- BCRP raises policy rate and signals possible pause.

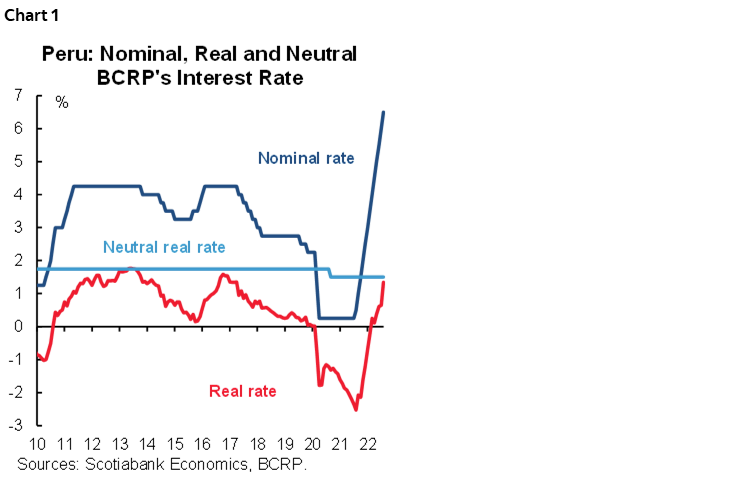

The Board of Peru’s central bank (BCRP) raised its key interest rate by 50 bps to 6.50% on Thursday, August 11, in line with the market consensus (Bloomberg), the interest rate swap market at 3 months, and our Scotiabank forecast. We believe that this could be the last increase in the current tightening cycle as the BCRP initiates a pause, provided that the reversal of inflationary expectations is confirmed after inflation peaked at 8.8% in June (the highest for the month of June in 29 years).

Inflation in July remained high (0.94% m/m), but may signal the beginning of a slowdown, as it fell from 8.8% y/y in June to 8.7% y/y in July. Surprisingly, 12-month inflation expectations also moderated, going from 5.35% in June to 5.16% in July. In the past, these expectations had reflected adaptive behaviour, which tend to make a downward adjustment a slow and gradual process. The reversal of inflation expectations in July allowed the real rate to go from 0.65% to 1.34%, still in expansionary territory, although it is very close to the real neutral rate of 1.5% (chart 1).

Like us, the central bank may entertain the possibility that inflation peaked in June. With this decision, and by reversing both inflation and its expectations, the interest rate hike cycle could thus be coming to an end. The key will be the speed at which inflation expectations moderate. With slowing inflation, inflation expectations, which have already been outside the target range for 13 consecutive months, would also moderate. Recent easing in international grain prices, oil and port costs increase the chances of this happening, although we assume the central bank will wait for clear evidence of easing price pressures.

The BCRP statement emphasizes that it projects a downward trend in year-on-year inflation owing to the moderation in international food and energy prices and a reduction in inflation expectations. We agree with that assessment, to which we add the influence of statistical base effects. The BCRP modified its expectation of the moment when it expects inflation to return to the target range. In the last four statements, its expectation of return to the target range was between Q2-2023 and Q3-2023. It now anticipates that it will do so during the second half of 2023 (between Q3-2023 and Q4-2023). This means that the BCRP sees a slower rate of convergence towards the target range; that is, inflation could remain high for longer than initially forecast.

In its statement, the BCRP reiterated that it will remain attentive to new information regarding inflation and its determinants, including inflation expectations and the evolution of economic activity, indicating that it is prepared to consider additional measures in the stance of monetary policy to ensure the return of inflation to the target range over the forecast horizon. This is the wording that has been used in recent statements, which would subordinate the next policy decision to the information available (data dependent). That said, to the extent that we expect inflation to have peaked in June, and given our expectation of inflation in August to be lower than in July, we see the BCRP possibly moderating the pace of monetary policy normalization, conditional on that the reversal of inflation expectations takes hold. Our forecast considers that the reference interest rate will remain at 6.50% by the year-end.

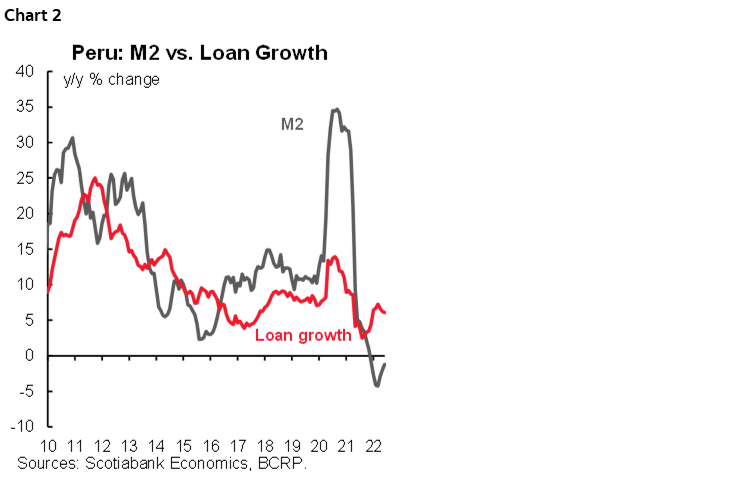

The statement also presents a more pessimistic outlook for global and local economic activity, emphasizing the decline in global growth expectations for this and next year despite some improvement in recent months. It also notes that most leading indicators and expectations for Peru’s economy continue to deteriorate and remain in pessimistic territory. On the quantitative side, the growth of the quantity of money (M2) remained in negative territory (-1.2% y/y in June) for the seventh consecutive month, although the rate of decline has moderated in the last three readings, which could reflect a greater comfort of the central bank with the current level of liquidity (chart 2). Loan growth maintained its dynamism in June, with a nominal rate above 6% y/y for the sixth consecutive month.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.