Late-2020 data suggest strong underlying momentum in Canada and the US despite the surge in the virus. Combined with conservative assumptions on the passage and impact of the American Rescue Plan in the United States, this leads us to raise our forecasts for real GDP growth in 2021 to 5.3% for Canada and to 5.8% in the US.

COVID remains a clear and present danger to the economy despite the (disappointing) vaccine rollout and will hold back economic activity in the first months of this year. A strong rebound is expected once we see sustained progress in controlling the virus.

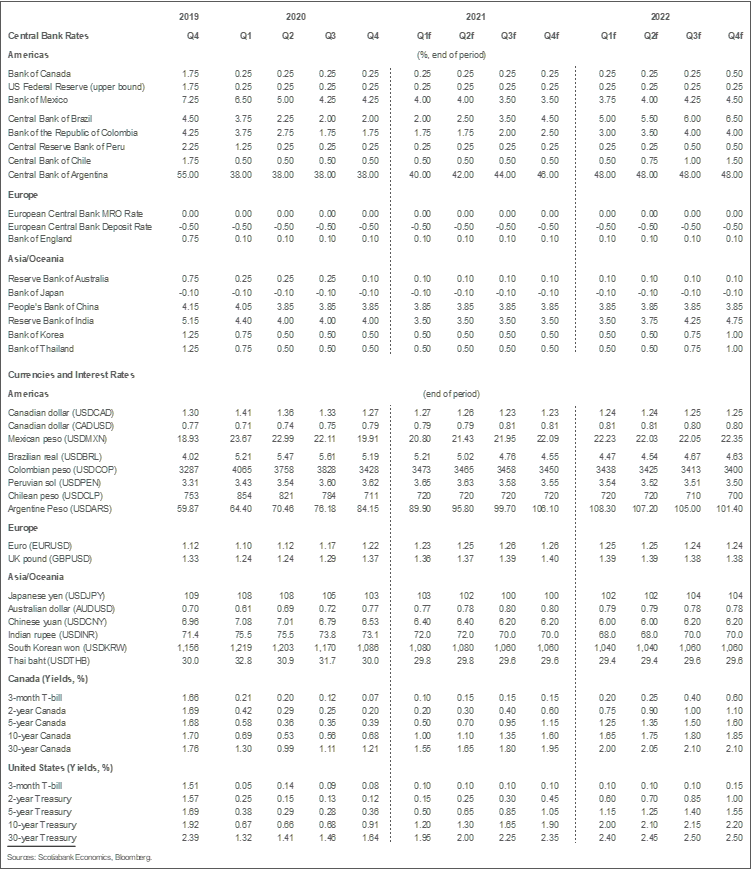

Indications from the Bank of Canada and the Federal Reserve that policy rates will remain on hold until 2023 and 2024, respectively, seem overly cautious. We think the Bank of Canada will taper its quantitative easing program more aggressively around mid-year and raise interest rates in 2022Q4. The Fed seems more likely to raise rates mid-2023 than in 2024. In both countries, a more pronounced steepening of the yield curve is expected over the next two years.

Major increases in our 2021 Canadian and US forecasts are in order. The final quarter of 2020 revealed that both economies were significantly more immune to the surge in COVID and associated containment measures than earlier anticipated. The parameters of President Biden’s fiscal plan are also becoming clearer, so we are now including an additional USD1 trillion in US fiscal spending. We had already incorporated USD400 billion of spending in anticipation of President Biden’s fiscal plan, bringing the total assumed spend in our forecast to USD1.4 trillion. This leads to a jump in our forecast for US growth in 2021 to 5.8%, well above the 5.0% we predicted in our January update. In Canada, the growth surprise at year-end suggests much stronger momentum going into 2021. This is leading to a particularly large revision to the growth outlook in Canada, which is further boosted by a stronger forecast for the US economy. We now forecast an expansion of 5.3% this year.

In both countries, several drivers of growth support the strong growth forecast:

- Equity markets are generating substantial wealth effects. These markets don’t appear to be richly priced given the growth and interest rate outlook, so these wealth effects are unlikely to be sustainably reversed in the near-term.

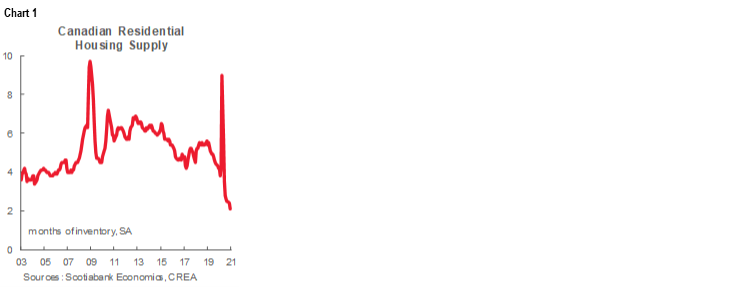

- The same is true for housing on both sides of the border, with owner’s equity rising in recent quarters. In Canada in particular, the housing market remains even more undersupplied (chart 1) than it was pre-pandemic, suggesting recent gains in home prices are sustainable. January home sales already suggest the year is off to a very solid start.

- Commodity prices have risen significantly in light of improved growth performance in China in particular, but they also reflect a generally more positive global outlook for the year. Higher commodity prices are another form of wealth shock for the Canadian economy.

- We have built into our forecast an additional CAD20 billion in fiscal support in Canada in the Spring budget as part of the yet-to-be-announced Build Back Better plan. In the US, there is a risk of even more supportive fiscal policy than assumed in this forecast. President Biden may well implement his proposed USD1.9 trillion fiscal plan. We are only assuming USD1.4 trillion in this forecast. Moreover, we are attaching a relatively low multiplier on this fiscal impulse—0.25—meaning that GDP rises by $25 for every $100 spent. In its review of the CARES Act, the CBO estimates the multiplier of that stimulus to have been 0.58, more than double what we assume in this forecast.

- Canadian firms and households are sitting on extremely high levels of deposits and there is clear evidence of pent-up demand. On the household side, the most recent data for November reveal personal deposits are CAD141 billion higher than they were a year ago. These deposits will eventually fall. The timing and speed of that is unknown, but we assume that it will occur once there is more clarity on the COVID front in the next couple of months. It is also unclear how those savings will be drawn down. Some will no doubt go to consumption of goods and services, but it may also be that a portion of these savings end up being invested or used to pay down debt. Given the resilience of spending on non-COVID-affected areas, it is safe to assume that spending on travel, food, accommodation and entertainment will particularly benefit once those activities are more easily undertaken.

Downside risks remain important, of course. We are still dealing with COVID. The virus is evolving and there are risks that vaccines may prove ineffective against some of these variants. Likewise, vaccine rollout globally is proceeding more slowly than desired. We cannot rule out additional infection surges until herd immunity is achieved. If future COVID waves were to occur, we might need to scale back our forecasts. Then again, we are being very conservative on the impact of the Biden fiscal plan and that offsets much of these virus-related risks.

The revised outlook in both countries suggests that central bank projections to maintain rates at current levels until 2023 in Canada and 2024 in the US may be overly cautious. Very simplistically in the US, GDP growth fell by 3.5% in 2020 and should grow by almost 6% this year. The shock, at an aggregate level, will be completely undone this year if the virus is reasonably contained. This will also be the case in Canada. The output gap could be closed as early as 2021Q3 in the US and 2021Q4 in Canada. From a policy perspective, these developments will need to be weighed against the scarring from last year. Unemployment rates will be well above pre-pandemic levels for much of the next two years. Firms in many industries will struggle until COVID is well and truly in the rear-view mirror. The balancing of powerful growth dynamics against risks to the outlook and ongoing economic repair will be a challenge for central banks this year. They will not want to trigger a premature tightening of financial conditions by sounding overly optimistic.

Nevertheless, we think economic conditions over the next few quarters will justify an earlier rate increase than currently projected by the Bank of Canada and the Federal Reserve. In Canada, we are pencilling in a first increase in 2022Q4. Before that happens, we assume the Bank of Canada will next taper its quantitative easing program around the middle of this year—once most COVID-related risks dissipate. In the US, our current view is that the Fed Funds target rate will rise mid-2023. In both countries, we expect the yield curve to steepen well ahead of the move in the policy rate and expect 10-year government bond yields to hit 1.6% and 1.9% in Canada and the US, respectively, by the end of this year.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.