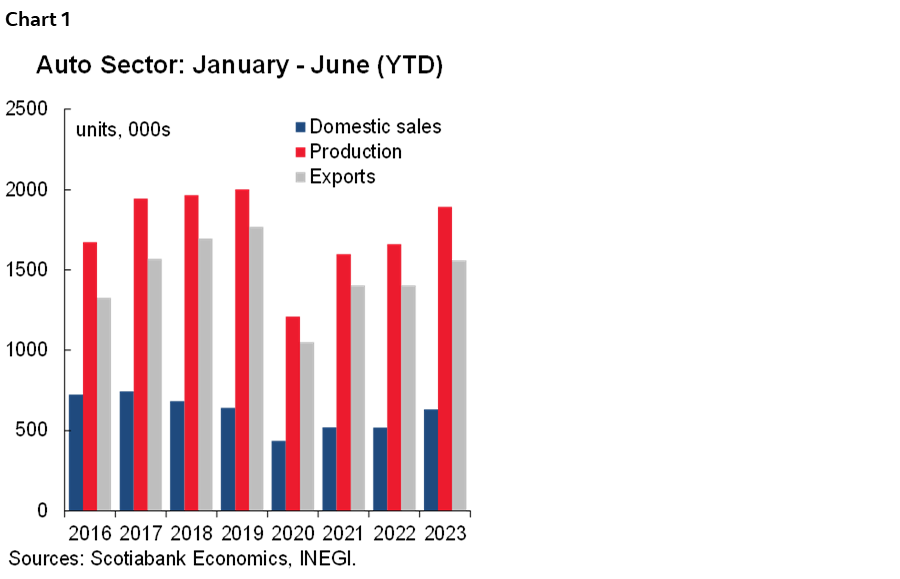

In the first half of 2023, the Mexican automotive sector continues showing signs of stabilization in supply chains even as production levels remain below its peak, in 2019, making significant gains also in domestic and foreign sales. At end-H1, the sector reflects still solid domestic demand, supported by a strong labour market, and increases in real wages. Additionally, production and exports have benefited from further stabilization in supply chains, although we see some risks ahead (chart 1 and table 1).

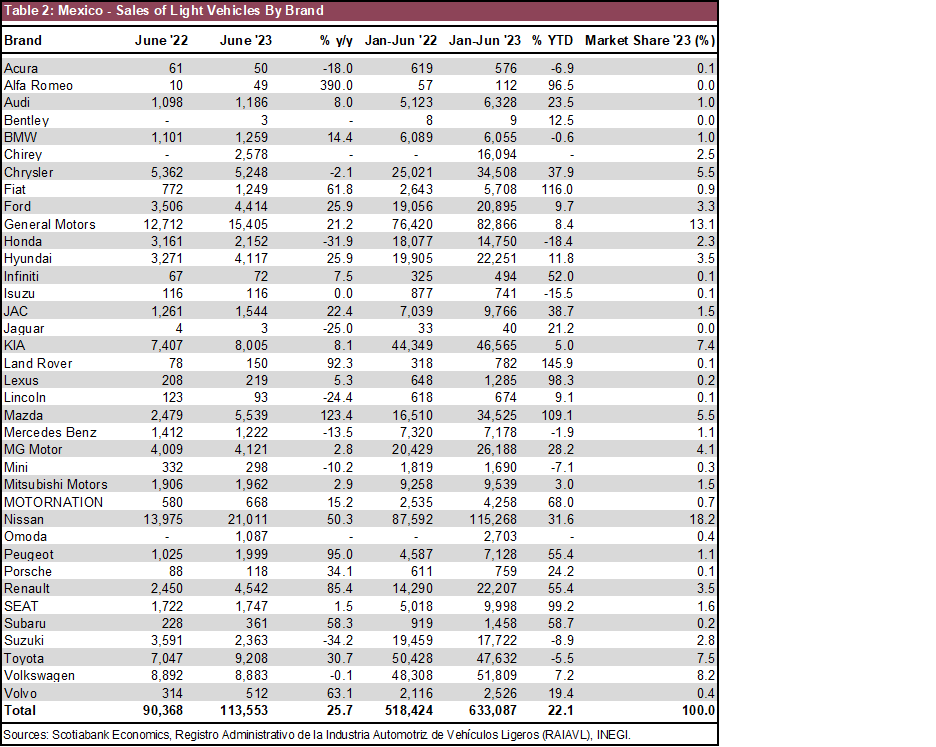

In June, domestic sales growth accelerated to 25.7% y/y, equivalent to 113.5k units sold. On a cumulative basis, domestic sales totaled 633k vehicles, equivalent to a 22.1% YTD increase. Nevertheless, H1 numbers show a -15.0% decline compared to the same period of 2017, which marked the strongest recorded first half of a calendar year. Within the details, we highlight the market share gains of new competitors in the year-to-date period from Chirey (2.5% share), JAC (1.5%) and Omoda (0.4%) brands, despite the fact that the largest participants, including Nissan (18.2%), General Motors (13.1%), Volkswagen (8.2%), Toyota (7.5%) and KIA (7.4%) retain over half of the market (see table 2 on page 3).

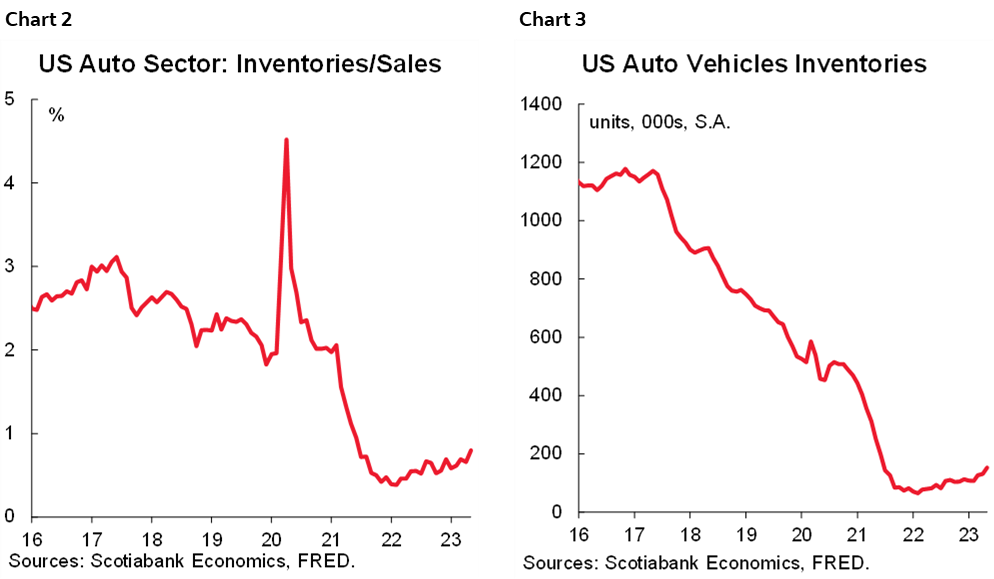

Exports of light vehicles showed annual gains of lesser magnitude than domestic sales. In June, exported units increased 20.5% y/y, to 286.3 k units. The cumulative numbers show the same story of growth in H1, as exports advanced 11.1% YTD in the January–June period, with 1.51mn units—though compared to 22.1% y/y increase in domestic sales. In comparison to its January–June peak in 2019, foreign sales remain -11.7% lower. In the United States, the largest destination for Mexican automotive exports, the ratio of sales to inventories remains close to but less than one car in inventory per sale. This implies that a significant percentage of sales are in backlog, suggesting persistent pressures in vehicle prices (chart 2 and chart 3)

On the supply side, light vehicles production decreased by -3.6% m/m in June, to 331.7 k units. However, the cumulative figure reached 1.892 million units, equivalent to a 13.9% YTD increase. Compared to its highest January–June numbers, production stands -5.4% below its highest level, in 2019.

Despite these results, we believe there are significant risks to production for the remainder of the year owing to the possibility of new scenarios of input shortages:

- We believe the recent news that China will limit its exports of metals used for chip manufacturing (mainly Gallium and Germanium, of which China is the largest producer), could limit the aggregate supply of inputs needed for the automotive industry.

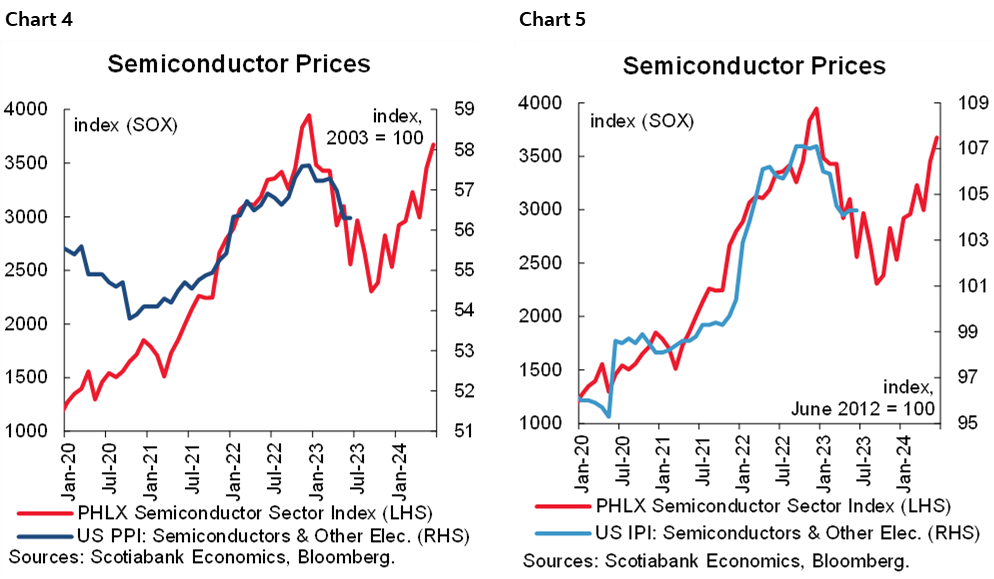

- The recent boom in AI technologies could divert the supply of microchips and semiconductors towards industries related to those recent developments (i.e. processors, computers, and electronics in general). In fact, the recent rise in the Philadelphia Stock Exchange Semiconductor Index suggests that demand for these types of inputs has increased in recent months. As noted in Derek Holt’s The Global Week Ahead, movements in U.S. producer prices and import prices for semiconductors appear to be moving in the same direction with twelve-month lag of the index, which reinforces our assumption of a recent increase in demand for inputs, which in turn may build cost pressures and new bottlenecks in light vehicle production (chart 4 and chart 5).

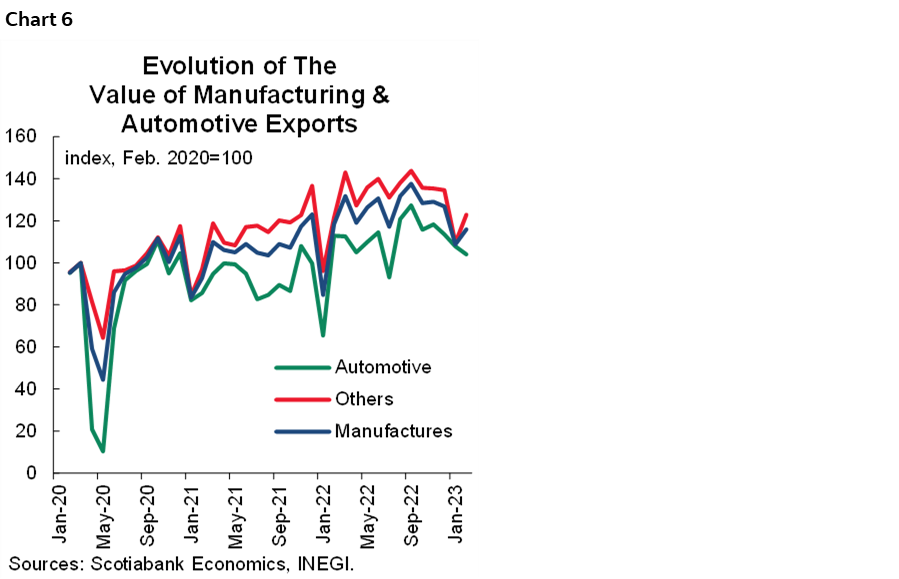

- One last risk to production, but no less relevant, is the expected slowdown in both the US and Mexican economies by the end of the year. Currently, initial signs of a slowdown in the economies, owing to the restrictiveness of policy rates, point to a slower pace in manufacturing (chart 6). However, we believe that supply has not yet caught up with demand despite the expected slowdown in the Mexican economy. In this regard, we believe that domestic sales will continue to be supported by a strong labour market. Proof of this is the entrance of new competitors that have been slowly gaining market share.

In the medium term, we see a more positive balance of risks, promoted by the positive Mexican growth outlook and optimism regarding nearshoring. In this sense, we highlight recent US efforts to reduce dependence on technological inputs from Asia, allocating large amounts to domestic investment. In this regard, despite the possibility of new bottlenecks, we believe that the worst is over for the Mexican automotive industry, and the medium-term outlook continues to be positive, towards its normalization.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.