READYING FOR RECOVERY AFTER AVOIDING THE PANDEMIC’S WORST

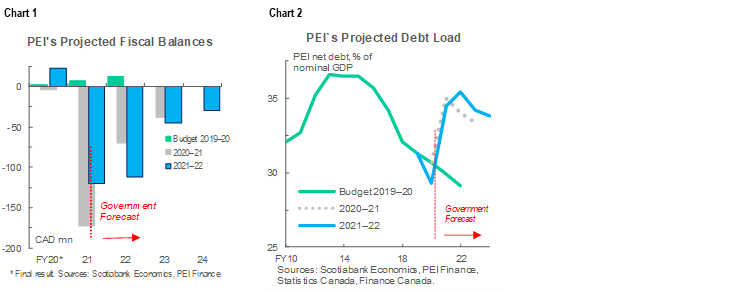

Budget balance forecasts: -$112 mn (-1.5% of nominal GDP) in FY22, -$46 mn (-0.6%) in FY23, -$28 mn (-0.3%) in FY24—all slightly wider than expected in the June 2020 budget (chart 1).

Net debt: expected to edge up to 35.4% in FY22, then ease to 33.8% by FY24—slightly higher than forecast in last year’s budget (chart 2).

Nominal GDP growth: -6.6% in 2020 and +5.8% this year—consistent with the provincial economy reaching pre-pandemic output level in late FY22 or early FY23.

Borrowing: $276 mn in FY22 of which $200 mn is long-term, $475 mn forecast for FY21 roughly evenly split between short- and long-term sources of cash.

We assess Budget to be a credible plan that maintains PEI’s healthy fiscal position relative to most other Canadian jurisdictions and sets up recovery.

OUR TAKE

Like virtually every economy around the world, Prince Edward Island has had its fiscal position eroded by COVID-19 over the last year. According to the Island’s latest projections, a return to black ink will not occur until after FY24; that contrasts sharply with the surpluses planned through at least FY22 as of the last pre-pandemic budget.

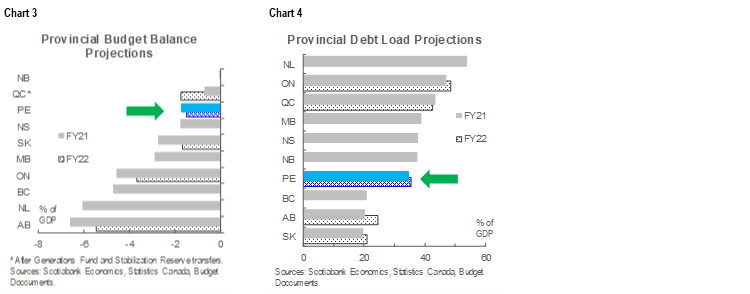

Relative to other jurisdictions, however, the Island’s finances are in good shape. Deficits of about 1.5% of provincial GDP in FY21–22 are among the lowest forecast by any subnational government in Canada thus far (chart 3, p.2). Ditto for net debt, despite the increase as a share of output expected in FY22 (chart 4, p.2). These figures reflect a strong fiscal position entering the pandemic, early and decisive action that helped quell the spread of COVID-19, and the natural advantages of Island status. PEI’s modest economic contraction relative to other jurisdictions in 2020 is well-established, and Budget noted a number of economic indicators for which PEI’s results far outperformed the national average in 2020.

Policy supports in the budget look appropriately targeted. Funds to recruit and retain nurses and nurse practitioners and efforts to expand use of virtual technology in the health care system seek to address the labour and care delivery challenges exposed by the pandemic across the world. Plans to designate new child care spaces and reduce related costs target higher labour force participation among working parents. A further cut to the small business tax rate should help reduce costs as firms relaunch their operations. Grants that subsidize reopening costs for tourism businesses in 2021 acknowledge the particularly challenging outlook for firms within one of the Island’s key sectors. The Province also announced plans to boost infrastructure outlays late last year.

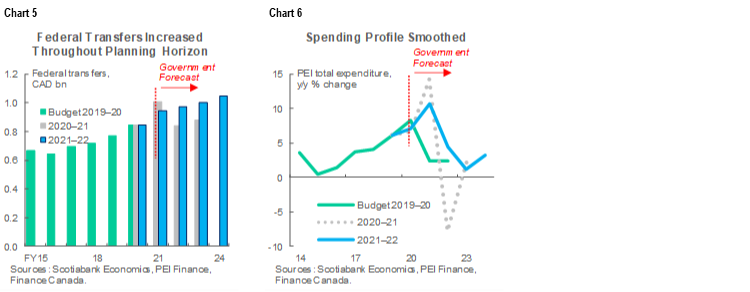

A planned increase in federal funding unlocks greater spending potential for the Island. The fiscal plan released in June 2020 assumed that transfers from Ottawa would surge by more than 20% in FY21, then retreat at a roughly equal rate the next year as pandemic support waned. By contrast, this year’s plan is built on average annual transfer growth of 3.5% during FY22–24, which puts FY22–23 revenues from federal sources on track to exceed the prior plan’s levels by more than $250 mn (chart 5, p.3). With the benefit of those funds, the province has pencilled a 4.4% climb in total expenditures into FY22—presumably reflecting the cost of new programs and policies—which compares to a 7.8% cut planned as of the June 2020 fiscal blueprint (chart 6, p.3).

Economic projections underlying Budget appear reasonable and consistent with prudent fiscal planning. Our most recent PEI economic forecast assumes real growth stronger than the private sector average noted within the document, but was completed following the passage of additional US stimulus and already incorporates some Canadian fiscal support in the spring. To the extent that our more optimistic national-level expansion unfolds, the Island may see some budget balance upside.

Population growth remains a key question mark with mobility limited and travel restrictions still in place. PEI witnessed the strongest headcount gains of any province in Canada during the years leading up to the pandemic, and those gains were anchored by the attraction and retention of skilled newcomers. Population projections underlying the fiscal plan—discussed in the budget paper and released in the prior week—are feasible, but acknowledged to be tilted towards the optimistic end of the range of standard Statistics Canada scenarios (chart 7, p.3). The Province assumes that immigration levels will return to their long-run trend by the end of 2021.

Cash requirements for FY22 are forecast to amount to $276 mn, of which $200 mn is expected to be apportioned to long-term borrowing. For FY21, the projected total is $475 mn—about $15 mn more than anticipated in the June 2020 budget—which includes $250 mn in long-term borrowing.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.