ON DECK FOR THURSDAY, DECEMBER 23

KEY POINTS:

- Omicron optimism fueling light risk-on sentiment

- What number of Canadian omicron cases will yield prior hospitalization peaks?

- Stale Canadian GDP: strong October, November flash

- The last notable batch of US releases for 2021

Omicron optimism in the context of light holiday trading is driving a mild risk-on bias so far. There was no overnight calendar-based risk ahead of backward looking N.A. readings that will pretty much wrap up calendar-based risk for the year.

N.A. equity futures and European cash markets are up by ¼% – ½% for the most part. Sovereign bond yields are up again with 10s climbing by 2–9bps across major benchmarks. The USD is little changed with outsized movers including gains in sterling and the A$/NZ$. Oil is a couple of dimes higher.

Omicron developments are mixed. On the positive side are the three UK and South African studies that indicate the omicron variant is only 20% to one-third as likely to result in hospitalization compared to prior variants, plus evidence that South Africa’s cases are going down as rapidly as they went up plus evidence that AstraZeneca’s third booster shot raised antibodies against omicron. On the negative side is a study showing that a third dose of Sinovac’s CoronaVac vaccine does not raise antibodies to protect against omicron and that matters as it’s among the most widely used vaccines primarily in relatively poorer countries. Also, some point to Israel’s remarks that a fourth booster would soon be needed over coming months after the omicron wave as 3rd dose efficacy rapidly wanes; that’s a challenge to countries that are frankly doing a poor job at administering third shots (and offering testing) like Canada.

WHAT CASE NUMBERS MAY STRAIN CANADIAN HOSPITALS?

Given that the prime rationale for tightening restrictions is to help to avoid hospitals being overrun with cases, an important advance metric is the number of daily cases that may start to risk such an outcome. Chart 1 attempts to provide the answer: between about 20,000 and 32,000 cases per day. Once cases cross that number, hospitalizations could reach the prior record number of hospitalizations during the pandemic that was pressuring capacity at Canadian hospitals; above that new daily case number is uncharted territory for hospitals. Note that yesterday’s new cases tallied just shy of 15k which is getting close to this range and cases are rapidly rising such that we could be within this range very shortly and faced with record hospitalizations in the ensuing days with important caveats I’ll come back to.

This estimated range of new cases that would trigger new possible peaks for hospitalized cases is arrived at by considering that about 73% of all COVID-19 cases to date have wound up in the hospital, but studies out of the UK and South Africa (eg. here) indicate that Omicron is only tending to result in hospitalization rates equal to between 20% and one-third of the hospitalization rates of prior variants.

A big caveat is how significant the hospitalized cases may be. The UK study tended to indicate that once admitted to hospital, the outcomes for Omicron cases are similar to other variants. Real world evidence from South Africa tends to suggest mild hospitalization and treatment outcomes. Also note the point made earlier this week in this morning note about how usage of mechanical vents as a share of hospitalized cases in London has been sharply falling through much of the year for several reasons including a sense that vents might worsen outcomes for some patients by causing greater damage to lungs. Further, we have more effective treatments now and—in Canada—relatively high vaccination rates whereas the most vulnerable part of the population is still going to be the unvaccinated especially those who haven’t had a prior variant. The point is to provide a rough numerical range of daily cases that triggers greater concern and that reflects current research on Omicron hospitalization rates. The next key will be to monitor the severity of those admissions ranging from quick assessments before being sent home for self-isolation toward more severe outcomes. This key uncertainty should be much further informed by early in the new year.

US AND CANADIAN RELEASES

On tap is a wave of US and Canadian macro data this morning. Comments are kept brief given the stale nature of the reports in the context of forward-looking uncertainties. Yesterday’s US releases were also stale in that the modest on-line consumer confidence sample was significantly skewed toward just before the large run-up in COVID-19 cases, while nothing is more stale than existing home sales that reflect homebuying decisions at the point of contract signing 30–90 days prior to November’s figures.

1. Canada updates both the final estimate for October GDP and the flash estimate for November GDP (8:30amET). StatsCan had guided 0.8% m/m for October and then we got a strong number for hours worked which may suggest upside risk. November guidance will be more important; readings we can observed were strong, like retail flash guidance, hours worked and housing starts, but BC flooding effects will be among the downsides. The key is obviously how December holds up into Q1 amid what are so far light restrictions primarily applied to bars and restaurants plus how behaviour may adjust.

2. US personal income and spending both probably climbed by ~½% m/m in November (8:30amET). Spending will need a strong service sector performance to offset soft retail sales. Going forward, retail may overstate consumer strengths given a likely rotation of demand back toward goods and online shopping.

3. The Fed’s preferred inflation gauges (8:30amET) are likely to follow CPI higher at a somewhat gentler pace given methodological differences and the general pattern (chart 2).

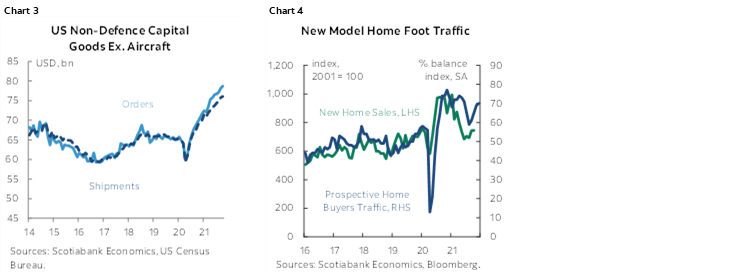

4. Watch US core durable goods orders (8:30amET) for continued momentum in demand for capital goods as shown in chart 3, and November’s new home sales (8:30amET) that are likely to follow measures like model home foot traffic higher (chart 4).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.