- Chile: March inflation of 1.9% m/m above already-high expectations

- Mexico: Inflation rises in March

- Peru: BCRP raises rate to 4.50%, keeps hawkish stance

CHILE: MARCH INFLATION OF 1.9% M/M ABOVE ALREADY-HIGH EXPECTATIONS

March CPI surpasses even the highest projections and puts the central bank in check (again).

Before the release of the March inflation rate, surveys and financial markets anticipated a figure of no more than 1.2% m/m, while the central bank’s (BCCh) baseline scenario projected a rate of inflation of 1.1% m/m. In this respect, the 1.9% figure is a significant upside surprise. Accordingly, we expect the BCCh to cautiously evaluate the appropriate policy settings going forward, as it previously indicated that it was close to the terminal policy rate of this tightening cycle.

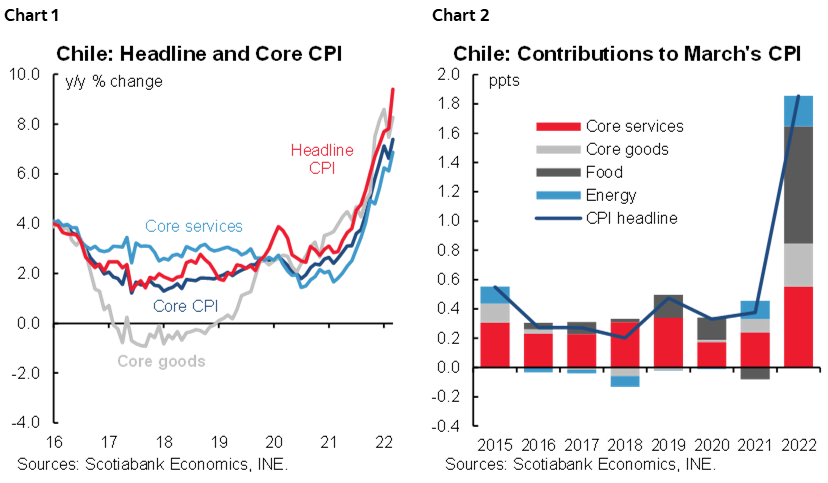

March inflation of 1.9% m/m (9.4% y/y) reflects a general increase in prices across volatile items, such as food and energy as well as at the core level (chart 1). In this regard, the diffusion of inflationary pressures (percentage of products with price rises) in the CPI reached 70%, its highest value since the current CPI basket was introduced (chart 2). Diffusion remains at the top of its historical range, both for the CPI core goods and services, at 62.3%% and 71.3% respectively.

However, analysis of the diffusion of CPI core goods and services does not reveal a deterioration relative to prior to the March CPI release. In general, a stabilization trend is emerging for goods prices, while services prices continue to display high diffusion—though this is explained in no small part by the relaxation of mobility restrictions in March.

A key question is what March inflation implies for the terminal monetary policy rate in this tightening cycle. In our view, the BCCh is likely to acknowledge the upside surprise in its May monetary policy meeting and consider two crucial aspects for monetary policy:

1. While the surprise to headline CPI level is 0.8 ppts above BCCh’s projection of 1.1%, excluding volatile components from the CPI (its preferred measure to assess inflation pressures) the surprise is 0.3 ppts given that the central bank incorporated an increase of 1.2% in its baseline scenario (versus 1.5% m/m actual).

2. As the March outcome may be a “one-off” surprise to its base scenario, mainly at the non-volatile level, it could be read as requiring a change in its forward guidance, rather than a need to move faster to the monetary policy rate indicated in the centre of its policy rate corridor, which would allow the BCCh to wait for more information to assess changes in forward guidance at the June meeting.

Accordingly, we are revising up our expectation of a rise in May from 25 bps to 50 bps. At the same time, the March Monetary Policy Report projection for annual inflation of 5.4% is now out of range, while our forecast of 6.6% is more likely. We retain this projection, anticipating a moderation of CPI inflation in April and May, since in our view the March figure was fueled by a set of specific rises that are unlikely to be repeated in the coming months.

On a political level, the March inflation outcome could impact the government. After revealing a USD 3.7 bn fiscal aid package yesterday with a focus on lower-income families and SMEs, financed with budget reallocations and without further sovereign debt issuance or affecting the fiscal deficit, voices are likely to emerge from Congress asking for additional aid. We believe that the government will be able to increase the size of the aid and take this fiscal package up to USD 4 bn. Financing additional expenses would require withdrawals from sovereign wealth funds (ESSF) and/or review of the spending spaces provided by the higher copper price within the fiscal rule (review the trend price of copper implicit in the fiscal rule).

—Jorge Selaive, Anibal Alarcón, & Waldo Riveras

MEXICO: INFLATION RISES IN MARCH

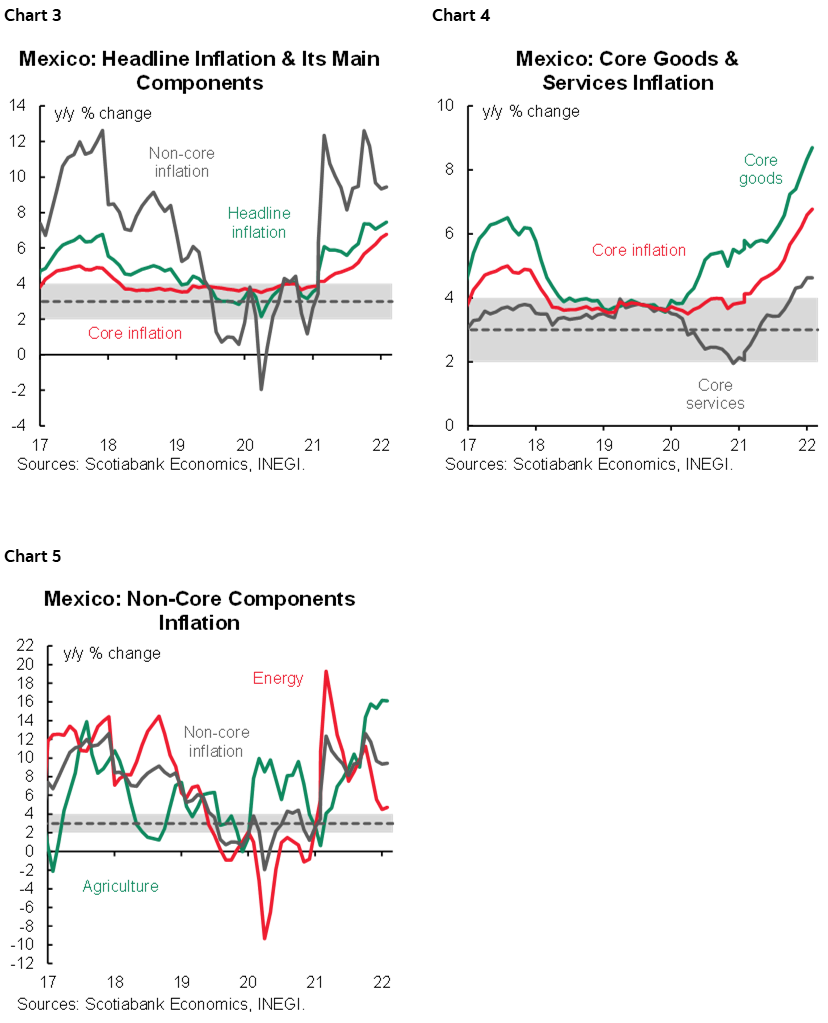

According to INEGI, headline inflation rose to 7.45% y/y in March, up from 7.28% previously, and above expectations (7.38%), to its highest level since 2001 (chart 3). Core inflation also exceeded expectations (6.71%), rising from 6.59% to 6.78% y/y, its highest level since 2001, sustaining the upward trajectory it has followed since March 2020 (chart 4). The increase in core was driven by an increase in merchandise from 8.34% to 8.69% y/y, while services stood at 4.62% y/y. The non-core component also accelerated, from 9.34% to 9.45% y/y, owing to an increase from 4.48% to 4.73% y/y in energy and regulated tariffs, despite a moderation in food from 16.17% to 16.12% y/y (chart 5).

On a month-over-month basis, inflation accelerated to 0.99% m/m from 0.83% m/m (0.92% consensus). Core inflation moderated from 0.76% to 0.72% m/m. However, non-core inflation came in at 1.79% m/m, up from 1.04% previously, with an increase in energy from 1.74% to 3.01%, and agriculture and livestock rising from 0.52% to 1.23%.

Furthermore, inflation expectations for the end of the year continue to deteriorate, as participants in the Citibanamex Survey now expect 5.99% headline inflation y/y, up from 5.88% previously. In this regard, it is worth noting the concerns raised by the Banxico’s Board in the minutes of the March meeting (link to minutes flash). As for the monetary policy implications, we maintain our outlook for a fourth rate hike of 50 basis points at the May monetary policy meeting. By the end of the year, we expect a rate of 8.25%, with upside risks of further rate hikes on a data driven approach.

—Miguel Saldaña

PERU: BCRP RAISES RATE TO 4.50%, KEEPS HAWKISH STANCE

The Board of Peru’s central bank (BCRP) raised its key interest rate by 50 bps to 4.50% on Thursday, April 7, in line with the market consensus (Bloomberg), the interest rate swap market, and Scotiabank’s forecast. The decision is consistent with the more aggressive stance that the BCRP has adopted since the beginning of the year and continues the normalization of monetary policy that began in August 2021. However, since the BCRP statement did not focus on economic activity and dispensed with conditional wording used in previous communications, such as “temporary” or “if necessary,” in our view, it has a more hawkish tone. After the decision, Peru’s monetary policy interest rate (4.50%) remains one of the lowest in the region.

Our forecast has the policy rate at 5.00% at the end of 2022 as presented in the Latam Weekly (March 18, 2022), consistent with our inflation forecast of 6.4% for the year. We maintain an upward bias given inflationary pressures are expected to remain.

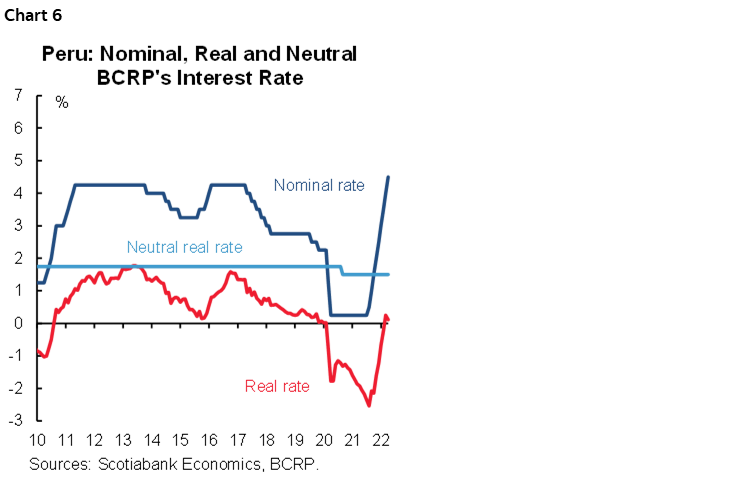

The BCRP statement expresses greater concern about inflationary pressures and cautions that inflation will take longer to reverse. It highlights the central bank’s concern over surging international energy and food prices, exacerbated by the Russian invasion of Ukraine, which have pushed inflation to 6.8% y/y in March. Reflecting these effects, 12-month inflation expectations rose significantly in March, from 3.75% to 4.39%, remaining above the inflation target range for the ninth consecutive month. The rise in inflation expectations exceeded the 50 bps hike in the reference nominal rate, so the real rate fell after five consecutive months of increases, declining from 0.25% to 0.11%. As a result, the monetary policy stance remains expansionary as it is below the 1.5% rate real neutral (chart 6). Year-on-year inflation should begin to decline in July, as base effects kick-in and factors on inflation, such as the FX rate and international prices of energy and commodities, unwind. The BCRP now expects inflation to return to the target in Q2–Q3 2023 in contrast to the March statement, which projected a reversal in Q1–Q2 2023.

Given the persistence of inflationary pressures, the BCRP reiterated that it will remain attentive to new information regarding inflation expectations and the evolution of economic activity, noting that it is prepared to consider additional measures to ensure inflation returns to the target range. The magnitude of future hikes will depend on the evolution of inflation expectations and economic growth. We also expect the BCRP to evaluate complementary measures in May, such as an additional increase in reserve requirements. In this regard, we also anticipate that the BCRP will continue to be comfortable with the trend PEN appreciation (7.1% YTD), which it considers necessary to offset inflationary pressures.

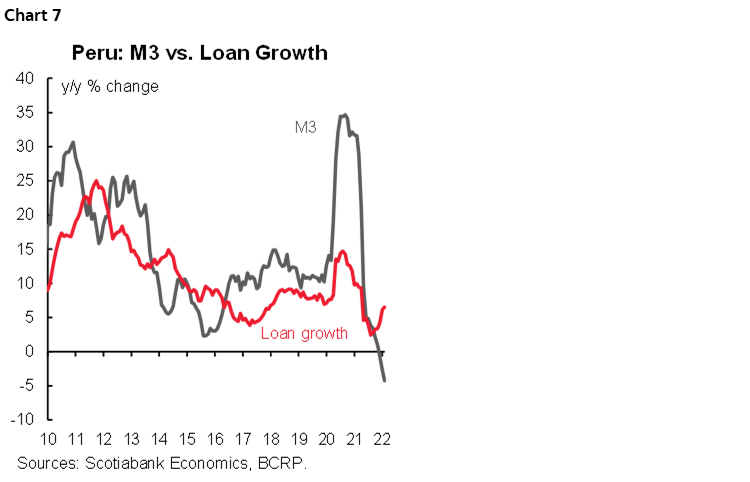

The quantity of money (M3) contracted -4.3% y/y in February, falling for the third consecutive month, as part of the monetary normalization process (chart 7). However, the growth of loans continued to expand, going from 6.2% y/y in January to 6.6% y/y in February.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.