Overview

- Key Insights from Customer Transactions

- COVID-19, the Canadian Economy and Scotiabank’s Transactions Data

- Business Transactions Data Details

- Retail Transactions Data Details

- Other High-Frequency Indicators of Activity

1. Key Insights from Canadian Customer Transactions

This presentation is part of the weekly series intended to draw insights about the state of the Canadian economy from the flow of Scotiabank’s retail and non-retail transactions data.

Key takeaways from the payments data in this week’s publication:

- Updated to October 29th, y/y growth of transactions in the business sector has been relatively stable throughout October, despite the new restrictions introduced by Ontario and Quebec to control the spread of COVID-19:

-Across major industries, growth in incoming transactions to firms in several industries, including in the retail, manufacturing and finance, climbed briefly at the end of October due to the different timing of the Thanksgiving weekend in 2020 and 2019. Growth in payments in the wholesale and transportation industries remains negative.

-Growth in outgoing payments has been relatively stable between 10 and 12 per cent in October. Payroll deposit growth picked up slightly towards the end of October, while rent payments have been running flat relative to last year’s levels, with no sign of a turnaround yet. - Growth in consumer transactions, available through November 1st, picked up over the last week, as an unusually low total observed on one day last year made the y/y comparison temporarily more favourable:

-Growth in card spending in Ontario and Quebec continued to underperform the aggregate average in October, hampered by restrictions to contain the spread of COVID-19. Some restrictions are scheduled to be relaxed in the coming days in Ontario, likely boosting spending in the affected categories.

-Spending in sectors that are less dependent on social proximity, that benefited from pent-up demand, or from changing consumer preferences continues to outperform.

2. COVID-19 and the Canadian Economy: Scotiabank Transactions Data

- We present data on retail and non-retail transactions, which capture distinct but related aspects of economic activity in Canada.

- The data comprises actual observed daily transactions going through debit or credit card payment networks in the retail space, and automated funds transfers (AFTs) in the non-retail space.

-The transactions are anonymized and aggregated to protect the privacy of Scotiabank’s clients. - In the current circumstances, comparing the dollar volumes of transactions in the current year and in 2019 can be indicative of the depth of the decline in economic activity in Q2-2020 and help track growth through the re-opening phase.

-Note that the mapping from the volume of transactions to measures of economic activity (e.g. GDP) is imperfect, and so care must be taken when drawing the implications. - The AFT payments show bill payments to/from companies in Canada.

-Incoming payments can be associated with company revenue, and outgoing payments can be associated with costs. - Debit and credit card payments can be used to measure the evolution of retail spending at various types of establishments.

-The transactions can serve as a measure of economy-wide retail spending, and of the extent to which households are resuming pre-COVID levels of activity.

-Note that the use of electronic payments has increased because of COVID-19, so comparisons to year-ago levels can be misleading. These data are best used to observe directional movements rather than to make specific assessments on the level of activity.

2. COVID-19 and the Canadian Economy: Caveats

There are important caveats to analysis based on the payments data:

- The data is observed at daily frequency and embeds different types of seasonal patterns.

-For retail payments, the volume and types of payments are different depending on the day of the week and the season.

-For non-retail payments, both the day of the week and the season are important. In addition, some payments are tied to the calendar date (e.g. rent payments are made on the first day of each month), some payments have a bi-weekly schedule, etc.

-To smooth out most of the day-to-day seasonality we use a 14-day moving average of the dollar volume of transactions, taking a y/y% change to remove any remaining seasonal patterns related to the calendar date. - In addition to seasonality, there is normal payment volatility related to the random nature of the transactions process and the impact of regional and economy-wide events (weather, labour strikes, etc.).

-The volatility of this nature may or may not be related to economic activity as measured by GDP and so, as mentioned above, care must be taken in drawing inference. - For business transactions, which are inherently more lumpy compared to retail spending, data towards the end of the sample can be revised as some AFT payments are recorded with a lag. As a result we exclude the last few days of data of business transactions only.

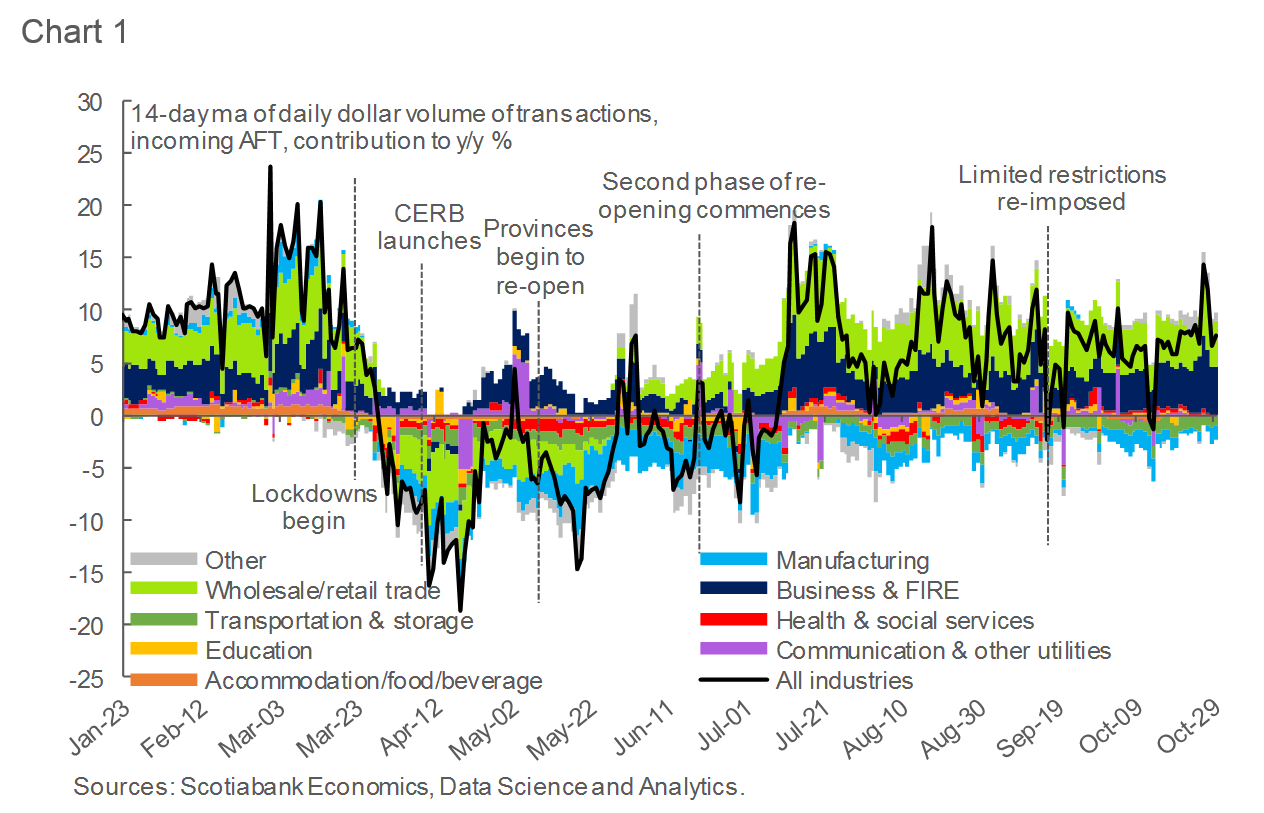

3. Business Transactions Data: Incoming Payments Stable Despite Restrictions

- Updated to October 29th, y/y growth of transactions in the business sector has been stable throughout October, despite new virus-related restrictions (Chart 1).

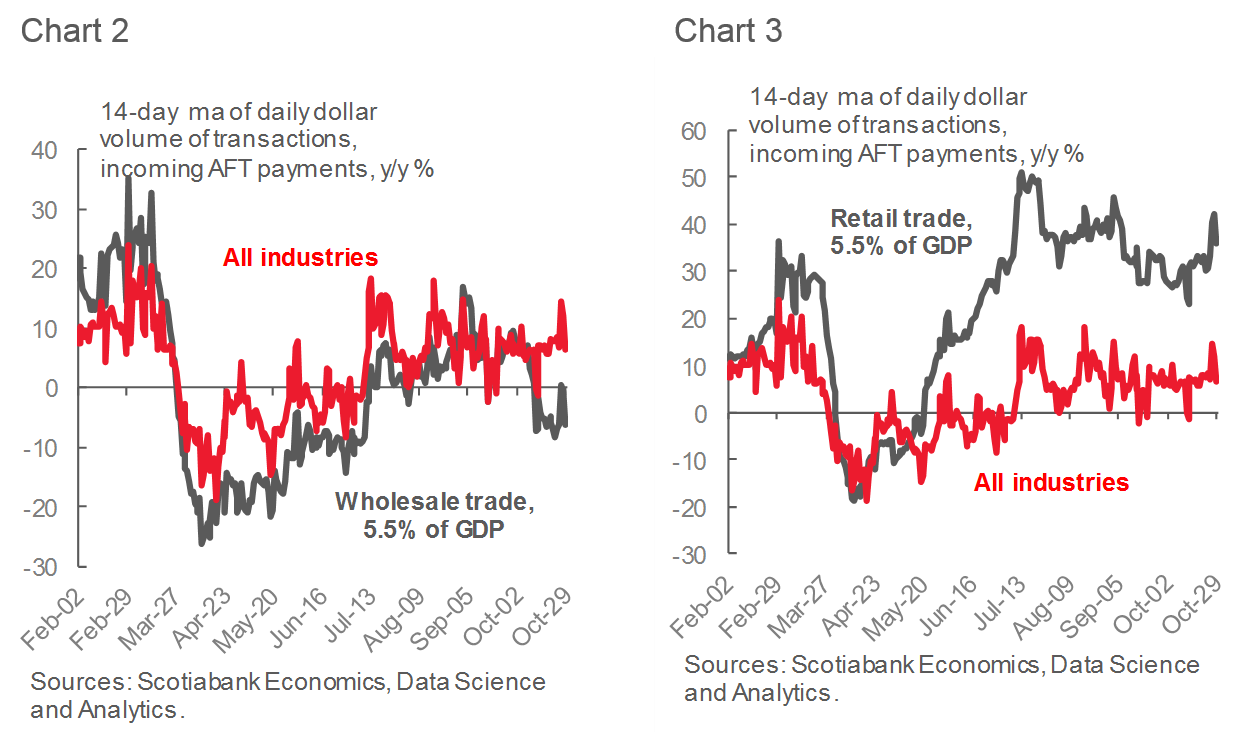

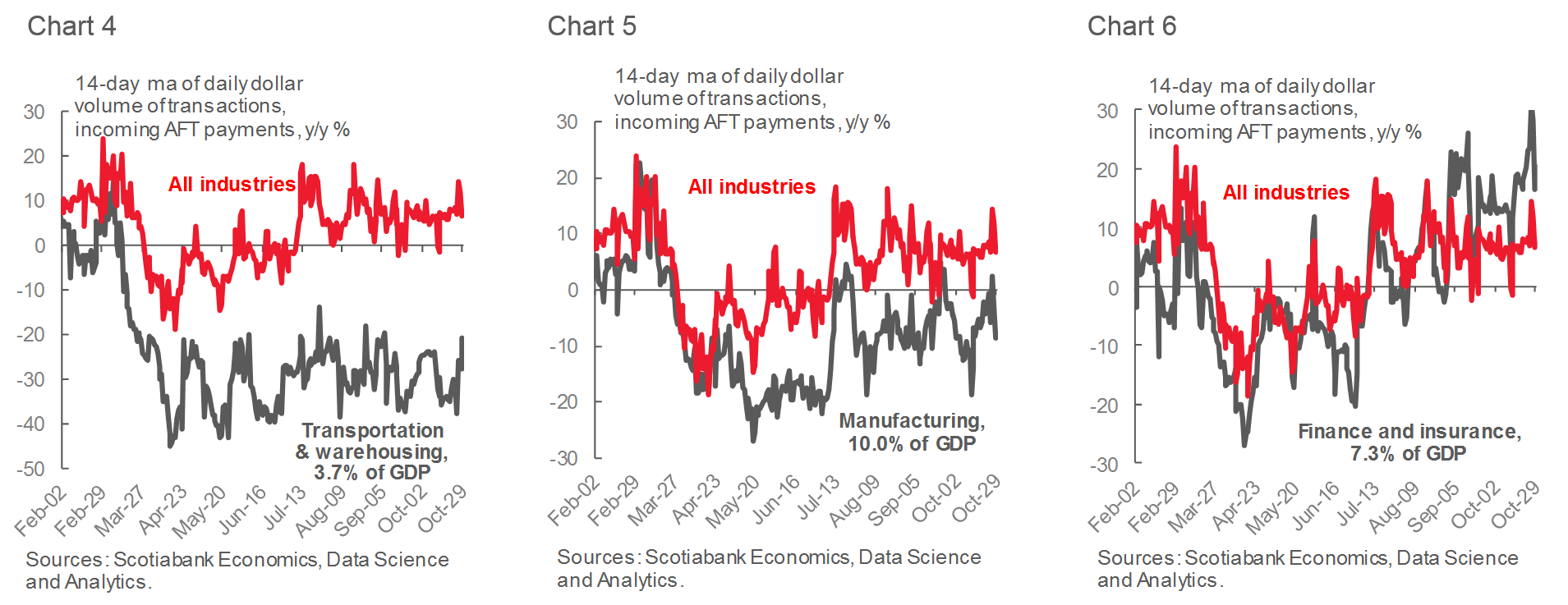

- Across industries, growth in incoming transactions to firms in several industries, including the retail, manufacturing and finance, climbed briefly due to the shifting date of the Thanksgiving weekend. Growth in payments in the wholesale and transportation industries remains negative (Charts 2-6).

- Automated Funds Transfers (AFT) are used for:

-rent and mortgage payments;

-payroll deposits; and

-other bills.

3. Business Transactions Data: Timing of Thanksgiving Leads to a Brief Spike in Growth

3. Business Transactions Data: Manufacturing/Transportation Still Below 2019 Levels

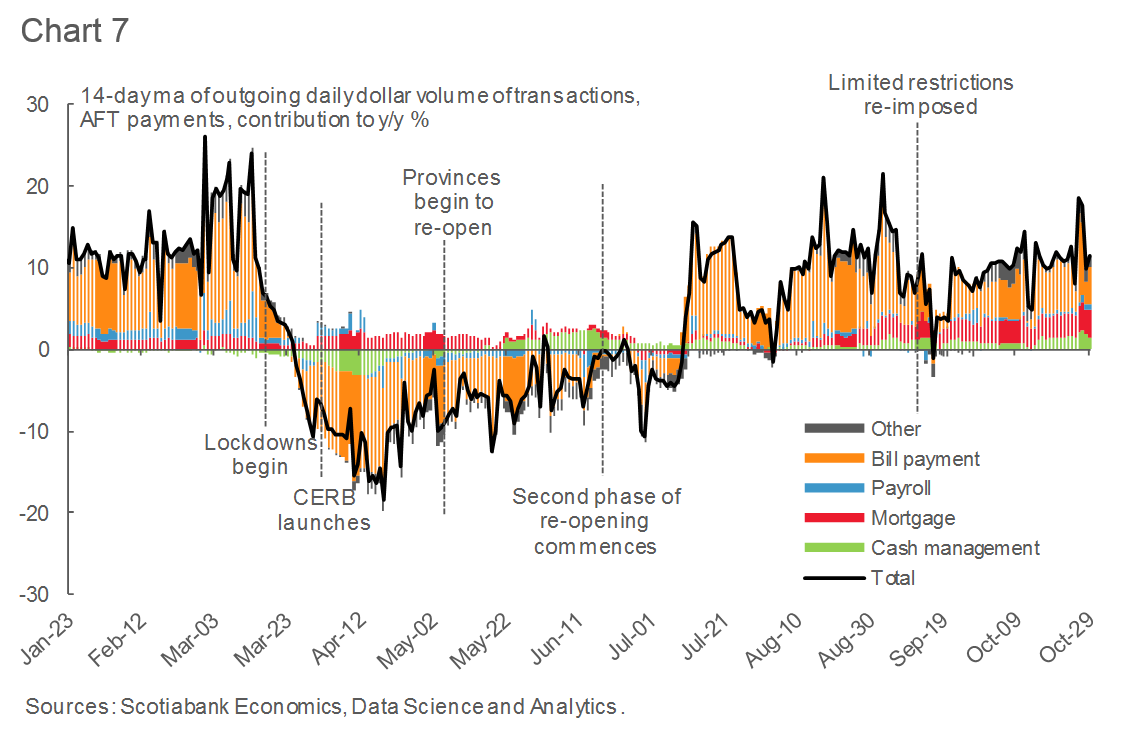

3. Business Transactions Data: Growth in Bill Payments Stable Over the Past Month

- Growth in outgoing payments has been relatively stable between 10 and 12 per cent in October (Chart 7).

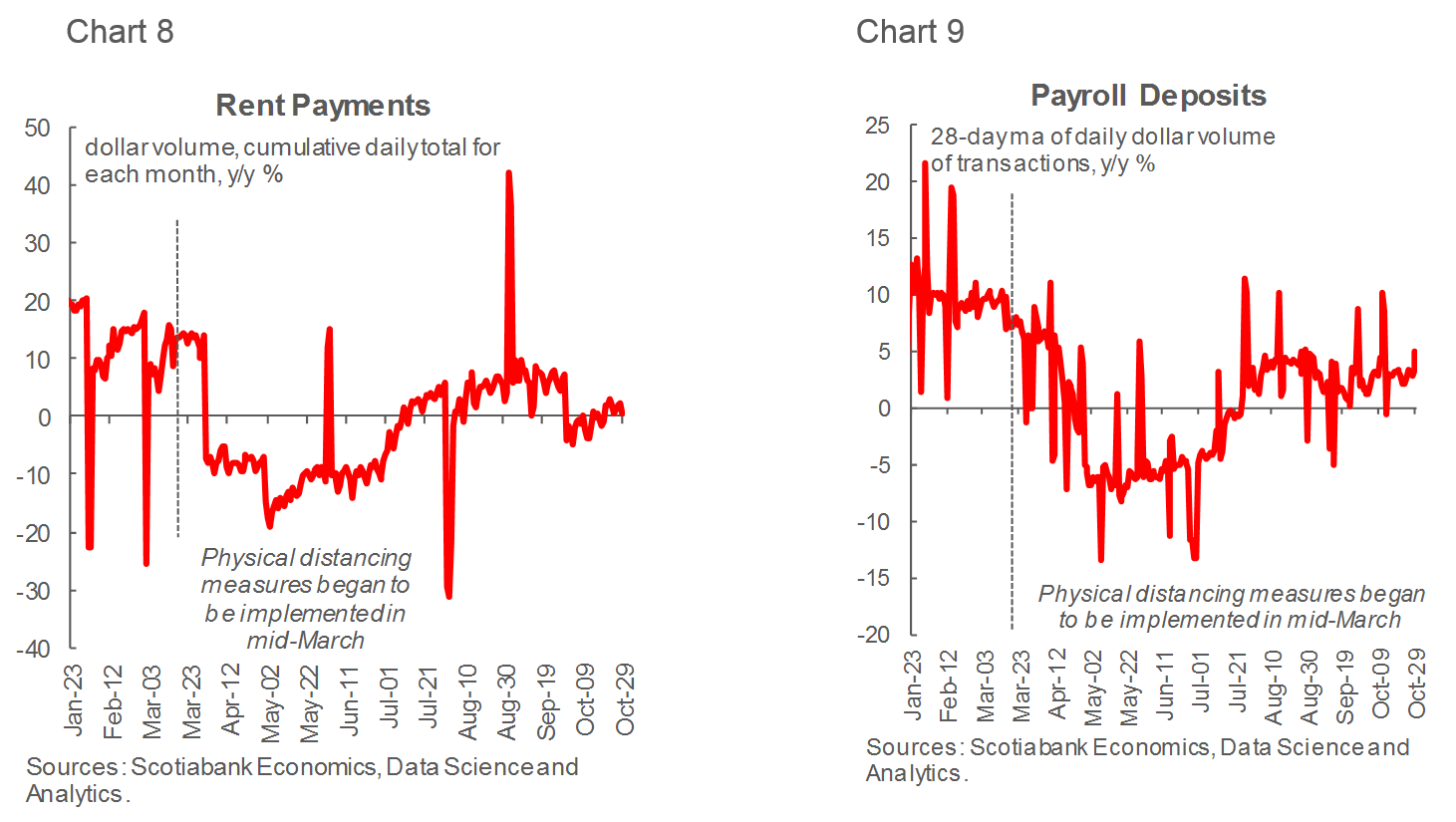

- Rent payments have been running flat relative to last year’s levels, with no sign of a turnaround yet (Chart 8). The bill to implement the Canada Emergency Rent Subsidy program, a replacement to the now-expired rent relief program, remains to be passed. If the legislation is approved, growth in rent payments will likely recover.

- Payroll deposit growth picked up slightly towards the end of October (Chart 9).

3. Business Transactions Data: Payroll Growth Picks Up, Rent Payments Weak

4. Retail Transactions Data: Unusually Weak Total in 2019 Boosts Growth Temporarily

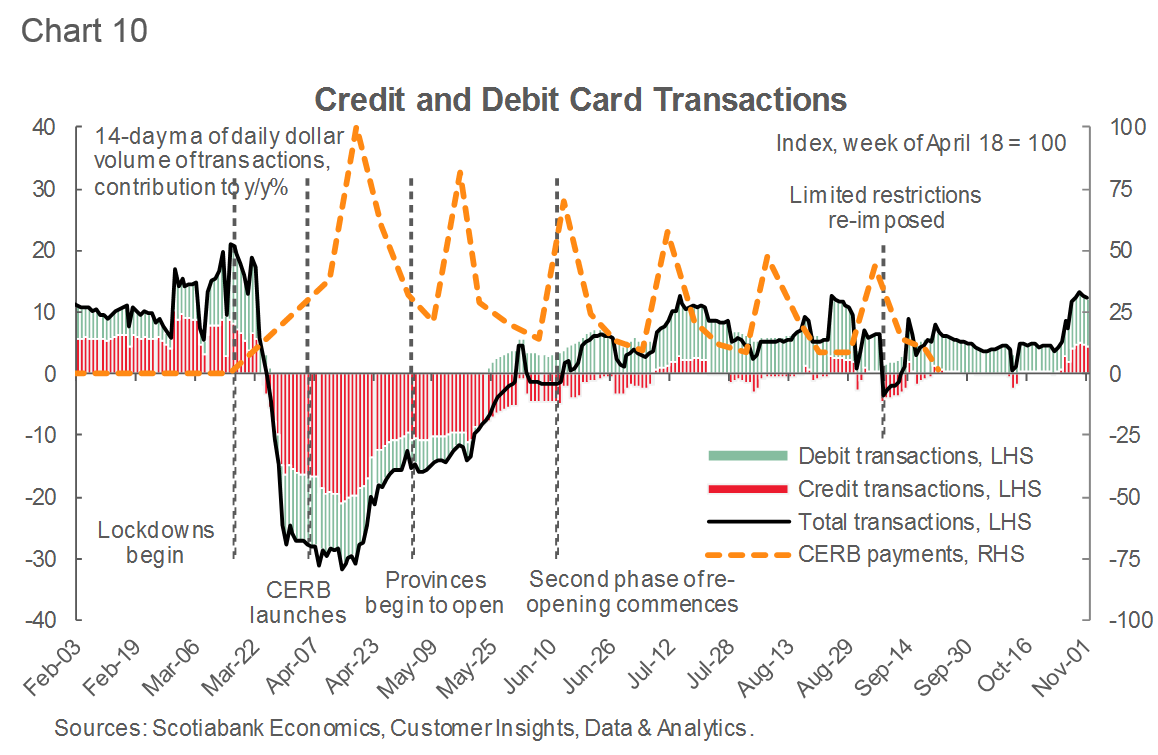

- Growth in consumer transactions, available through November 1st, picked up over the last week, as an unusually low total volume of transactions observed on one day at the end of October in 2019 made the y/y comparison temporarily more favourable (Chart 10):

-The boost to growth has already started to wane, with stronger 2019 transaction totals observed in late-October and early November bringing y/y growth to more normal levels.

4. Retail Transactions Data: Use of Bank Machines Down, Despite Temporary Boost

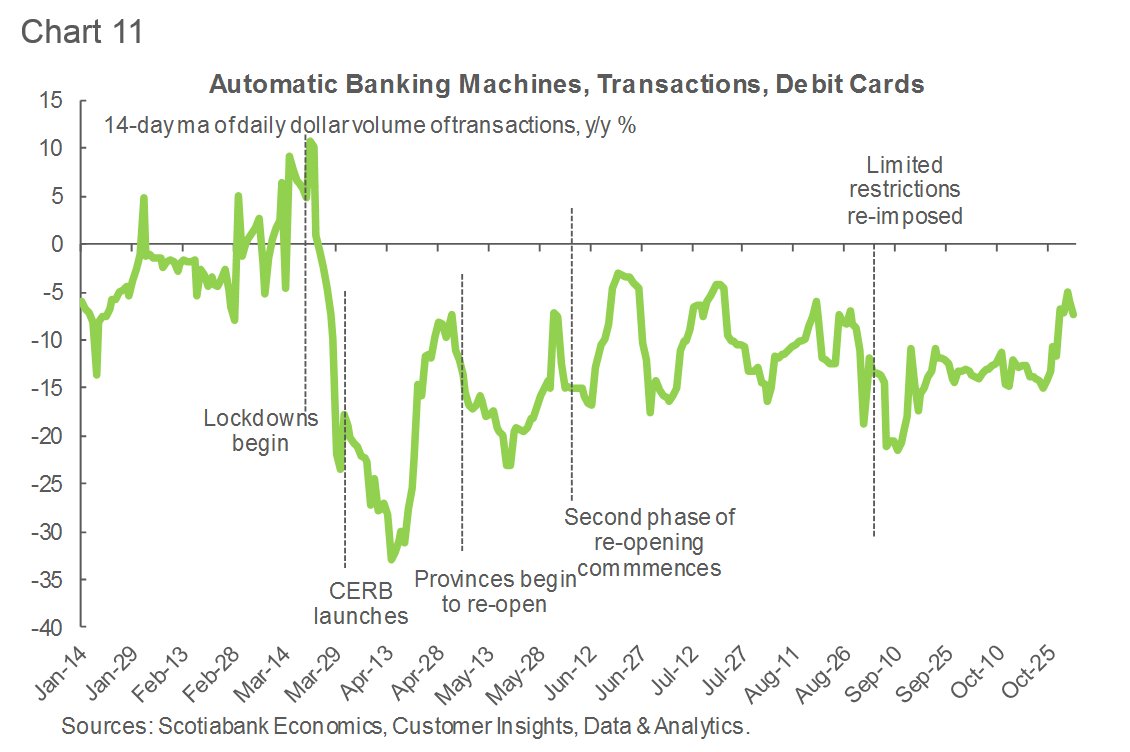

- The volume of debit card transactions through automatic banking machines (ABMs) continues to run significantly below the pre-pandemic levels (Chart 11).

- Public health-related restrictions on store operations, consumers spending more time at home, as well as a move away from cash by store owners, could explain lower levels of ABM usage.

4. Retail Transactions Data: Ontario, Quebec, Alberta and BC Underperform

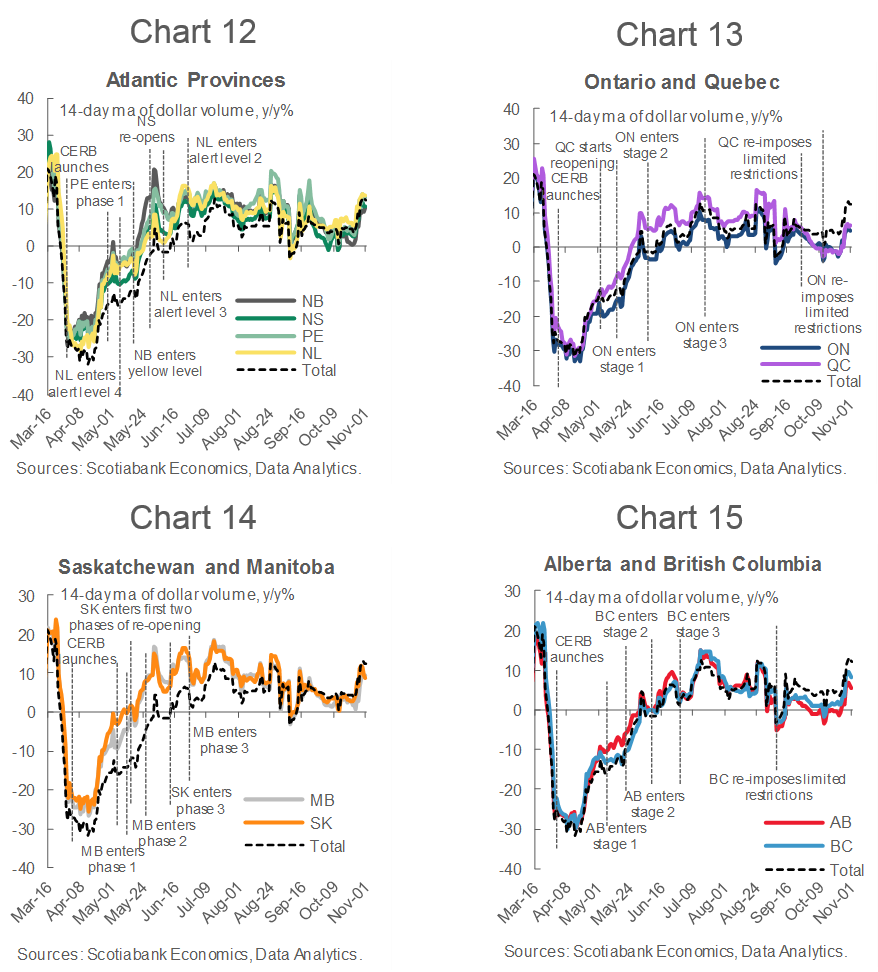

- Growth in the card transactions in Ontario and Quebec continued to underperform the aggregate average and most other provinces in October (Charts 12-15), as the re-introduction of restrictions to contain the spread of COVID-19 reduced spending at local restaurants and other businesses. Some of these restrictions are scheduled to be relaxed in the coming days in Ontario, likely boosting spending.

- Growth in card spending in Alberta and BC underperformed the average through September and October, in line with a worsening epidemiological situation in both provinces.

4. Retail Transactions Data: Growth in Card Spending Shows Lopsided Recovery

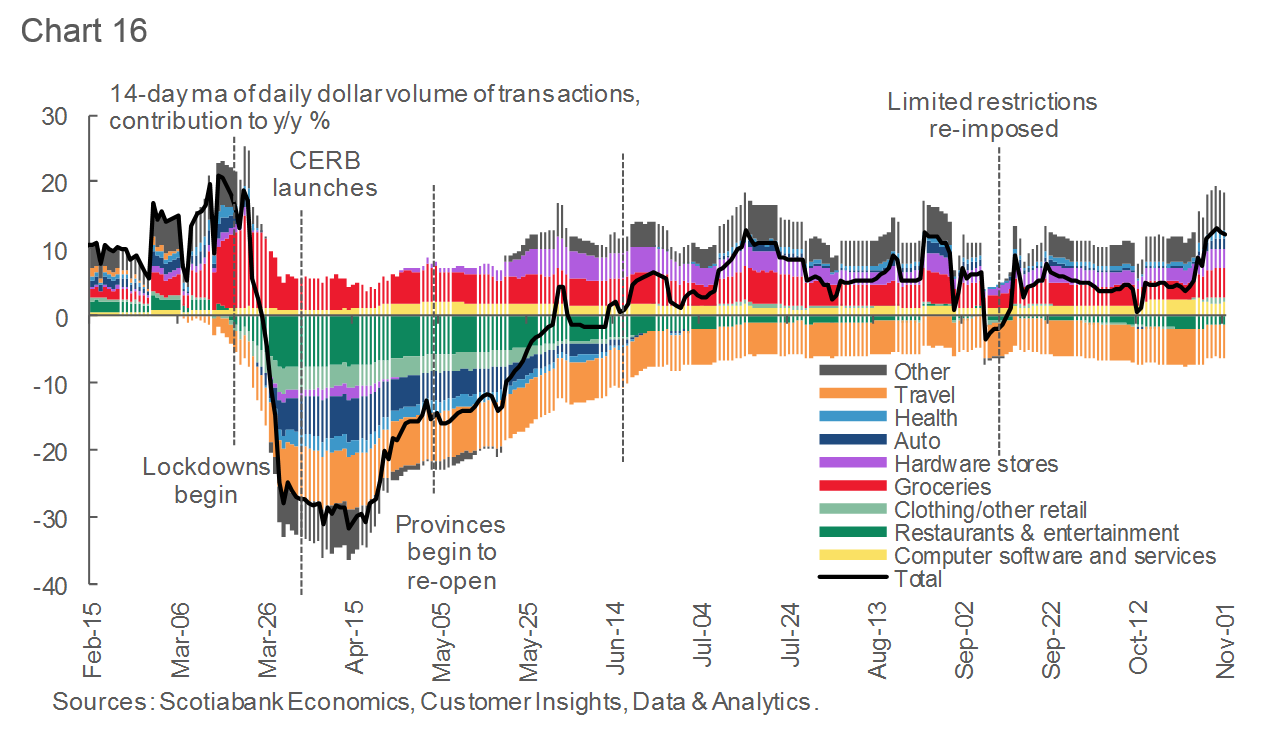

- Abstracting from temporary factors, growth in spending at various merchants highlights the lopsided nature of the recovery (Chart 16).

- Spending recovered faster in sectors that:

-Were less dependent on social proximity;

-Benefited from pent-up demand (clothing, automotive, home renovations);

-Enjoyed higher demand due to changing consumer preferences (e.g. shift to online work and entertainment).

4. Retail Transactions Data: Travel, Restaurants and Entertainment Remain Weak

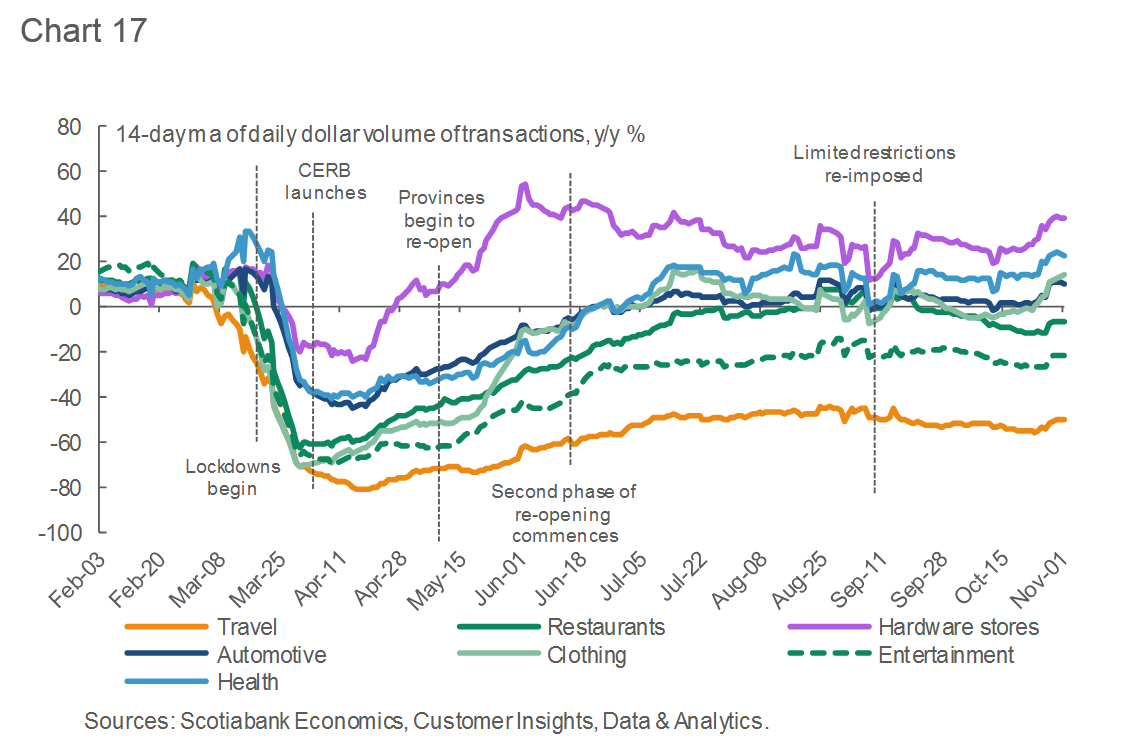

- Looking at categories that declined during the lockdowns in the spring, growth is again diverging, as spending on goods (e.g. items related to autos, clothing, hardware), as well as on essential services like health, remains strong (Chart 17).

- Those merchants that are most affected by the restrictions, as well as weaker demand as consumers remain cautious of social proximity (e.g. restaurants, entertainment and travel) see growth in spending weak and declining.

4. Retail Transactions Data: Software, Large Promotions Drive Spending Higher

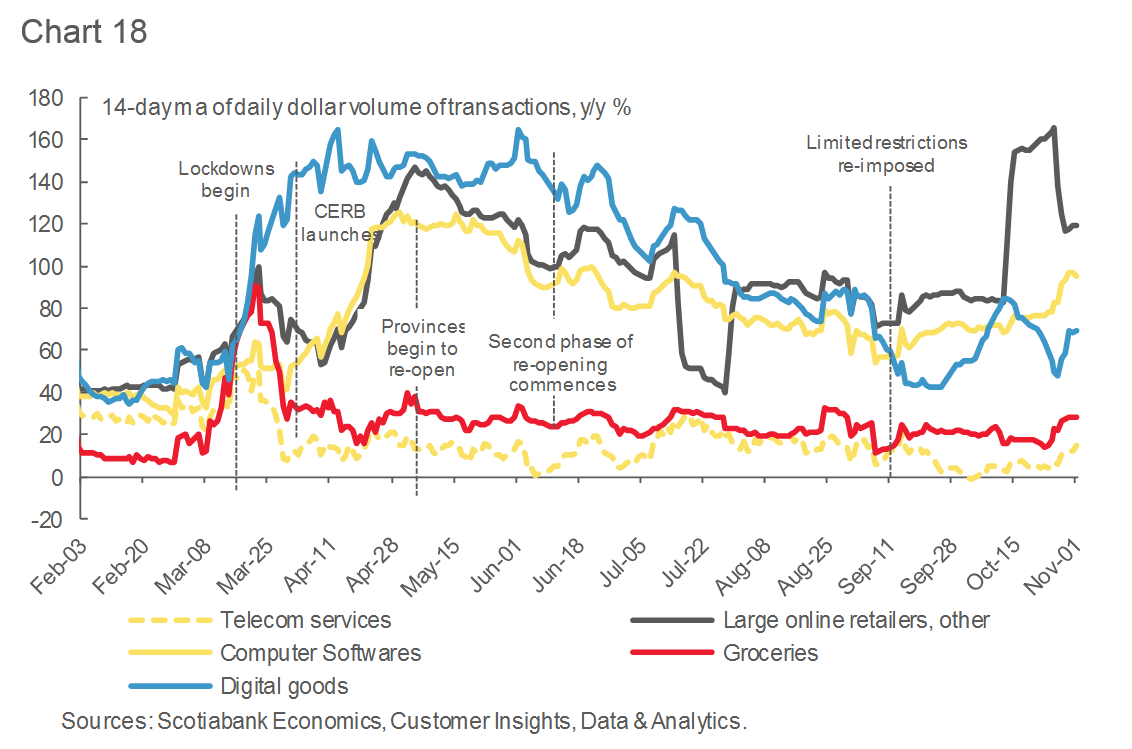

- Merchants that saw spending rise during the pandemic continue to see strong growth relative to last year (Chart 18).

- Strong demand for hardware and software required for outfitting a home office, or for home entertainment, continues to boost spending at merchants specializing in these items.

- Spending at digital retailers was boosted by Prime Days held by at Amazon on October 13-14.

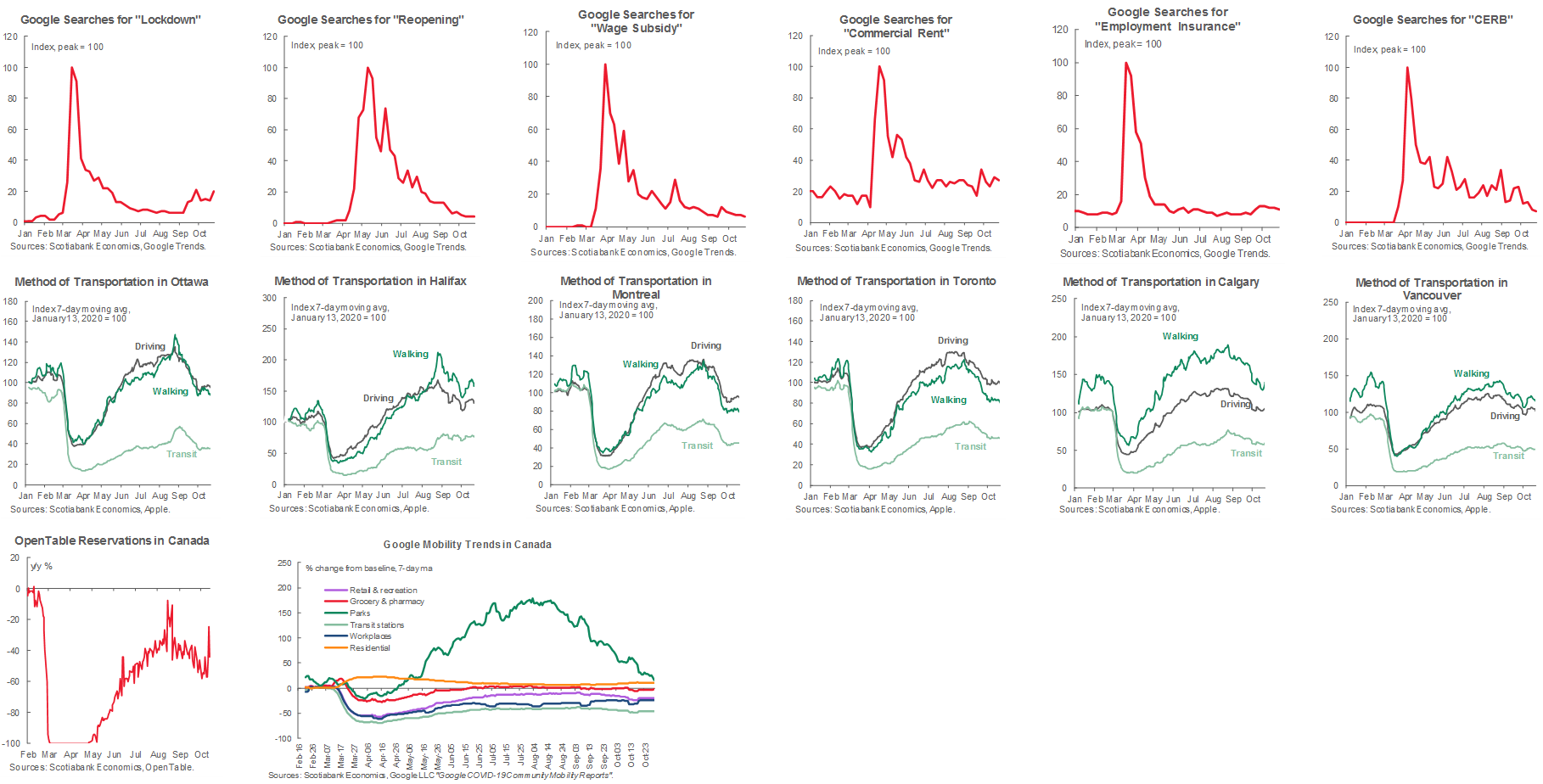

5. Other High-Frequency Indicators Of Activity

Charts 19-32 Google Searches, Various Keywords, Dining and Transportation Data

Nikita Perevalov* (Scotiabank Economics)

Taha Jaffer, Jason Liang (Data Science and Analytics)

Roland Merbis, Artur Motruk (Customer Insights & Analytics)

* Director of Economic Forecasting, 437.775.5137, nikita.perevalov@scotiabank.com

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.