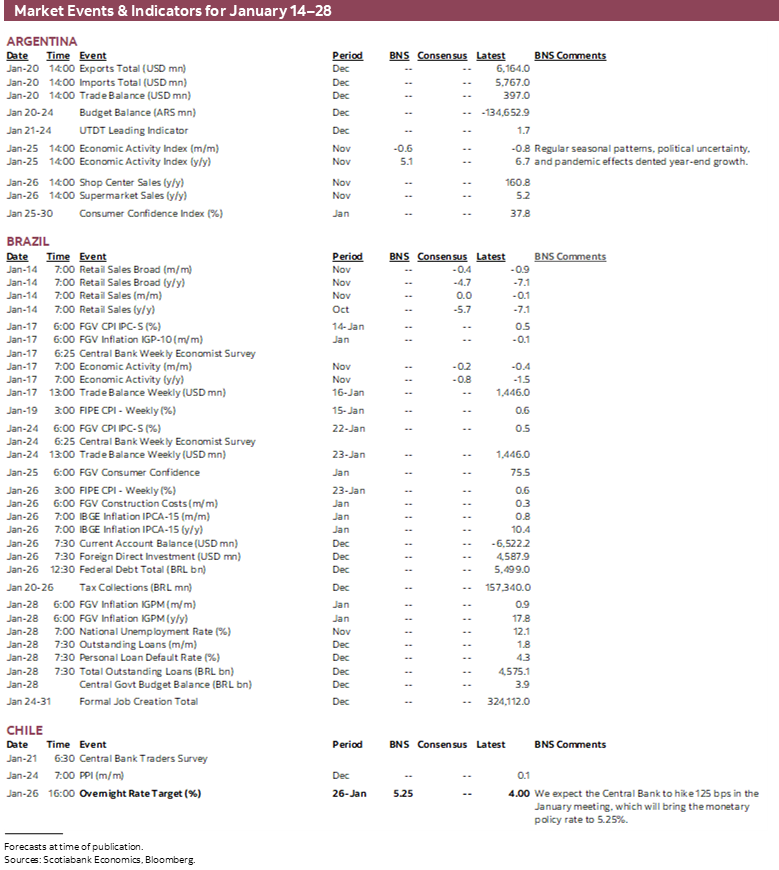

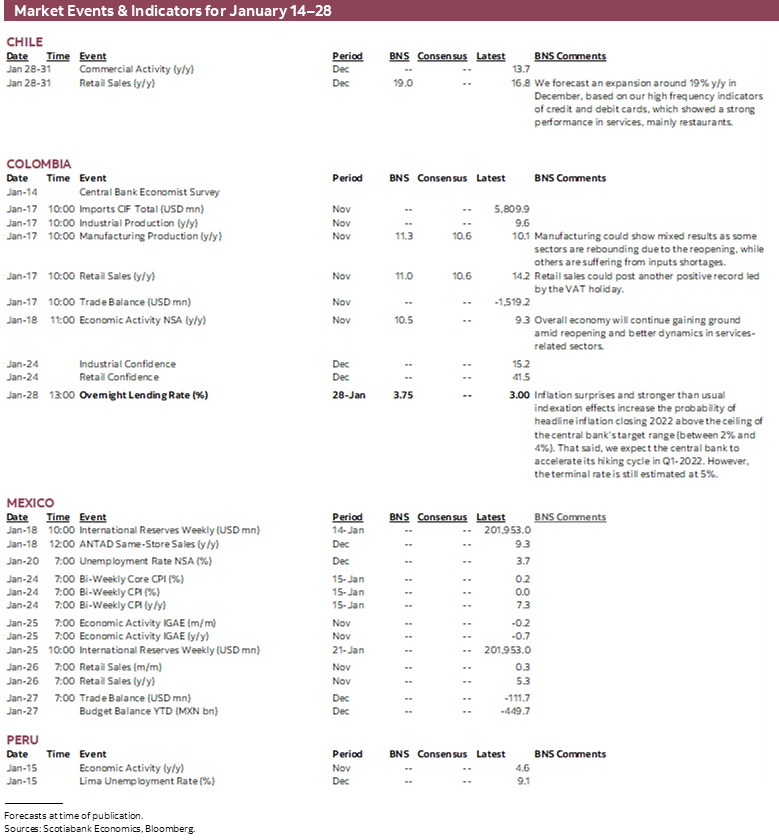

KEY ECONOMIC CHARTS

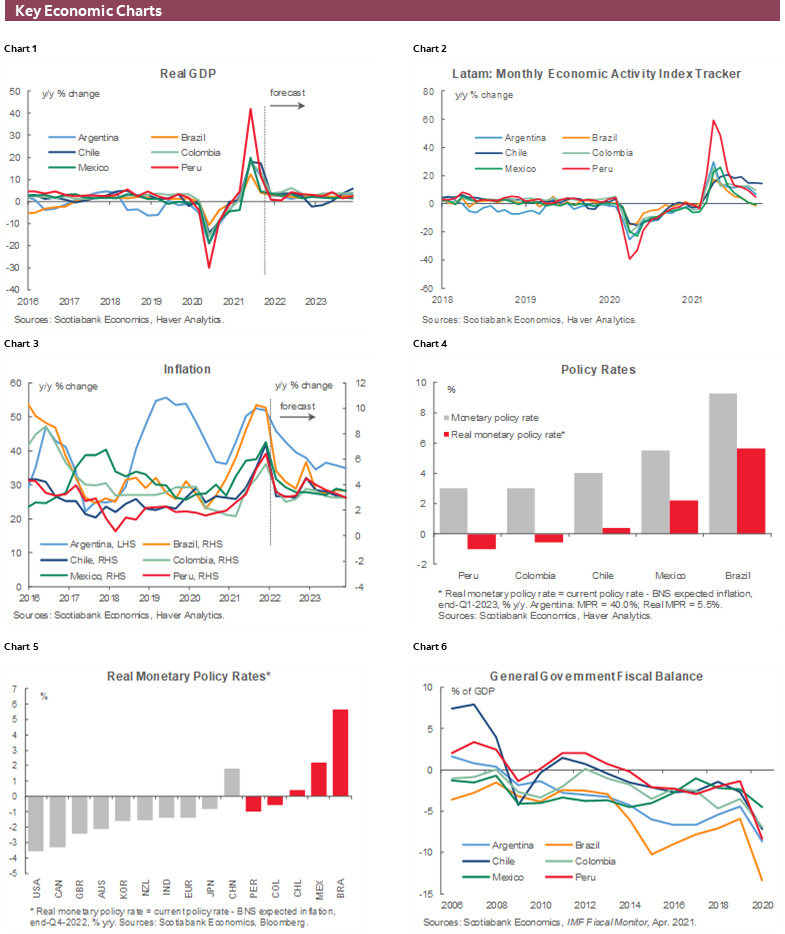

As the new year begins, the omicron variant introduces new uncertainties with respect to the economic prospects for the Latam region. There is reason to believe that the economic effects of the latest wave of the pandemic could be limited, notwithstanding the dramatic spike in cases. Economic growth is expected to moderate in 2022, coming off a rebound in output in 2021 (chart 1). And prior to the latest outbreak, Scotiabank economists anticipated year-over-year growth rates to broadly return to pre-pandemic levels across the region. For now, that remains the base case scenario.

The case for cautious optimism is based, in part, on the seemingly short duration of omicron outbreaks observed in other countries and indications that this strain is less virulent than previous variants; in part, on the adoption of practices that allow businesses to remain in operation despite the outbreak. Still, the omicron variant could have a significant economic impact through worker absences, which have already led to widespread airline cancellations, or the re-introduction of stricter social distancing measures or, in some jurisdictions, lockdowns.

Such effects are likely to show up first in y/y changes in monthly economic indicators (chart 2). Changes in the monthly activity index tracker for most countries were falling through the second half of 2021 as would be expected as the influence of base effects eroded over time. That said, signs of 2021 year-end weakness in Brazil and Mexico bear close monitoring.

There is also uncertainty with respect to the potential impact of omicron on inflation. Widespread labour shortages, as workers fall ill or isolate themselves in accordance with public health guidelines, could further disrupt global supply chains. Even a temporary outbreak could have long-lasting supply effects should it exacerbate existing bottlenecks, particularly if specific critical links in the global supply chain (e.g., microchips) are affected. This possibility is worrisome given the steep increase in inflation rates recorded across the region (chart 3).

Latam central banks have responded to growing price pressures by hiking key policy rates, aggressively so in some countries. This response reflects underlying concerns that higher inflation could become embedded in expectations, a development that could increase the output costs of bringing inflation back to target. In this respect, while headline inflation is currently well above inflation targets across the region, Scotiabank economists project a steady—albeit gradual—return to target ranges over the medium term.

Aggressive increases in central bank policy rates have led to an increase in real (after inflation) rates in Brazil, Mexico, and Chile (chart 4). Rates have likewise been hiked in Colombia and Peru in recent months. But rates in these two countries remain negative in real terms, despite these increases. They do not stand out against international peers in this regard (chart 5), though recent indications that the Fed and other advanced country central banks are poised to pull the trigger on rate hikes, including testimony this week by Fed Chair Powell, are likely to increase pressure on rates elsewhere.

Fiscal balances deteriorated sharply in 2020 as lockdowns shrank output and emergency support measures were extended (chart 6). The rebound in activity in 2021 has improved fiscal balances in the region, while governments have articulated plans to restore fiscal positions and introduced reforms to ensure long-term fiscal sustainability. Nevertheless, investors will closely watch increases in general government gross debt burdens (chart 7), along with external debt (chart 8), current account balances (chart 9), and total reserves (chart 10). While these indicators do not signal imminent problems, the decline in current account balances in Chile and Colombia reflected by the increase in external debt warrants monitoring going forward.

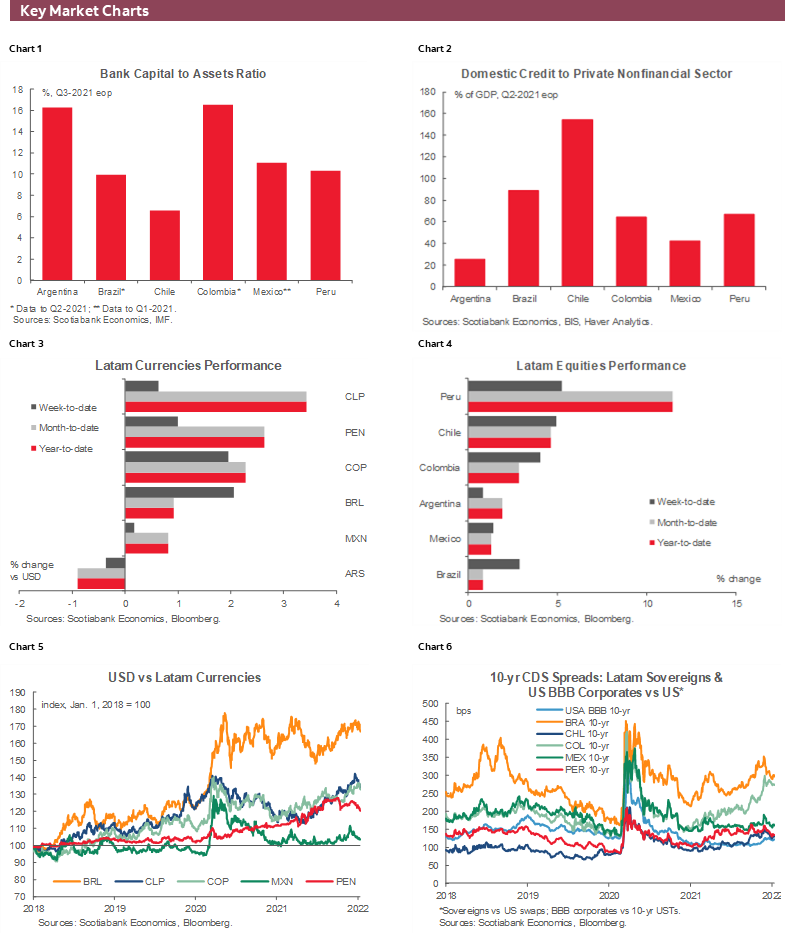

KEY MARKET CHARTS

Latam financial markets opened the year with currency appreciation and equity market gains. Currencies across the region appreciated against the US dollar, with the Chilean and Peruvian currencies leading the way (chart 3). The Argentine currency depreciated, however, possibly on news of expected challenges ahead in the government’s negotiations with the IMF.

Equity markets also rose throughout the region (chart 4). The strong performance in Peru may reflect the market’s pricing-in of reduced uncertainty on the political front. Political factors may likewise be mirrored in currency markets (chart 5) and 10-year CDS spreads of Latam sovereigns (chart 6).

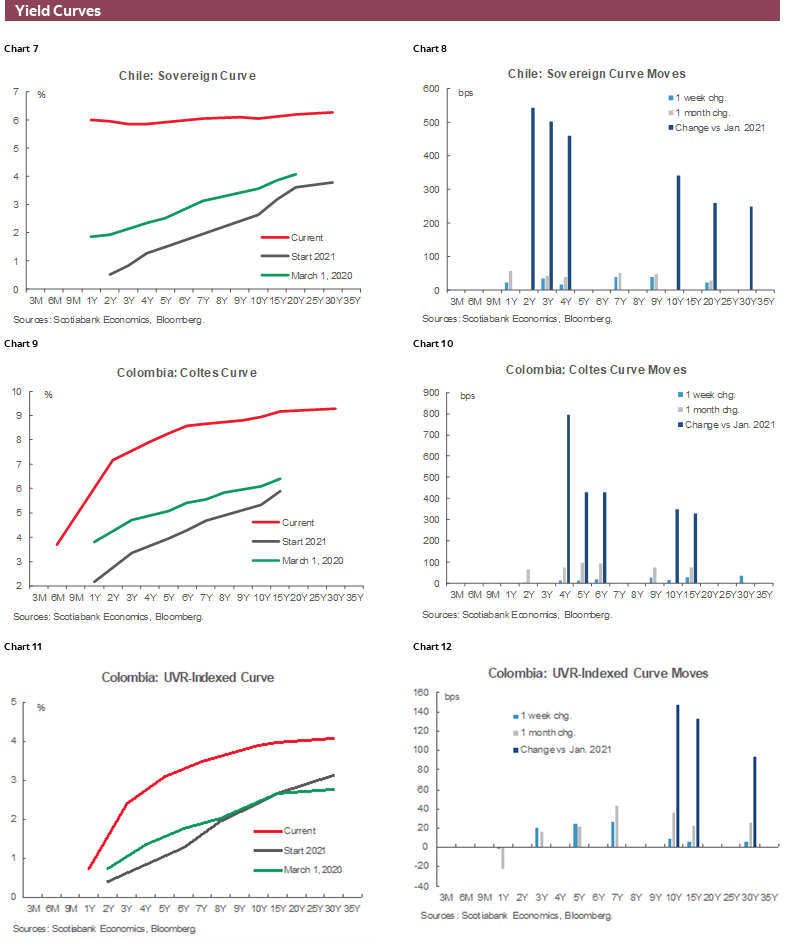

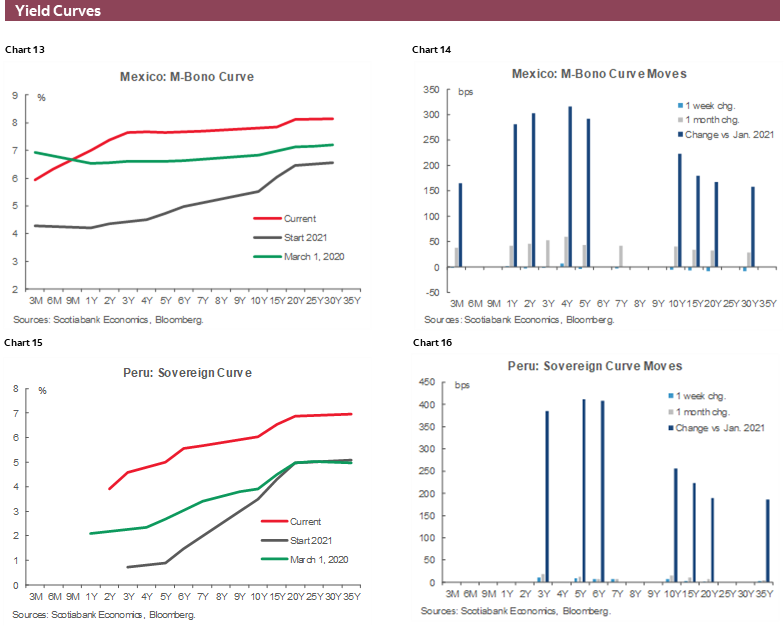

YIELD CURVE CHARTS

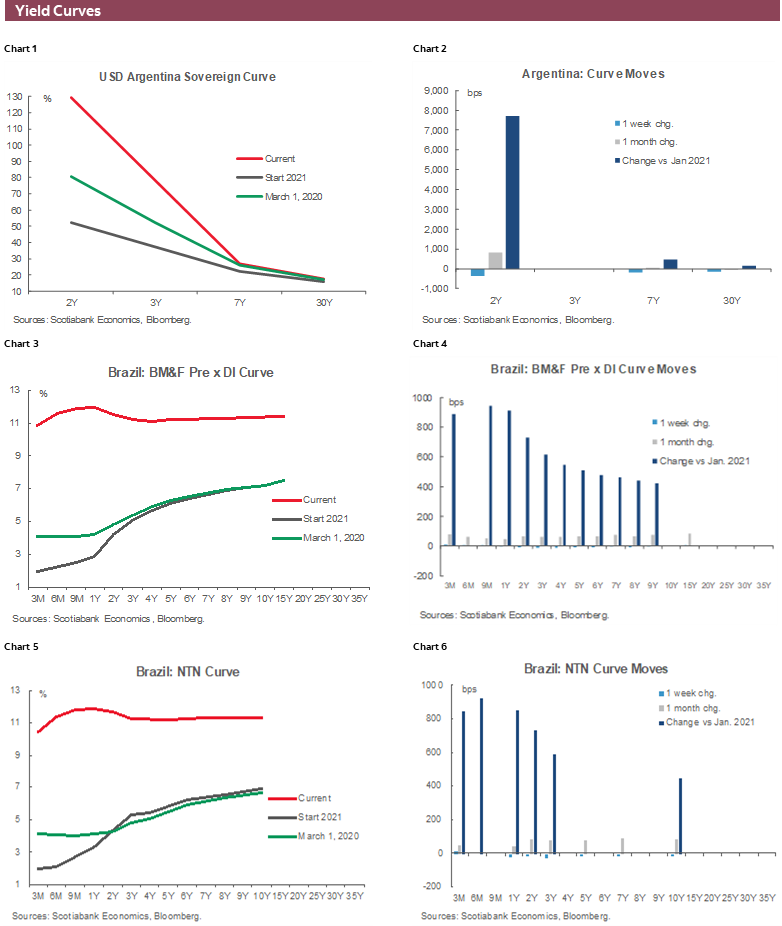

Sovereign yield curves have been largely stable in recent weeks. Most curves shifted up in 2021 as higher inflation and the effects of expected tighter money were priced in (charts 1–16). Yield curves have generally shifted up across the maturity spectrum. The Argentina yield curve, in contrast, is highly inverted, reflecting the unique circumstances there.

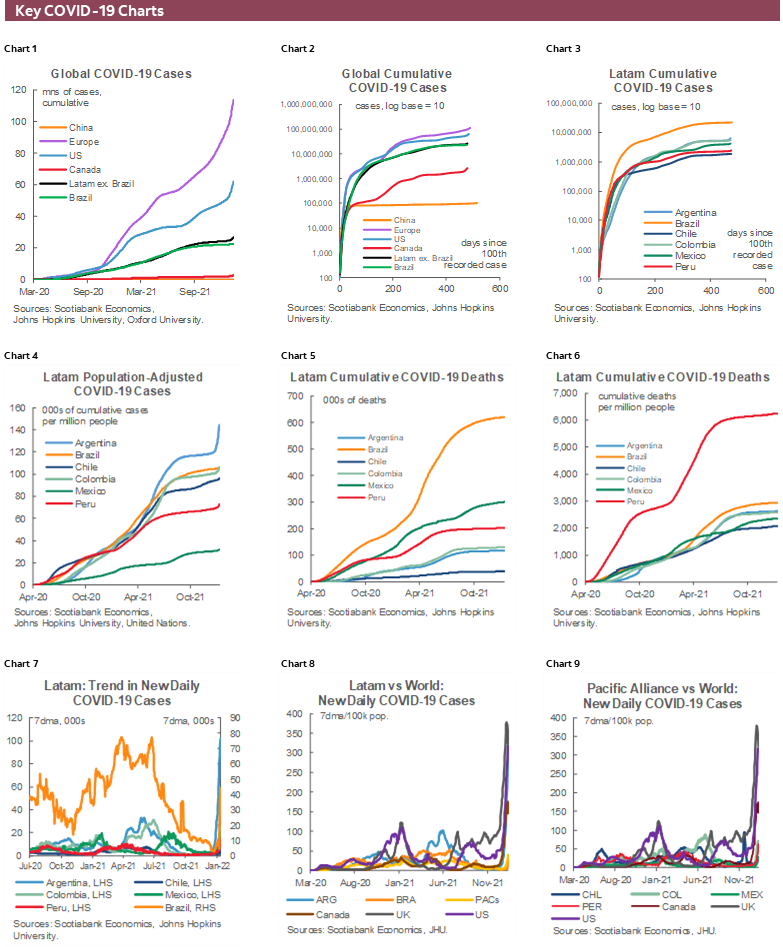

KEY COVID-19 CHARTS

As discussed above, short-term economic prospects depend crucially on the evolving pandemic, particularly the impact of the omicron variant on economic activity and inflation. In this respect, key monitoring charts (charts 1–12) already reveal the effects of the latest wave of the pandemic on the Latam region. Argentina has experienced the sharpest increase in cumulative cases per million people (chart 4), with smaller upticks discernible elsewhere.

The increase in new daily COVID-19 cases measured by a seven-day moving average (chart 7) in Argentina and Brazil is especially striking. Thus far, however, these increases are below those in advanced economies (chart 8). Similarly, while Pacific Alliance cases have ticked higher, they remain a fraction of the rates in advanced economies (chart 9).

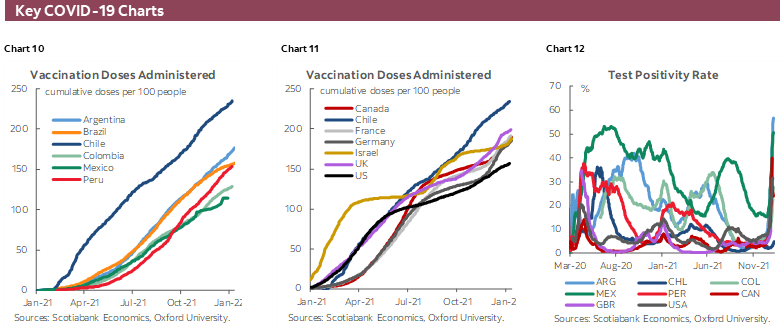

Meanwhile, vaccination programs continue, with Chile the clear leader in this regard both within the Latam region (chart 10) and around the globe (chart 11).

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.