RETURN TO SURPLUS DELAYED BY ONE YEAR IN STATUS QUO BUDGET

- A month before Premier Furey steps down, and ahead of a provincial election due this year, the Newfoundland and Labrador government tables a stay-the-course budget, with no new tax increases but also no significant new spending measures. The deficit is projected to rise this year before turning into surpluses going forward on the back of significant expenditure restraint and a significant pickup in economic activity in outer years. However, for all intents and purposes this is a placeholder fiscal framework that will be significantly impacted by the evolution of the trade war, the imminent provincial electoral cycle, and the final version of the agreement with Quebec on new hydroelectricity payments.

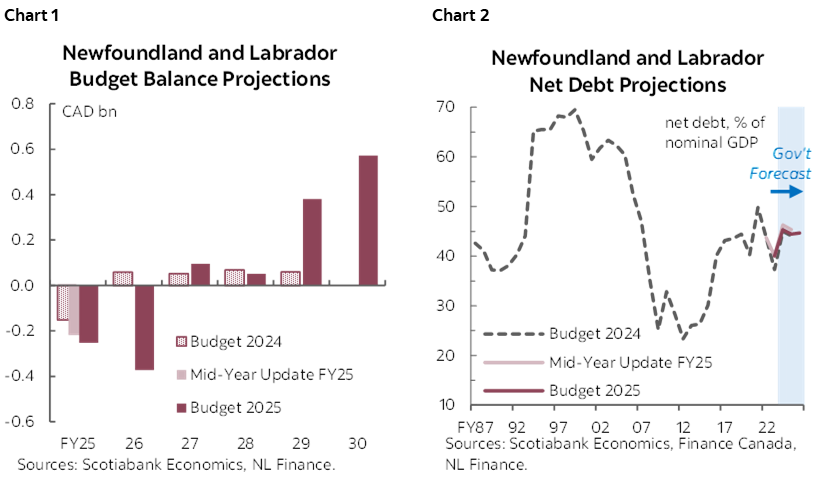

- Budget balance forecasts: the deficit is estimated at -$252 mn (-0.6% of nominal GDP) in FY25 and projected to expand to -$372 mn (-0.9%) in FY26, before returning to surpluses that are expected to increase from $96 mn (0.2%) in FY27 to $571 mn (1.0%) by FY30 (chart 1).

- Economic assumptions: real GDP growth of 6.7% in 2024, expected to slow to 4.4% in 2025 and 1.6% in 2026. Oil price of US$73 in FY26.

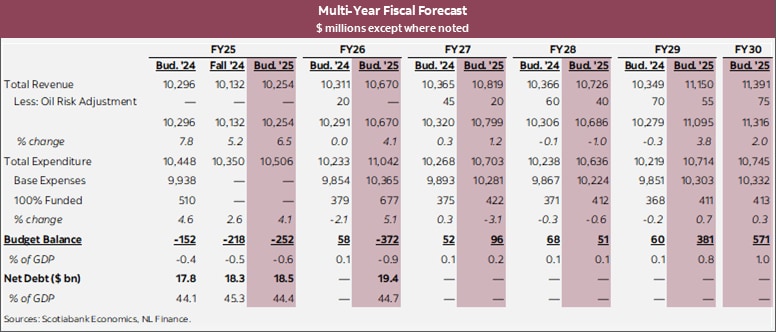

- Net debt: revised down to 44.4% of nominal GDP in FY25 versus 45.3% in the mid-year update, and marginally rising to 44.7% in FY26 (chart 2).

- Borrowing requirements: increasing from $2.8 bn in FY25 to $4.1 bn in FY26.

OUR TAKE

Newfoundland and Labrador’s Budget 2025 expects another deficit in fiscal year 2025–26 (FY26) before returning to surpluses that are projected to grow over most of the horizon. The FY25 deficit was revised higher to -$252 mn (-0.6% of nominal GDP) in FY25 compared to the mid-year update, primarily due to lower oil royalties and increased health care spending. The deficit is expected to increase to -$372 mn (-0.9%) in FY26, as total expenditure rises by 5.1% year-over-year versus a more modest rise of 4.1% for total revenue. Health spending is projected to be flat, and the largest increases are for the Executive Council and Municipal and Provincial Affairs departments. The government is also seeking spending authority from the legislature for $200 mn to cover unforeseen expenditures in FY26, but has not built this contingency budget into the fiscal outlook. As a result, any use of the contingency budget would add to the projected FY26 deficit.

To return to the black beginning in FY27, ambitious spending restraint is projected for future years, including expense decreases in both FY27 and FY28. Revenue is projected to grow by an average 2% from FY26 through FY30, though pick up in the outer years as large new capital projects get underway. A worsened economic outlook owing to an extended trade war would pose headwinds to achieving this outlook, but there is potential for significant revenue windfalls from the Churchill Falls memorandum of understanding announced with Quebec in December 2024—hoped to be finalized next year.

The economic forecasts assumed for the outlook incorporate the negative impacts of tariffs imposed on Canadian goods entering the US and China, according to the budget. Provincial real GDP growth is projected to be 4.4% in 2025 and 1.6% in 2026, down from 6.7% in 2024. While growth is expected to slow over the next two years in the face of tariff and trade headwinds, the budget notes real GDP growth is projected to remain positive primarily due to increased oil and mineral production, with brent crude oil prices averaging US$73.90 per barrel in 2025. However, given the volatility and rapid pace at which the tariff environment is changing, the risks to the near-term outlook are likely more heavily weighted towards the downside.

Net debt levels are estimated to be $18.5 bn in FY25, higher than the $18.3 bn projected in the mid-year update. However, net debt as a share of nominal GDP in FY25 is estimated at 44.4% as opposed to the 45.3% presented in Fall 2024 owing to higher nominal GDP growth. Net debt levels in FY26 are projected to increase to $19.4 bn but only marginally increase to 44.7% as a share of GDP owing to slowing but still positive growth in economic activity.

Gross borrowing requirements are projected to rise to $4.1 bn in FY26 from $2.8 bn in FY25. This mainly reflects a significant increase in debt to be retired this year, but is also impacted by the higher deficit, an uptick in capital spending, and a prudent increase in planned cash holdings.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.