- Economic recovery in the Latam region remains broadly on track and the outlook is positive.

- Inflation is up and central banks across the region have begun to withdraw stimulus. The direction of policy rate changes is not in doubt. The pace and aggressiveness of the tightening cycle is less clear.

- Financial markets appear to have priced in shifts in monetary policy; markets that had been affected by policy and political uncertainty earlier in the year have stabilized more recently.

- In nautical terms, the overall assessment could be “steady as she goes.”

KEY ECONOMIC CHARTS

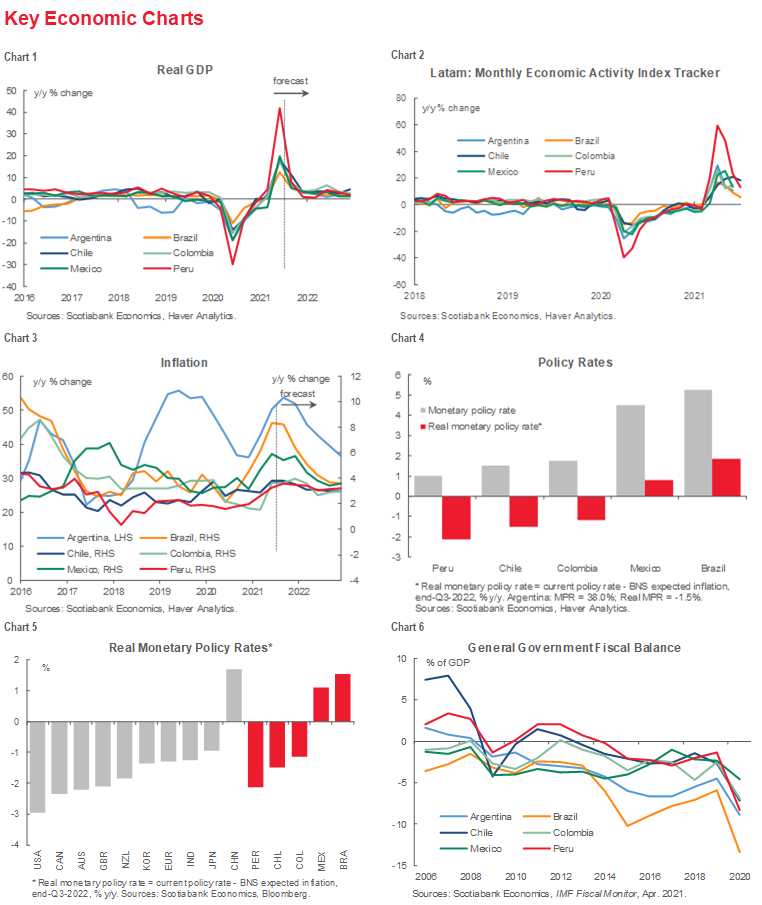

Economies of the Latam region continue to recover from the sharp collapse of economic activity early in the pandemic (chart 1). The bounce back has been particularly pronounced in Peru, which endured an especially severe contraction in 2020. While impressive, as we have consistently emphasized, high year-over-year growth rates that include base effects—the favourable comparison with 2020 levels depressed by the pandemic—will decline over time; growth is expected to converge on pre-pandemic levels in the medium term.

Evidence of eroding base effects is already emerging in high-frequency activity indicators, and this trend is likely to continue (chart 2). Nevertheless, the latest data remains encouraging and the overall outlook remains positive. For example, our team in Bogota reports that the latest data show manufacturing in Colombia is now at its highest historical level and that “pre-pandemic” is no longer the relevant benchmark. This recovery represents a remarkable turnaround from the situation earlier in the year, when nationwide protests disrupted production, and suggests good support for further growth going forward. Scotiabank’s team in Peru, meanwhile, reports that GDP increased by 13% (y/y) in July, indicating that the political uncertainty that followed the second round of presidential elections in June did not have much of an impact on growth. Our experts in Lima expect that y/y monthly growth rates will gradually decline consistent with their forecast of 12.3% for the year. While their estimate is higher than that of most other analysts, they are confident that other forecasts for growth will be ratcheted up. The BCRP has already indicated that it will raise its current forecast of 10.7%. At the same time, the latest employment and unemployment rate data for Lima, which show a pause in employment growth and a slight increase in the unemployment rate, are a reminder that recovery is not necessarily a linear process.

As recent editions of the Latam Weekly and the Latam Charts Weekly have highlighted, economic recovery has been accompanied by higher inflation (chart 3). All countries in the Latam region have seen inflation spike higher, though increases in Argentina and Brazil have been especially sharp. More moderate price rises have been recorded in Pacific Alliance members. These countries (and Brazil) have well established inflation-targeting regimes that help anchor expectations, though the latest inflation numbers exceed the upper bounds of those frameworks.

Higher inflation rates reflect several factors, including temporary shocks to global supply chains, and are expected to broadly return to pre-pandemic levels over the forecast horizon. Regardless, central banks in the region are grappling with the risk that higher inflation, even if transitory, could become embedded in expectations, raising the costs of bringing inflation back to targets prescribed by their inflation-targeting frameworks. To achieve this outcome, key policy rates (chart 4) will have to move higher. Central banks across the region have already acted. But with these rates in several countries negative in real—adjusted for inflation—terms, further increases are in the cards.

The direction of policy rate action is not in doubt. What is less certain is the pace at which central banks in the region recalibrate monetary policy conditions. A key consideration here is how their monetary tightening cycles align with the actions of other central banks and real policy rates in other countries (chart 5). At this point in time, Latam central banks appear to be in sync with their advanced economies counterparts in terms of real policy rates, with Brazil and Mexico seemingly ahead of the pack.

Central banks must balance long-term price stability commitments with short-run support for the economy. Moving too fast, too aggressively could withdraw support for the economy at a critical juncture; delaying too long could lead to higher inflation bleeding over into expectations. Striking the right balance is the policy challenge.

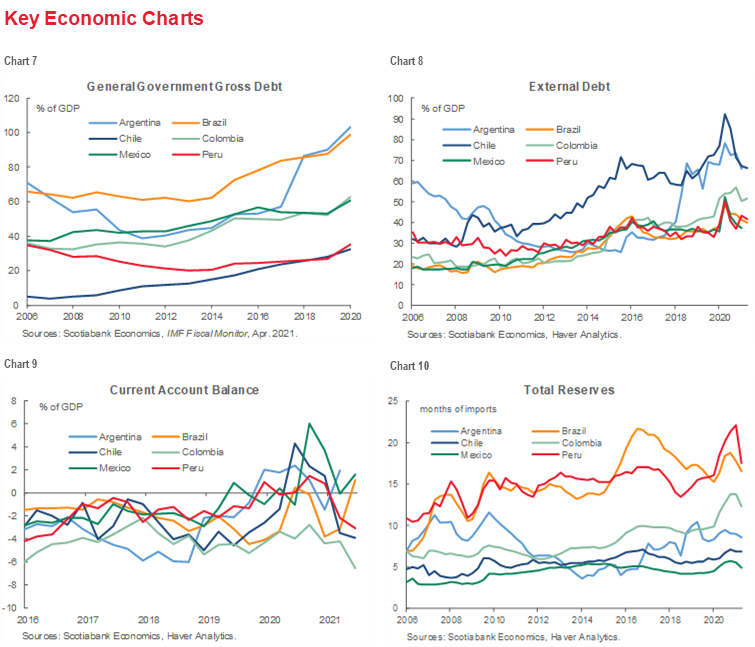

Fiscal policy, likewise, must balance continued support for individuals adversely affected by the lockdowns with long-term fiscal sustainability. Fiscal balances across the region deteriorated during the pandemic (chart 6) as governments adopted extraordinary measures to contain the economic costs of the crisis. The result has been a marked increase in gross debt as a share of GDP (chart 7). While external debt (chart 8), current account balances (chart 9) and total reserves (chart 10) are not signalling alarm, Latam governments will need to articulate clear plans to address fiscal balances and buttress their commitments to fiscal sustainability. In Colombia, President Duque recently signed new fiscal reforms into law that are aimed at achieving these goals.

KEY MARKET CHARTS

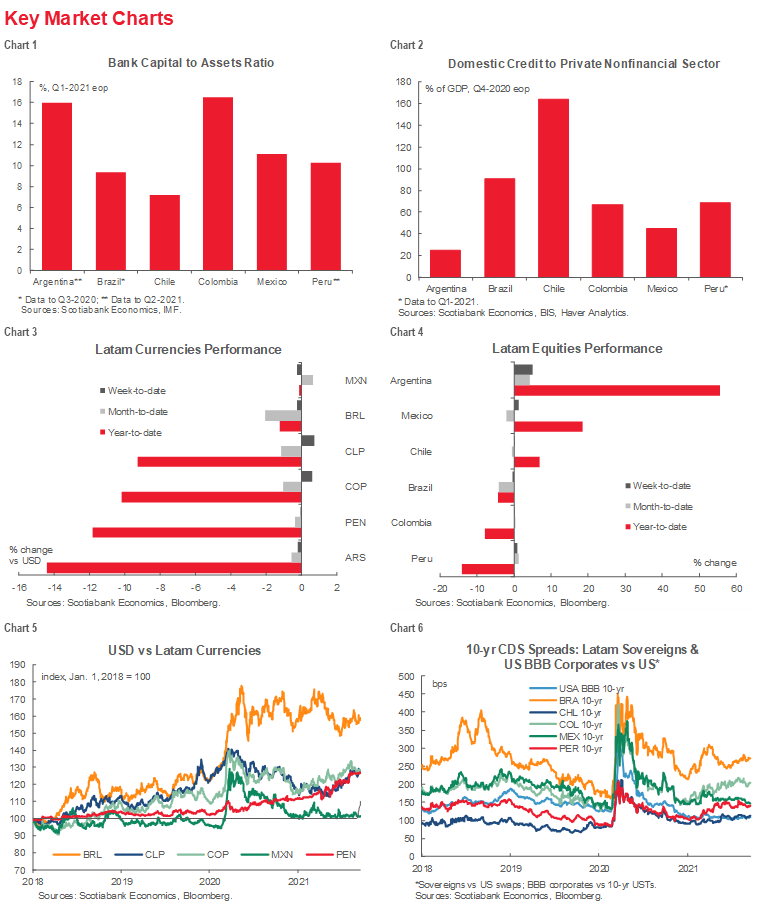

Fiscal reforms may account for the recent appreciation of the Colombian peso, which nevertheless remains down for the year to date against the US dollar. Currencies across the region more broadly have depreciated against the dollar since the start of the year (chart 3), with the Brazilian real bucking that trend, supported by aggressive policy tightening by the central bank. Political and policy uncertainty earlier in the year help explain currency depreciation, especially when viewed in a longer-term perspective (chart 5). The same could be said with respect to equity markets (chart 4) and 10-year CDS spreads (chart 6).

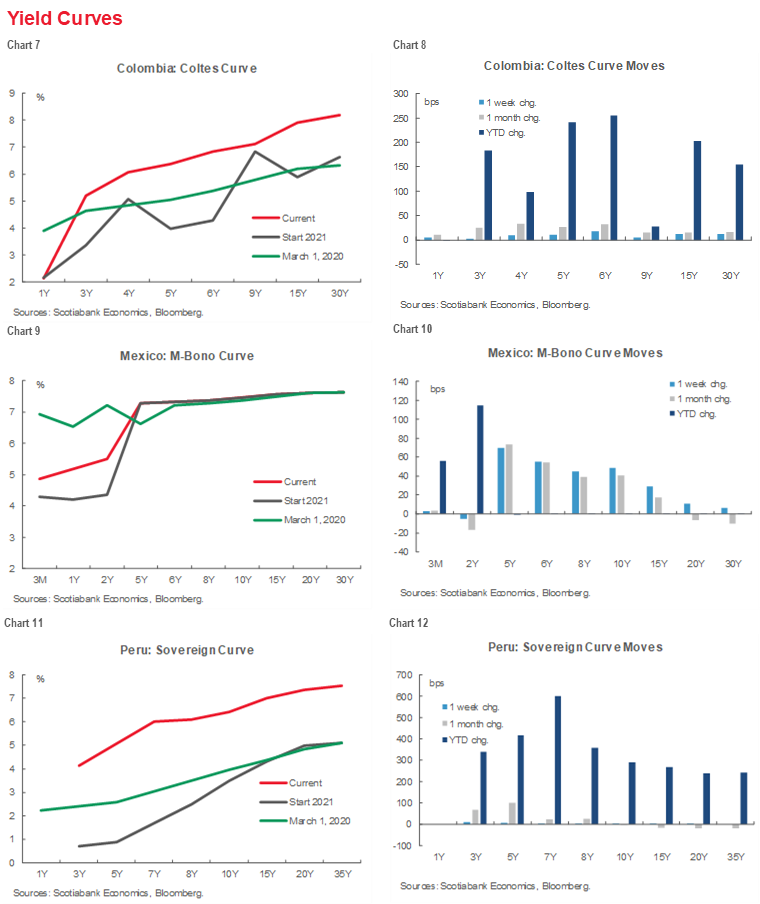

YIELD CURVE CHARTS

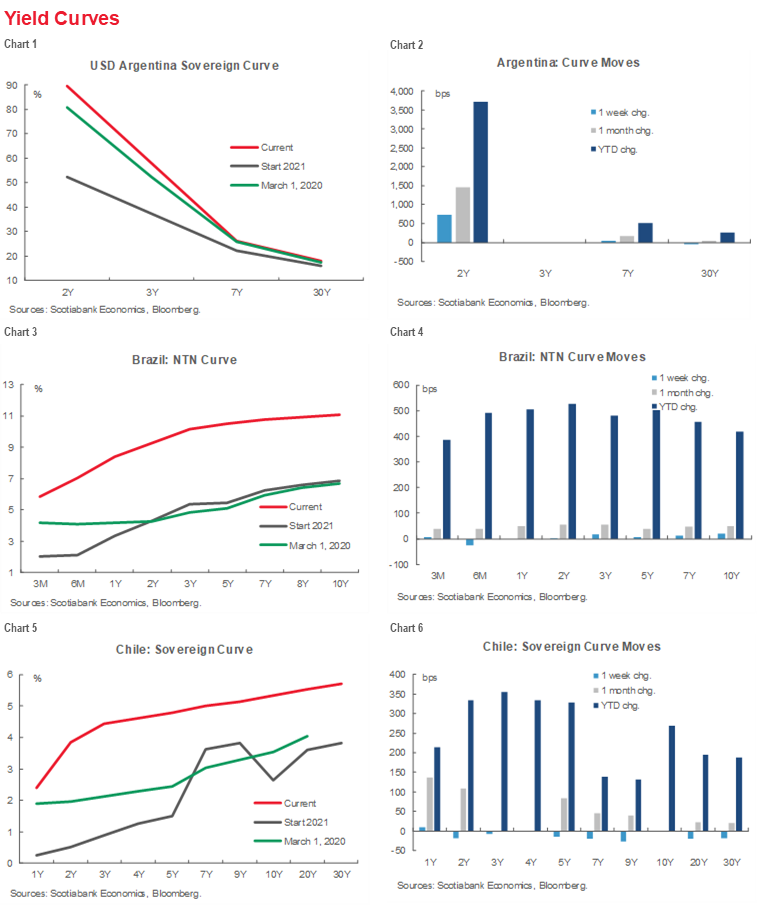

Latam sovereign yield curves have, for the most part, shifted up across the maturity spectrum since the start of the year (charts 1–12). Argentina, which has seen a steepening inversion, and Mexico, where the sovereign yield curve has been remarkably stable, are the two exceptions.

KEY COVID-19 CHARTS

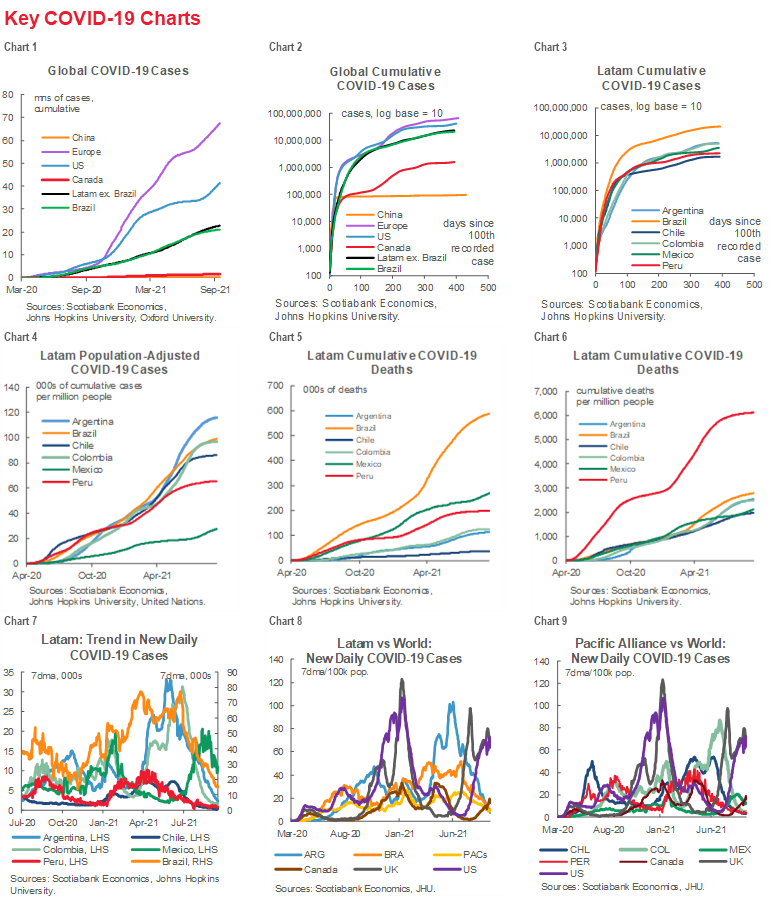

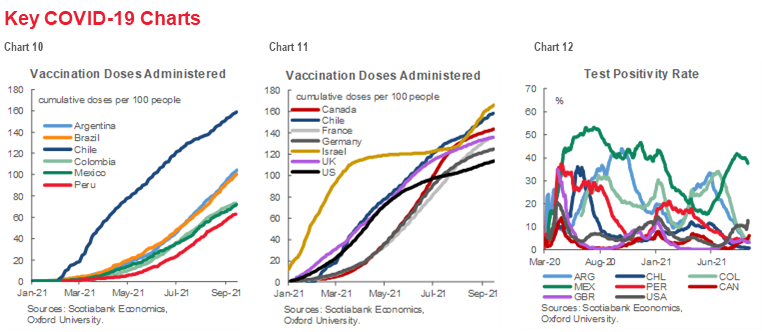

Our narrative above on the outlook is subject to continuing uncertainty with respect to the evolution of the pandemic and related policy responses (charts 1–12). Vaccines are the pathway to sustained economic growth. In this respect, Chile continues to lead the Latam region in vaccine doses administered. The progress made there offers reassurance with respect to economic growth. In contrast, the elevated test positivity rate in Mexico is a source of concern and warrants close monitoring.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.