- On Sunday, May 7, the election of the Constitutional Council will take place, where between 50 and 52 councilors will be chosen under a mandatory voting system.

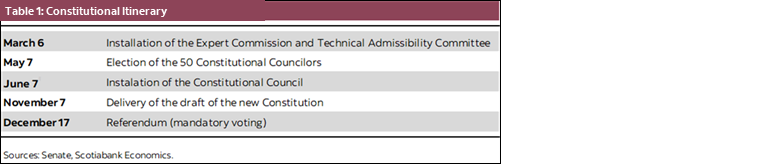

- The elected Council will begin its work on June 7, considering the final draft issued by the Commission of Experts. The political composition of the new constituent assembly is important since it is a collegiate body that will be able to adjust the proposal received from the Commission.

- We believe that financial markets will pay close attention precisely to the results of the vote. A result where the right-wing coalition obtains 23 or more councilors (that allows them to block proposals) could have favorable consequences for Chilean assets. Alternatively, a lower seat count would very likely lead to increases in political uncertainty, with repercussions for markets.

On Sunday, May 7, the election of the Constitutional Council will take place, where between 50 and 52 councilors will be chosen under a mandatory voting system. The election pacts, or lists, formed for this election are the following: (i) Partido de la Gente (center); (ii) Todo Por Chile (moderate left): PR, PPD and DC; (iii) Partido Republicano de Chile (extreme right); (iv) Unidad Para Chile (extreme left): Socialist, Communist and Government coalition; (v) Chile Seguro (moderated right): RN, UDI and Evopoli.

There are four regions that will elect 5 councilors each (Metropolitan, Valparaíso, El Maule, and La Araucanía), while six other regions will select 3 councilors and the remaining six regions will pick only 2 councilors. The election of councilors will have the same geographical distribution as the election of senators. We must note that currently the Senate has a balanced political composition with Chile Vamos and the Republican Party having 25 senators (50% of the Senate). Preliminarily, the Constitutional Council will have 50 members. However, there are reserved seats for Indigenous Peoples (2 in total), which will be used only if the Indigenous vote is higher than 3.5% of the total votes. On the other hand, if the votes are lower than 3.5% and higher than 1.5%, they will only be able to take 1 seat. In other words, the final composition of the Constitutional Council may be composed of a maximum of 52 councilors.

Although the general results will be known on Sunday, May 7, it is possible that the final composition will instead be known early on Monday, due to the adjustment that must be made to comply with the gender parity criterion required in the Constitutional Council.

The elected Council will begin its work on June 7, considering the final draft issued by the Commission of Experts. The Experts have been working since the beginning of March and are now in the process of deliberating to define the final draft of the new Constitution. In our view, the work of the Experts and, thus, the draft has sufficient boundaries without extreme proposals. However, although the proposal that the Commission would present would be moderate and market-friendly, we must remember that councilors elected this coming May 7 have the right to vote and the ability to modify or accept this proposal.

Political analysts anticipate a moderate composition of the Constitutional Council to result from the upcoming elections. Recent polls estimate that right-wing parties will obtain between 24 and 27 councilors, of which between 6 and 8 will come from the Republican party (extreme right). In addition, Indigenous Peoples seats were reduced from 17 to 2 in the current process that reduced the size of the Commission to 52 from 155—thus going from 11% to 4% of the total number of seats. Considering a total of 50-52 councilors to be elected and the recent polls, it is likely that there will be political moderation in the Constitutional Council.

The political composition of the new constituent assembly is relevant since it is a collegiate body that will be able to adjust the proposal received from the Commission of Experts. The quorum to approve the articles corresponds to 4/7, that is, the favorable vote of 30 directors is required (assuming a Council of 52 members). Symmetrically, if 23 councilors vote against a certain article, it cannot be part of the new constitution. Given the political tendencies of those participating in this election, if the right-wing parties (Chile Seguro + Republican Party) obtain 23 councilors, it is highly likely that all extreme proposals that affect property rights, state participation in currently private activities, among others that were present in the constitutional proposal rejected in September 2022, will not be part of this new constitutional proposal.

We believe that financial markets will pay close attention precisely to these party distribution results to adequately tabulate the risks and their probability of occurring. A result where the right-wing coalition obtains 23 or more councilors could have favorable consequences for Chilean assets. Alternatively, a result where right-wing parties do not achieve a blocking percentage (i.e. 23 seats) will very likely lead to increases in political uncertainty, penalizing the Chilean peso, interest rates, and the stock market.

It will also be important to examine the votes of the political lists and parties. Some polls suggest that the Republican Party could obtain a high percentage of votes, which would place it as the main political party in Chile, at least looking only at this election. This could have consequences for the structural reforms that the government wants to undertake. Alternatively, if the government list (Unidad para Chile) manages to maintain its historical share of the vote, it could improve its negotiating position in Congress to speed up the tax and pension reforms.

Finally, the exit referendum will take place on December 17 (see table 1 for key dates).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.