- Mexico: Inflation grazes 5% due to rise in agricultural prices; Consumer confidence improved in June, but remains in contraction

- Peru: New car sales should recover in H2-24

MEXICO: INFLATION GRAZES 5% DUE TO RISE IN AGRICULTURAL PRICES

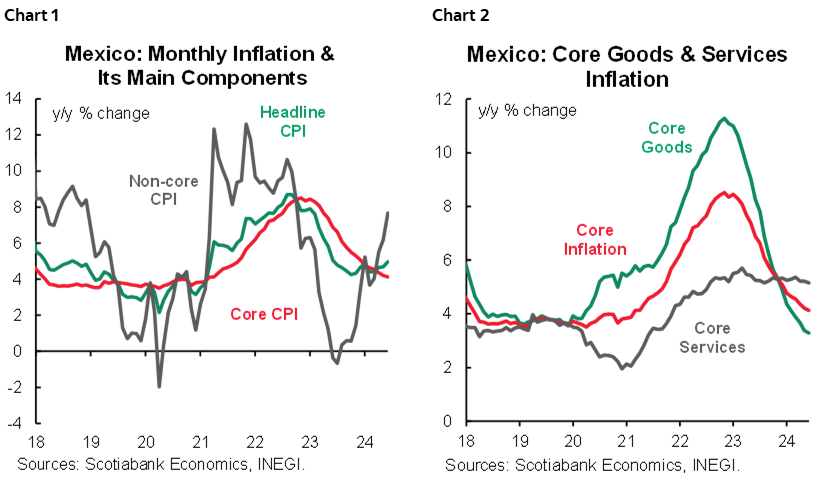

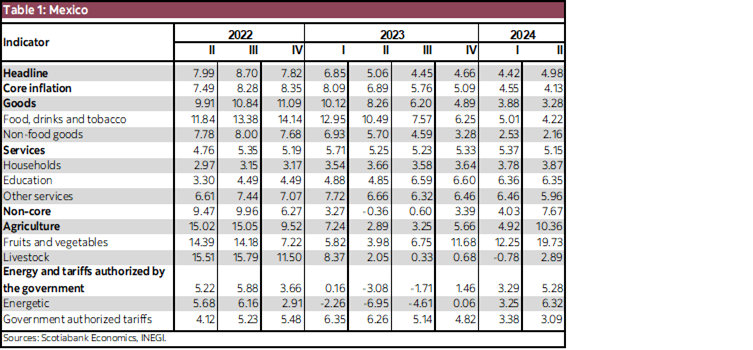

Inflation rose to 4.98% in June from 4.69% (vs. 4.84% consensus), core inflation moderated to 4.13% from 4.21% (vs. 4.24% consensus). Merchandise decelerated 3.28% (3.38% previously), and services fell to 5.15% (5.22% previously). On the other hand, non-core inflation showed a strong increase of 7.67% (6.19% previously), highlighting agricultural inflation that rose 10.36% (8.44% previously). In its monthly comparison, headline inflation rose 0.38% (-0.19% previously, 0.24% consensus), the core component 0.22% (0.17% v, 0.24% consensus) and non-core 0.87% (-1.28% previously), see chart 1.

In detail, the product with the highest monthly impact on inflation was chayote, which rose +128.6% m/m, followed by oranges +31.4%, while on the decline, tomato stood out -12.8% and Serrano chili -27.02%. The state with the greatest prices increase was Oaxaca, and the one where prices decreased the most was Zacatecas.

The monthly increase in prices came from the most volatile components, mainly due to fruits and vegetables, affected by climatic phenomena (now hurricanes), and problems in the local supply chain. The good news comes from core inflation that continues to decelerate, although at a slow pace, supported by merchandise (table 1). These data overall challenge Banxico’s governing board regarding a possible cut in August, given annual inflation aims to return to a five handle.

CONSUMER CONFIDENCE IMPROVED IN JUNE, BUT REMAINS IN CONTRACTION

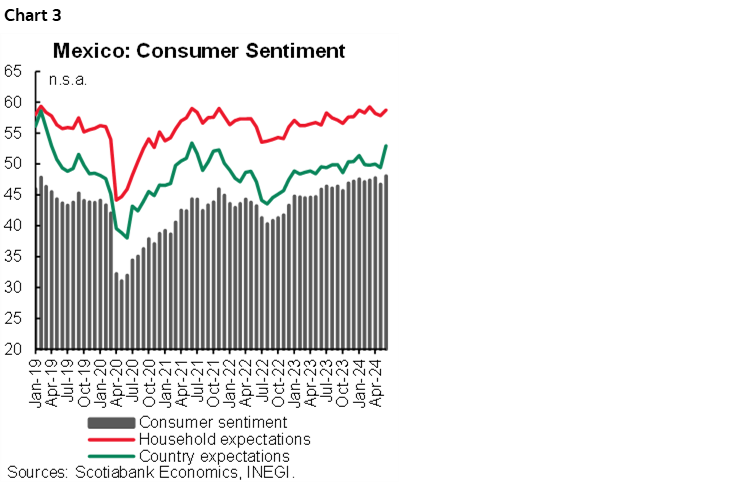

In June, consumer confidence rose to 47.5 points (vs. 46.9 previously) with seasonally adjusted series, remaining in contraction territory. Inside, two of its five components showed a monthly drop. The current situation of households fell to 52.4 (-0.2 points), household expectations rose to 58.5 (+0.9 points), both remain in positive. The country’s current economic situation 44.0 (+1.4 points), while the country’s expectations increased to 52.1 (+2.0 points). Finally, the possibility of purchasing durable goods fell to 30.5 (-0.9 points). The indicator shows that the consumer has seen a significant improvement in both the household economy and the country in general, since three components exceed 50 points (chart 3).

—Brian Pérez

PERU: NEW CAR SALES SHOULD RECOVER IN H2-24

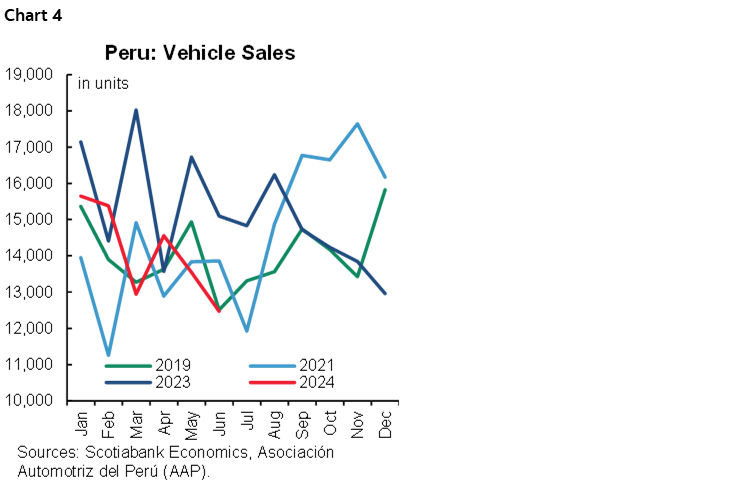

New car sales are expected to recover in the second half of the year. Our optimistic outlook is based on the projected recovery in domestic demand, which is expected to grow around 3% during H2-24. Furthermore, considering that auto sales in H2-23 fell by around 2% compared to H2-22 and that, on a half-year basis, sales were the lowest since H1-21, we expect a positive base effect. Furthermore, the gradual improvement in employment and purchasing power, together with lower inflationary pressures, could encourage the purchase of light vehicles. Finally, the availability of extraordinary income—CTS and pension funds—could be used as advance payments to acquire light vehicles in the second half of the year. As a result, we anticipate that new vehicle sales will increase by approximately 5% in H2-24.

Likewise, we expect that annual sales of vehicles—light and heavy—will be close to 177 thousand units. Although this level would be 3% below 2023 sales, if achieved, it would be the third highest since 2017 (180,281 units). By segment, although light vehicle sales in H2-24 would exceed H2-23 sales, according to our projections, this would not offset the lower sales in H1-24 (chart 4).

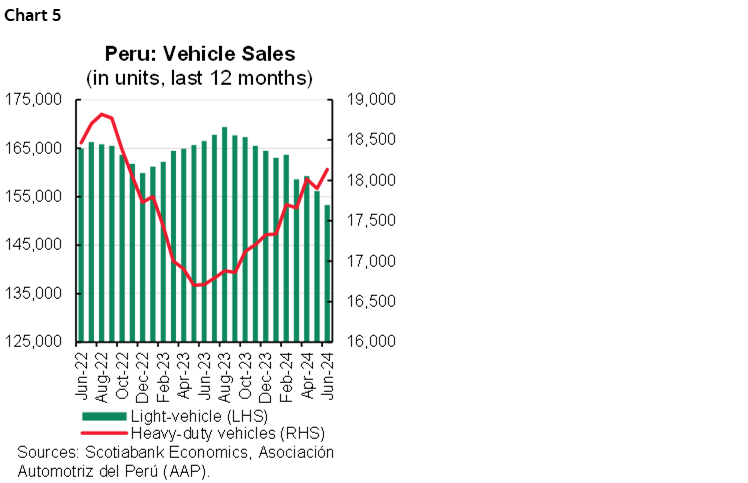

We project light vehicle sales to reach around 159,000 units in 2024, representing a decrease from the 2023 figure. In contrast, sales of heavy -duty vehicles are expected to increase, following the recent trend. It is projected that these sales will reach close to 18,000 units by the end of 2024, representing an increase over the 2023 result (chart 5).

CAR SALES IN H1-24

During H1-24 auto sales declined 11% y/y, according to Automotive Association of Peru (AAP). This drop was largely attributed to lower demand for light vehicles in H1-24 (-13% y/y). The drop in sales is linked to the weakening of household spending, in line with slight job creation and a slow rebound in private investment in Q1-24 (+0.3% YoY). However, this drop was partially offset by an increase in heavy -duty vehicle sales in H1-24 (+10% y/y). This increase was driven by higher demand for buses in tourism and private transport, as well as heavy-duty vehicles for mining and construction operations.

—Carlos Asmat

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.