- Chile: GDP recorded zero year-on-year change in September

- Peru: Inflation surprises lower again; September growth indicators are mixed

Closed Japanese markets and only a Caixin Chinese PMIs miss on the data front meant mostly range-bound trading overnight, leading up to a European morning that also only had second-tier releases to count down the hours until US and Canadian jobs data. BoE chief economist Pill speaks at 8.15ET to give us some more colour on the bank’s new forecasts in yesterday’s MPR and maybe express his bias on the odds of another hike or how long they may remain at the current 5.25% bank rate (see our recap here). Fifteen minutes later markets will forget about what Pill is saying to focus on US and Canadian jobs data which are the G10 highlight followed by US ISM data.

The risk-mood is pretty much as North American markets left it, but disappointing earnings results from Apple have Nasdaq futures down 0.3/4% against a marginal drop in SPX contracts—and this comes after Thursday gains of 1.8/9% in the indices so it’s only a scratch. The SPX is tracking a nearly 5% rise since Friday thanks to a combination of relatively benign BoJ, Fed, and BoE decisions, UST issuance plans undershooting long-end sales expectations, only mixed data, and an internalising of Middle East risks. This ~5% gain would mark the SPX’s best week since November 2022, though there’s still a challenging downtrend from the July peak that is coming into view.

USTs opened a few hours ago around where they closed yesterday with a very slight bear steepening bias after a 5bps flattening in 10s30s yesterday. Commodity prices are not doing much. Oil is down a touch, with a sharp $1 move in WTI in the last hour on nothing obvious, that is also tracked by copper’s 0.4% fall while iron ore is 0.2% firmer.

On the FX front, moves are small too, the USD is up/down 0.2% against most majors and there’s no obvious trend overnight—if at all maybe a bit of a USD-negative mood ahead of US hours. The BBDXY’s decline of 0.8% on the week is its largest since mid-July. The MXN is holding to a very narrow range just above the 17.50 mark as the cross closed on Thursday below its 50-day MA for the first tine since late-August, a firm break of the mid-figure zone leaves a mostly unobstructed path to the 17 pesos level (with the 100-day MA at 17.3170 standing in between).

It has certainly been a good week for Latam FX, with gains ranging from 5% for the CLP (thanks to the BCCh’s announcement last Thursday) to 1.2% for the BRL (MXN +3.5%, PEN +2.3%, COP +1.5%). In fact, the CLP, MXN, and PEN are all in the top five expanded major currencies this week against the USD.

Brazilian and Mexican markets reopen today after holidays on Thursday, but the Latam day ahead has little major to drive price action. Mexican gross fixed investment data out at 8ET is the data highlight where we’re watching the evolution of investment as far as nearshoring may be concerned—so far, the bulk of the surge in investment spending has been in public infrastructure projects. BanRep’s meeting minutes out at 18ET may be the most interesting release in the region today, as economists and markets debate whether Colombia’s central bank may wait until next year to cut rates. Alas, the late release time means local markets will only be able to react until the next market open, which isn’t until Tuesday given the holiday closures on Monday.

—Juan Manuel Herrera

CHILE: GDP RECORDED ZERO YEAR-ON-YEAR CHANGE IN SEPTEMBER

- Positive surprise in terms of y/y GDP growth, although non-mining sectors disappoint at the margin

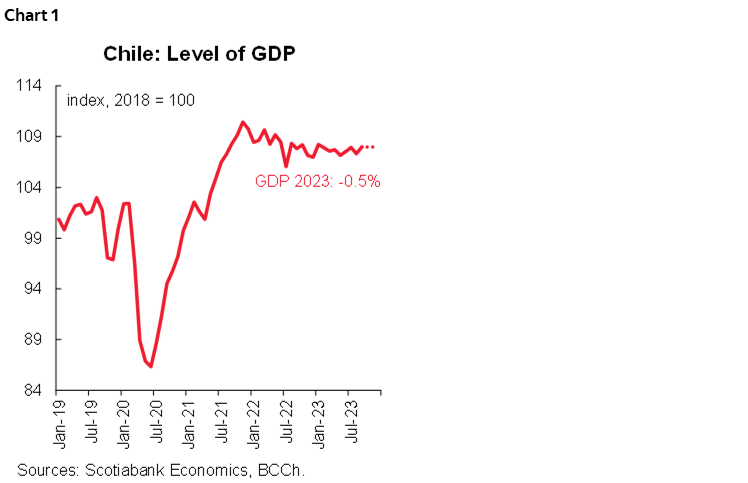

On Thursday, November 2nd, the Central Bank (BCCh) released the September GDP, which registered a null y/y variation, positively surprising market expectations (Economists’ Survey: -0.6; Bloomberg: -0.5%) and ours (-0.8%). However, the dynamism of non-mining activity was only 0.2% m/m (SA), below our expectations, disappointing in almost all economic sectors. The surprise then came from the seasonal factor, accounting for a better-than-expected calendar effect. Along these lines, services grew by only 0.1% m/m and commerce showed a 0.7% m/m drop, while mining grew by only 2.9% m/m. Given this negative surprise in the monthly rate, despite the positive y/y record, we maintain our projection of a 0.5% decline for GDP in 2023 (chart 1), somewhat below market expectations.

Better-than-expected y/y GDP, concentrated in mining and electricity generation. With respect to the previous year, the main positive contribution came from the mining sector, although the value added provided by electricity generation also made a relevant contribution. In contrast, commerce, services and industry experienced y/y declines that completely offset the growth in goods GDP. This was reflected in the 1.2% y/y fall in non-mining GDP, which would have accumulated a contraction of 0.4% y/y in the Q3-23.

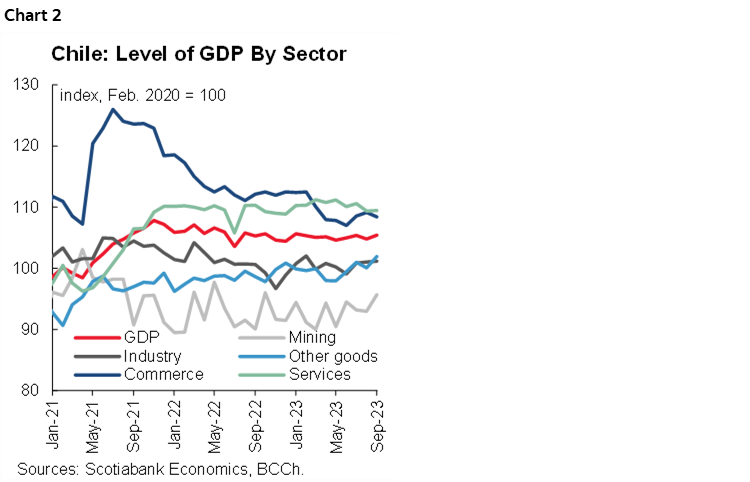

At the monthly level, GDP registered a growth of 0.6% m/m, positively impacted by the recovery of mining production and to a lesser extent by factors that we estimate to be transitory. Regarding non-mining activity, we highlight the low dynamism registered by the services sector, where the rebound in education activity (Personal Services) was almost entirely offset by a deterioration in business services (linked to investment) and transportation services (chart 2). Although the Q3-23 preliminarily closed with a better dynamism than the previous quarter, we do not see relevant factors contributing to the dynamism in the Q4, as the transitory factors (weather factors in electricity generation) that contributed to the dynamism in Q3 would not be present in the last quarter of the year.

—Aníbal Alarcón

PERU: INFLATION SURPRISES LOWER AGAIN

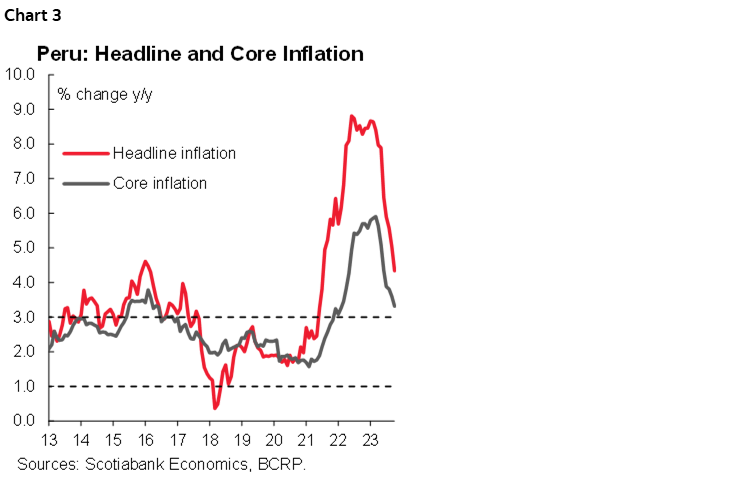

Inflation continues to surprise downwards. The Lima CPI fell -0.32% m/m, below all forecasts, including the market consensus (+0.19% according to Bloomberg survey), Scotiabank (+0.10% according to our last update) and the historical average of the last 20 years (0.17%). With this, year-on-year inflation continued to slow, going from 5.0% to 4.3%, reaching its lowest rate since July 2021.

The inflation surprise in October came from the reversal in the prices of some perishable foods and poultry prices greater than we expected and which together contributed to a decrease of 0.66 percentage points (only in five prices).

The effects of El Niño on prices appear to be moderating even though the probability of a moderate/strong El Niño scenario for the coming months rose from 88% to 96% in the most recent reading.

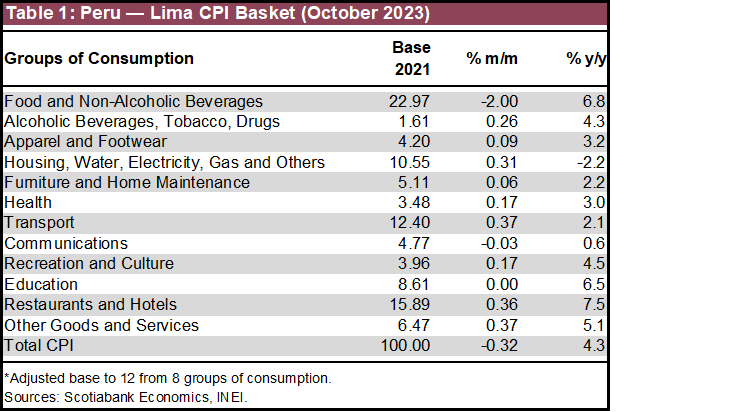

With inflation data from October, there are 29 months in which inflation remains above the upper limit of 3% of the inflation target (table 1). Inflation at the national level (not just in Lima) went from 5.3% to 4.5%, exceeding Lima’s inflation for 26 consecutive months. In October, of the 586 products that make up the consumption basket (2021 base), 316 increased (54%), 149 decreased (25%) and 121 remained unchanged (21%), similar proportions to those posted in September reflecting that the slowdown in inflation is concentrated in a few products with a high weighting in the basket but remains structurally slow.

Core inflation rose 0.22%, above its historical average (0.14%, last 20 years). In year-on-year terms it went from 3.6% to 3.3%, slowing for the seventh consecutive month and in line with what we expected (chart 3). Cost pressures remained low, with year-on-year variations close to zero. The PEN continued to depreciate in October, although in year-on-year terms it accumulated an appreciation of 3%.

Looking ahead, we expect inflation to continue to decline in November, approaching 4%. The comparison base effect will play in its favour since inflation in November 2022 (0.52%) was relatively high for the historical average for the months of November (+0.10). However, factors such as higher wholesale inflation, the depreciation of the PEN and the lagged effects of rising oil prices could put upward pressure on headline inflation. We recently reduced our inflation forecast from 5.0% to 4.6% by the end of 2023. The reduction could have been greater had we not considered a strong El Niño scenario that we expect for the following months.

The BCRP indicated that inflation was affected by temporary supply factors and expects the correction of food prices to continue in 2024 in a moderate El Niño scenario, although they warned of their concern about the probability of a strong El Niño scenario. With this result, we predict that the BCRP would continue to cut its key rate by 25bps to 7.00% at its meeting on Thursday, November 9th.

—Mario Guerrero

PERU: SEPTEMBER GROWTH INDICATORS ARE MIXED

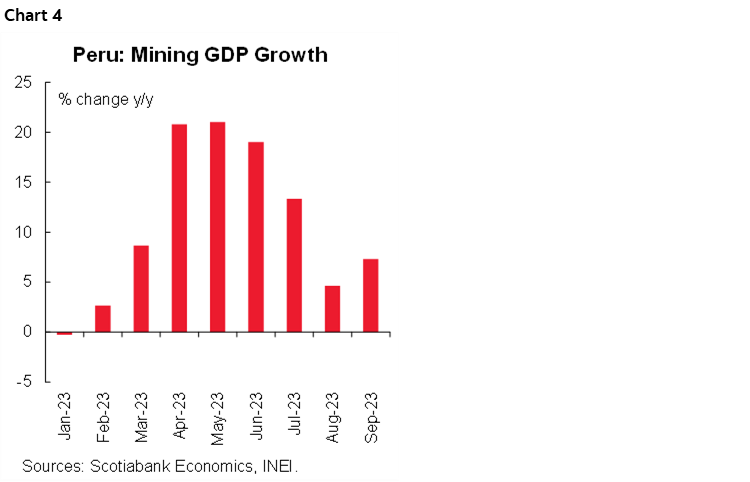

Advance indicators for September GDP growth were published on November 2nd. The information was mostly positive. Mining GDP rose 7.3% y/y. This was quite good, especially considering that the new Quellaveco copper mine had already come on stream in September 2022. In fact, copper output itself was only up 2.0% y/y, and it was other metals, namely molybdenum (41% y/y) iron (25%), gold (13%) and zinc (8.6%) that led the way in mining growth. Even more impressive was the 19.6% increase in Oil & Gas, although the sector doesn’t really have enough weight in global GDP to make too much of a difference (chart 4).

Fishing GDP rose 17%, y/y, in September. Here again the weight is low. However, the positive aspect is that the figure contrasted with the El Niño-induced huge negative growth of earlier months.

Electricity growth of 3.1% y/y was mildly hopeful. Mining companies are strong demanders of electricity, so the new Quellaveco operations had been distorting the y/y growth figures. However, this base factor has largely ended, and electricity growth is once again more indicative of GDP growth.

That’s the good news. The bad news is that domestic cement consumption fell 10.5% y/y in September, with negative growth dipping back into double-digit figures, which is quite a disappointment after much softer declines in August (-9.5%) and July (-5.6%).

September GDP growth will depend more on domestic-demand sectors such as industrial manufacturing, services and commerce, but these tend to be a bit less volatile. Our main concern is industrial manufacturing. We need industrial manufacturing performance to improve for positive GDP growth to be more secure. However, having said this, if we take the recently published indicators all together, September GDP should outperform the dismal growth figures of the previous months. Furthermore, there is a good possibility that growth will not be negative, although it will be low. Peru is coming out of a long negative growth period lasting three quarters very slowly and with insufficient conviction. Moreover, positive growth is barely starting to raise its head just as another El Niño looms on the quickly approaching horizon.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.