ON DECK FOR TUESDAY, DECEMBER 21

KEY POINTS:

- Lighter holiday trading is magnifying sentiment swings across markets

- COVID-19 evidence drawn from daily London data…

- ...gives cause for tentative optimism against the waves of negativity

- Stale Canadian retail sales beat expectations…

- ...with strong October and November results that pre-dated omicron effects

Global markets are reversing yesterday’s omicron-driven market moves. Calendar-based risk is non-existent. Erratic moves through the holiday period should be viewed with skepticism given holiday-interrupted trading volumes that magnify the swings.

US stock futures are up by about 1% with Toronto up ¾%. European benchmarks are up by ~1%. Asian exchanges rose by between about ½% and as much as 2% in Tokyo. Sovereign bonds are cheaper with most curves bear steepening and driven by 4–8bps increases in 10 year yields. Shorter term 2 year yields are also higher across most markets but by less than 10s except in Canada post retail sales. The USD is very slightly weaker. Oil is up by about 1%.

STALE—BUT BETTER THAN EXPECTED—CANADIAN RETAIL SALES

The only calendar-based global development is Canadian retail sales that don’t even matter in the local market context given forward-looking uncertainties (8:30amET). The combined October reading and the better than expected initial flash print for November beat expectations all around. October’s gain landed at 1.6% which was higher than StatsCan’s initial 1.0% m/m guidance based upon a partial sample. The prior month’s 0.6% m/m drop was revised to be a little better at –0.3%. But the big surprise—to me at least—was another 1.2% m/m rise in the value of sales in November despite a sharp drop in auto sales and despite BC flooding effects over the back half of the month. This leaves us tracking about a 5% q/q annualized lift in retail sales volumes during Q4 so far after a 6% q/q annualized gain in Q3. This also confirms expectations for strong GDP growth during October (Thursday) and another likely gain for November given the gains in hours worked, retail sales and housing starts. Still, back to the point about being stale, this is data that is obviously pre-omicron in nature and so I get the flat initial response in CAD, notwithstanding that bonds reacted by cheapening the 2-year note to the tune of about 2bps or so. Stale data is a nice segue into assessing evolving forward-looking risks.

WHAT LONDON HOSPITALS ARE REVEALING ABOUT COVID-19 TRENDS

What matters far more to markets is the answer to this question: How bad is the omicron variant? The stock answer is that we don’t know yet, more studies are needed, they will take weeks to months to complete and so hang tight everyone. Put your lives on hold, hunker down, shut everything down until we have answers by, oh, maybe Springtime. Public health officials can’t wait for those studies versus embracing an approach that shoots first and asks questions later. I understand that to a point, given that the risk-reward dynamic to getting it wrong counsels implementing at least some cautious restrictions, but there should be a very, very high bar set against widespread lockdowns this time especially as the effects hit hard anyone not on guaranteed incomes in the health and government sectors. What I would be watching is daily data out of London that is a real world experiment that financial markets can learn from long before the formal studies come out. It’s a better backdrop for evaluating outcomes than, say, South Africa’s population that has a much higher share of immunocompromised individuals.

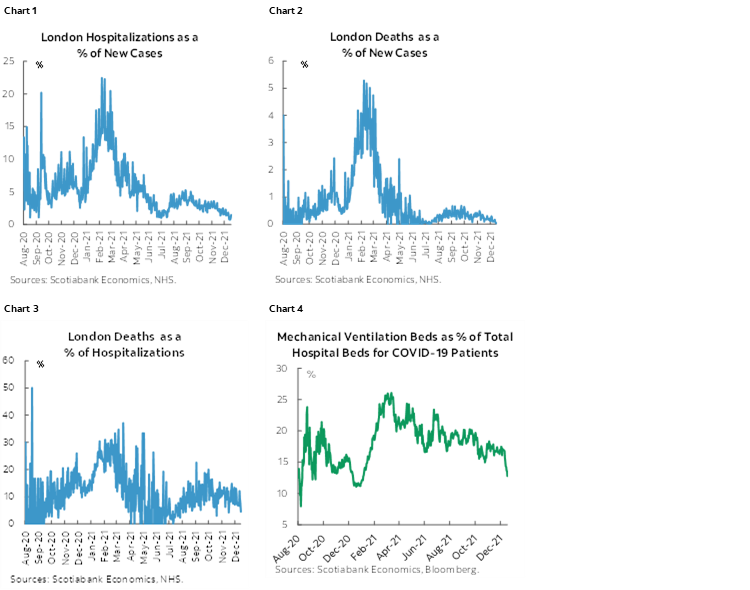

Here are some tentative observations drawn from London’s daily data:

- Chart 1 shows that hospitalizations are around a record low share of new daily cases. Over one-in-five cases were being hospitalized at the peak last February but now this share is hovering around 1%. We are about a month or so into the discovery of the new omicron variant and cases have been accelerating for 2–3 weeks. There are lags between testing positive and then becoming hospitalized and I’m sure plenty of data quality issues the world over, but we’re at the point now where it’s reasonable to be ask with greater attentiveness why we aren’t seeing a massive surge in hospital admissions.

- Chart 2 shows deaths as a percentage of new daily cases. The peak was just over 5% back in February and now it’s less than one-tenth of one percent of new cases. Obviously deaths lag everything else but the point is that even under the previously dominant delta variant the death rate had been plummeting for many months.

- Chart 3 shows deaths as a percent of hospitalizations which gives us an idea of the worst outcome for those that already have it badly enough to require hospitalization. At the peak in late February through early March this figure was over one-third and now it’s riding in the upper single digit percentages.

- Chart 4 shows the share of hospital admissions that are put on mechanical vents. At the peak last March that share was about one-in-four and today it is at about half that rate. One caution here is that there is a belief that too many patients were being put on vents in the past and this may have worsened their outcomes by forcing too much higher pressure oxygen into lungs and worsening inflammation. If true then doctors have perhaps developed a better understanding of appropriate treatment options for some.

Also, given evidence that one is probably well protected against omicron if you’ve either had COVID-19 and then been fully vaccinated or had three doses, it’s worth taking a look at super-immunity readings across the global population (chart 5). The UK actually tops the list with the biggest combined share of the population that has had it, been fully vaccinated and boosted. It’s a rough gauge since the categories are not additive in reality.

The advice that drops out of these observations isn’t exactly to rush off to your local shopping mall and start licking the handrails or to breath deeply sans mask at a COVID-19 testing site. You still don’t want to get any variant and need to be cautious, get vaccinated and boosted and follow proper precautions. The unvaccinated are still at high risk of paying a steep price for their choices. There are still many unknowns. The point, however, is that financial markets should continue to leave open the upside possibility that this might not turn out as badly as all the sour faced pundits on the evening news would have us believe. If omicron spreads much faster, infects a much bigger share of the population, has much less severe outcomes on balance and leaves behind much higher antibody protection across the general population, then perhaps this turns out to be a big leap forward in terms of immunity protections against future possible variants and case surges. That’s a big maybe, but listen to all sides of the potential outcomes.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.