ECONOMIC OVERVIEW

- Mexican and Brazilian mid-July inflation data is the highlight of a relatively quiet Latam week ahead. After recent losses, local rates could’ve benefitted from soft prices data, but that seems unlikely.

- In today’s report, our team in Colombia go over the country’s transformation over the past few years and their hopes for a return to a pre-pandemic Colombia. In Peru, the team outline their latest forecast changes and the political events on the horizon.

- Regional (and global) markets will be sensitive to US political news, global PMIs, US GDP/PCE data, and the BoC’s decision (25bps cut expected).

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Colombia, Mexico and Peru.

MARKET EVENTS & INDICATORS

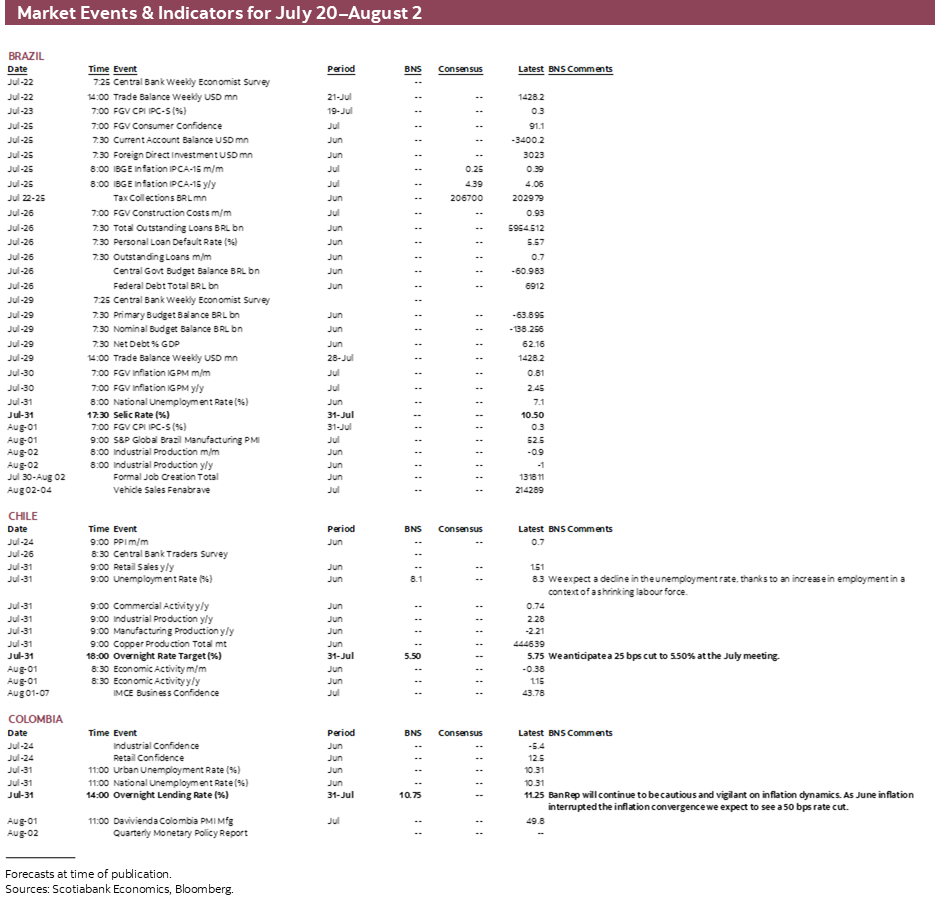

- A comprehensive risk calendar with selected highlights for the period July 20–August 2 across the Pacific Alliance countries and Brazil.

Chart of the Week

ECONOMIC OVERVIEW: MEXICO AND BRAZIL INFLATION, QUIET ELSEWHERE IN LATAM

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- Mexican and Brazilian mid-July inflation data is the highlight of a relatively quiet Latam week ahead. After recent losses, local rates could’ve benefitted from soft prices data, but that seems unlikely.

- In today’s report, our team in Colombia go over the country’s transformation over the past few years and their hopes for a return to a pre-pandemic Colombia. In Peru, the team outline their latest forecast changes and the political events on the horizon.

- Regional (and global) markets will be sensitive to US political news, global PMIs, US GDP/PCE data, and the BoC’s decision (25bps cut expected).

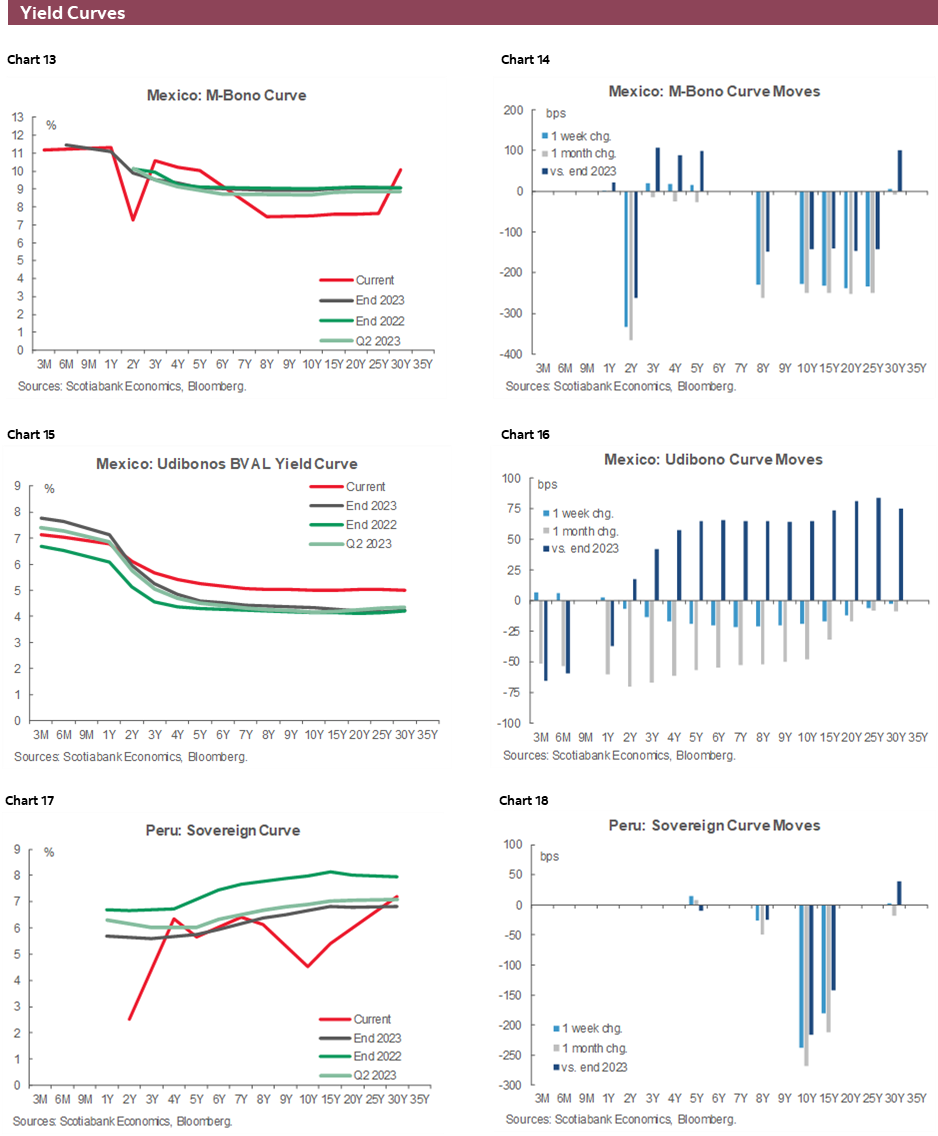

After a solid global rates rally on below-expectations US CPI last Thursday, key G10 debt broadly held on to this optimism over the past week, unshaken by the ECB’s non-event decision and even the assassination attempt on former President Trump last Saturday. The same cannot be said for Mexican and Brazilian rates that have had a rough few days, as the former are weighed by recent hot inflation prints and political risks (domestic and foreign) while the latter are dragged by fiscal concerns as President Lula remains uninterested in meeting fiscal targets.

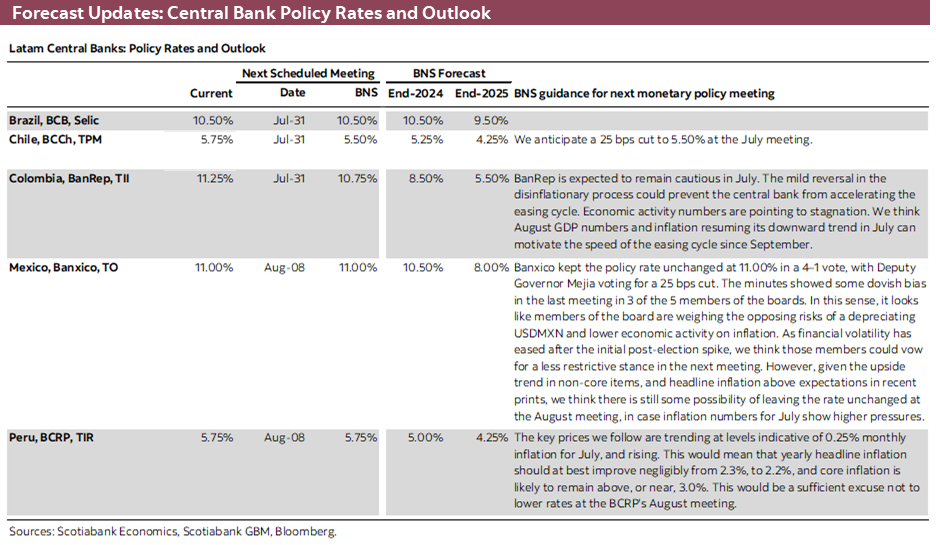

Mexican and Brazilian debt may correct or add to losses next week as both countries release mid-month inflation data that are the highlight of the Latam week ahead; Mexico also releases economic activity and retail sales data. Brazilian inflation is on an uptrend for the balance of the year owing to base effects, so we think the BCB is on hold for the time being, no hikes no cuts. The regional calendar is relatively quiet outside of Mexican and Brazilian data, and is thus unlikely to provide much direction for domestic markets. Regional markets will be sensitive to US election news (Biden possibly dropping out), a new set of global PMIs, US GDP/PCE data, and the BoC’s decision (25bps cut expected).

Chilean PPI and the BCCh’s traders survey are worth a look but we’re heading into the late-July decision with a strong sense that officials will cut by 25bps; next week’s releases have no chance of changing this. Colombian and Peruvian calendars are bare of anything of note, unfortunately. In today’s weekly, our team in Colombia go over the country’s transformation over the past few years and their hopes for a return to a pre-pandemic Colombia. In Peru, the team outlines their latest forecast changes and the political events on the horizon.

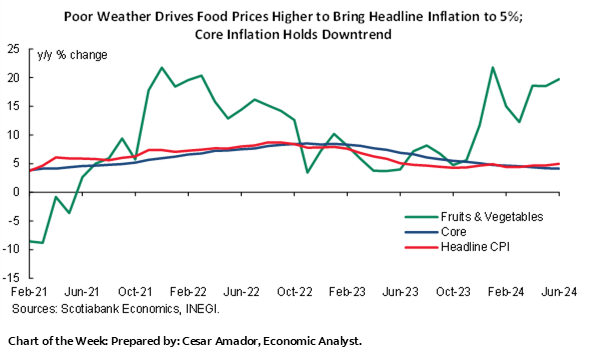

In today’s report, our Mexico team writes a preview of next week’s data releases. The H1-Jul CPI data out on Thursday is of greater importance than Monday’s economic activity reading (though weak growth is noteworthy), as economists and markets second guess August cut bets after the 5% y/y June headline inflation print. It’s not looking good for inflation trends in Mexico as rising fruits and vegetable prices challenge the anchoring of inflation expectations that Banxico so desires to feel confident about cutting again—a move that would be motivated by softening activity.

PACIFIC ALLIANCE COUNTRY UPDATES

Is Colombia Becoming Colombia Again?

Sergio Olarte, Head Economist, Colombia

+57.601.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Before the pandemic, the Colombian economy and its markets used to be rather predictable and stable, a country with some premium due to its lower financial deepening, but enough to ensure that FDI and portfolio investment were the main sources of financing for the structural 3% of GDP current account deficit. Headline inflation used to oscillate in the upper half of the target range, and inflation expectations usually hovered around the central bank’s target. GDP growth used to be at 3.50% on average, fiscal deficit and fiscal accounts ran a bit above peers but the country always complied with debt payments and controlled debt stock below 55% of GDP, with a strong tradition of having good credit. In fact, 1910 was the last time that Colombia went into default. Additionally, markets were not concerned about the institutional framework; checks and balances were practically axiomatic, BanRep autonomy worked, while the status-quo was never under discussion by investors.

After the pandemic, on top of the worldwide shock that hit economic activity and productivity across the globe, Colombia experienced an amplified effect that produced stickier headline inflation, material social discontent, and higher deterioration of the fiscal accounts, which resulted in a credit rating downgrade to become a non-investment grade country. In Colombia, inflation deceleration has been painful and too gradual; debt to GDP is way above its peers, and the fiscal deficit has failed to be reduced. More important and permanent, for the first time in recent history, there are many question marks around the possibility that pro-market institutions can change as President Petro explicitly has said that he prefers a central bank more aligned with government purposes, more intervention in the FX market, and greater debt to comply with his social programs, while wanting to restrict foreign participation in some businesses such as infrastructure, capital markets, healthcare, among others.

All of the above changed the market’s perception of risk in Colombia, while local assets became more volatile and are now operating at higher premiums. In the case of the Colombian peso, weekly volatility increased from 53 pesos before the pandemic to 92 pesos post-March 2020, and since June 2022 the average weekly volatility has been 106 pesos. On the fixed income front, the slope of the curve suggests a more significant pricing of the fiscal risk, while spreads vs. international references have also widened. This deterioration in assets and the increment in volatility change the way that agents see the Colombian economy. Investment decisions had to incorporate higher premiums due to uncertainty; portfolio investment also needed to adapt to less stable markets, while consumers had a hard time due to inflation and market reactions to the FX and rates.

That said, structural levels for financial assets changed and now involve higher risk premiums because Colombia is no longer an investment-grade economy but also because international rates are expected to stay structurally “high for longer”. However, fundamental variables are transitioning to a more predictable path and are converging to what they used to be before the pandemic. The institutional framework proved robust, and BanRep demonstrates independence and a rigorous approach in which they want to avoid surprise markets. Regarding macro variables, GDP has stagnated, but expectations point to a gradual recovery to an expansion speed of ~3%, below pre-pandemic standards. Inflation reduction is a matter of patience, as the indexation that took us to the highest inflation rate in the modern era is the same indexation that is taking us gradually to the target of 3% again, and inflation expectations are also anchoring gradually. If there is no further shock, Colombia gradually will become the Colombia we used to know again.

Mexico—Inflation and Economic Activity Preview

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Next week, two important indicators will be released in Mexico; bi-weekly inflation for the first half of July, and IGAE (economic activity) for May. During the year, headline inflation has outperformed consensus, showing an acceleration in the latest readings due to the rebound in agricultural and energy prices. On this occasion, we believe that fruits and vegetables will continue to lead the increase in prices, mainly due to adverse weather conditions. As a result, we believe that headline inflation will rebound to reach levels close to 5.4%, a level not observed since May 2023. On the other hand, the core component of inflation could continue its slowing trend, moderating its pace to 4.0%. In terms of monetary policy implications, we believe that the next decision on August 8th will be divided for a 25bps cut. The minutes of the last meeting noted that the Governing Board maintains a dovish tone, considering that the effect of lower-than-expected economic activity on inflation will be greater than the effect of the appreciation of the USDMXN after the elections. Nevertheless, the May IGAE (GDP monthly proxy) print could present a stronger annual pace, derived from the dynamism in services, offsetting the stagnation in industry and setbacks in manufacturing. Also, the minutes showed that the Governing Board consider the spike in non-core items to be transitory and highlighted that medium-term inflation expectations have remained somewhat stable. Thus, we believe Banxico will cut at the next meeting, despite setbacks in headline inflation in the coming print. However, any higher-than-expected number in core items such as merchandise and services could justify the case for a pause in August, moving the next cut to September.

Peru—New Economic Forecasts, Old Political Woes

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

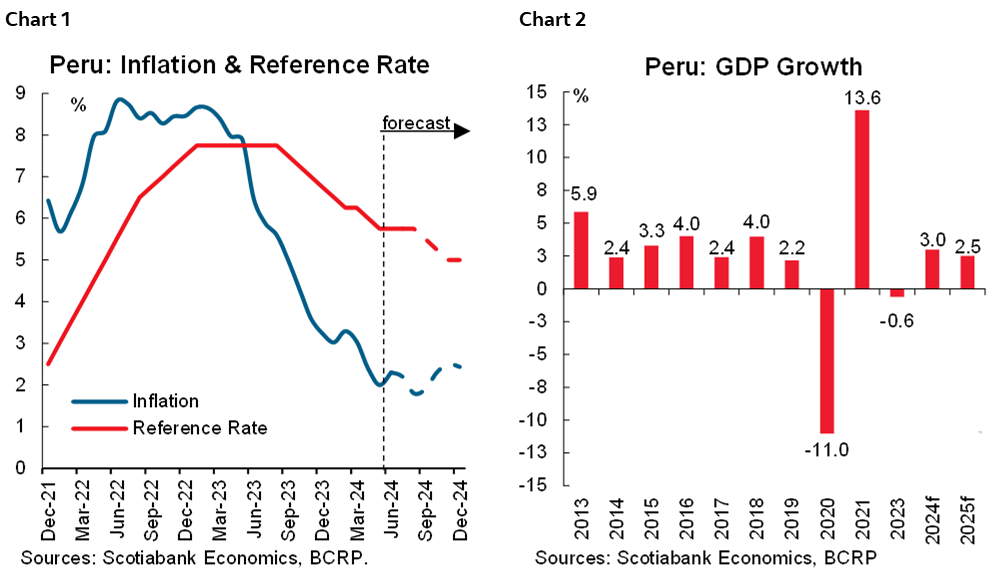

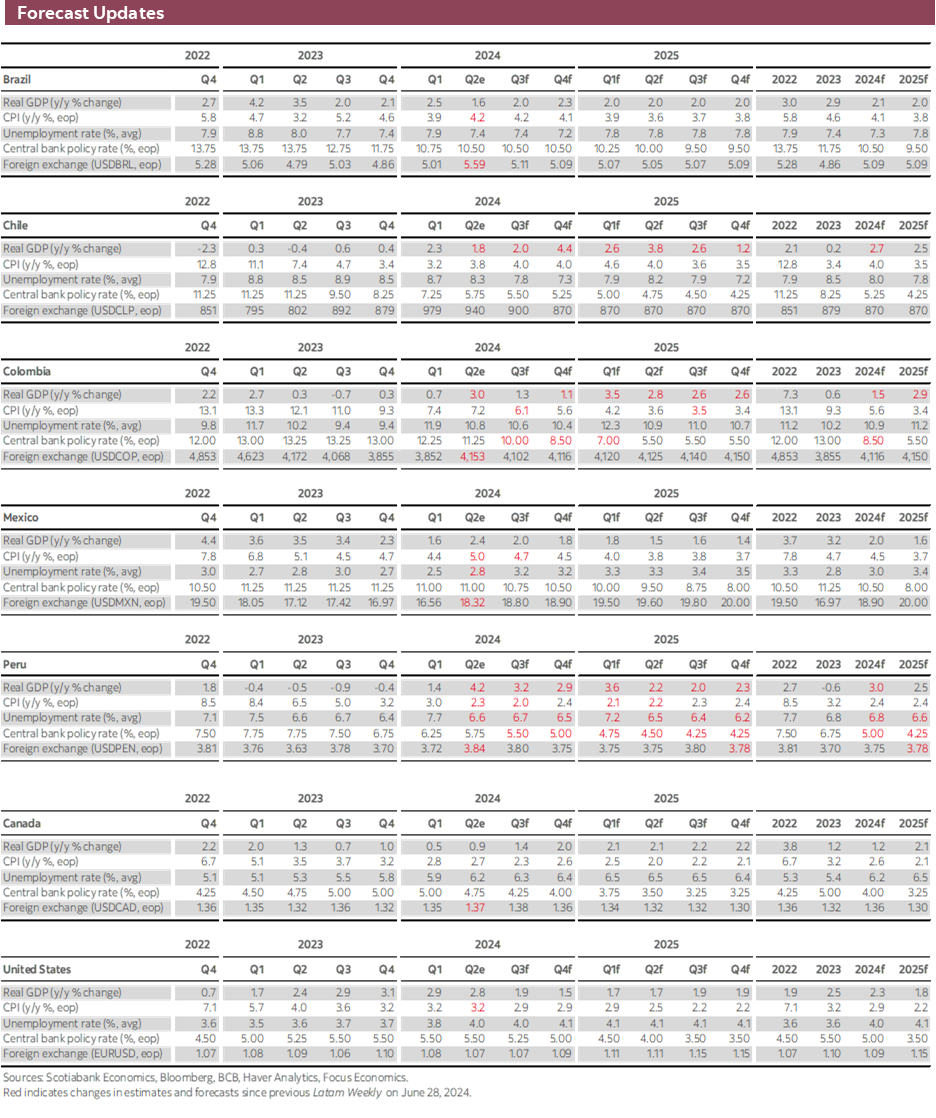

We are increasing our GDP growth forecast for 2024 from 2.7% to 3.0%. This is partially math, following higher-than-expected +5.0% growth during April–May, and partially reflects the impact on consumption that we expect after the legally-mandated AFP pension fund withdrawals beginning in July.

One might wonder whether growth in 2024 might not be even greater than 3.0%. The problem with this is that domestic demand continues to be low, especially private sector demand. The +5.0% growth figures for April–May were largely the result of a post-Niño rebound in agriculture and, especially, fishing. In June, with the fishing campaign much abridged, we expect growth to be much lower, somewhere between 2.0% and 2.5%.

Overall, we need to see three domestic demand-linked indicators show some vigor before we can be more aggressive in our growth expectations. These are cement sales (a proxy for private construction), industrial manufacturing (which strips away fishmeal processing) and loans growth in the financial system. All three were weak in May. For June, we only have data for cement sales, and these were down a discouraging 9%, y/y, for the month.

We have also mildly revised our BCRP reference rate forecasts. We had already raised our year-end 2024 forecast to 5.0% (from 4.75%). We are also now raising our year-end 2025 forecast to 4.25% (from 4.00%). The BCRP has signaled a number of times its discomfort with the idea of lowering the local reference rate to par with the Fed rate. We are inclined to believe that it will continue to avoid doing so. As a result, we expect the BCRP to maintain its reference rate at 5.75% once again in August.

Inflation would apparently help the BCRP to argue in favour of not moving its policy rate. The key prices we follow are trending at levels indicative of 0.25% monthly inflation for July, and rising. This would mean that yearly headline inflation should at best improve negligibly from 2.3%, to 2.2%, and core inflation is likely to remain above, or near, 3.0%. This would be a sufficient excuse not to lower rates at the BCRP’s August meeting.

On the political front, the next couple of weeks promise to be eventful. Much of the focus will be on the traditional July 28th Presidential address. July 28th is Peru’s Independence Day, and the yearly anniversary of each government’s regime. In the past this has been an opportunity for governments to announce novelties, and outline changes in strategy and policy. In recent years, the addresses have centered around more pedestrian topics, basically recounting what the government has done, and what is in the pipeline, little of which normally constitutes a novelty. The Boluarte regime has so far instated good State management on a day-to-day basis, but avoided strong novelty or policy statements. Given this behaviour, we do not expect anything too new in the July 28th address.

There is a chance, however, of a few changes in the cabinet. This has also happened in the past, every so often, although it is not a sure thing. The head of the cabinet, Gustavo Adrianzén, has stated that there will be no cabinet changes around this date, but this has not stopped part of the press from speculating that there might. Much of the focus is on the Minister of the Interior, of Health, and of Education. The Ministries most linked to the economy, such as Finance, Production, or Transportation seem safe (hopefully!).

On the frontier between the economic and the political, is the recent announcement by Southern Copper that it is going ahead with the large Tía María copper project. It is our understanding that certain peripheral works have, in fact, begun. This decision has, as expected, triggered voices of opposition, although so far, this opposition has been rather lukewarm. Having said that, the national labour union (CGTP, Confederación General de Trabajadores del Perú) has announced mobilizations on different dates from July 19th to July 29th, and one of the issues they have included in their platform is their opposition to Tía María. Many people may look at the magnitude of these mobilizations to gauge the extent of opposition to the project.

Meanwhile, political jockeying with an eye on the 2026 elections has begun, linked to the July 12th deadline for hopefuls to attach themselves to a political party. It is, perhaps, too early to read too much into who is who and what parties are doing what, but one news item has risen above the rest. Keiko Fujimori announced that her father, Alberto Fujimori, would run for president representing the Fuerza Popular Party. It is not clear whether he, as an ex-convict, is legally capable of doing so, however, and there seems to be a good chance that electoral authorities will legally block his candidacy.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.