- Colombia: Strong domestic demand leading to an acceleration in economic activity

COLOMBIA: STRONG DOMESTIC DEMAND LEADING TO AN ACCELERATION IN ECONOMIC ACTIVITY

I. Economic growth remains strong, explained by service sectors and strong domestic demand

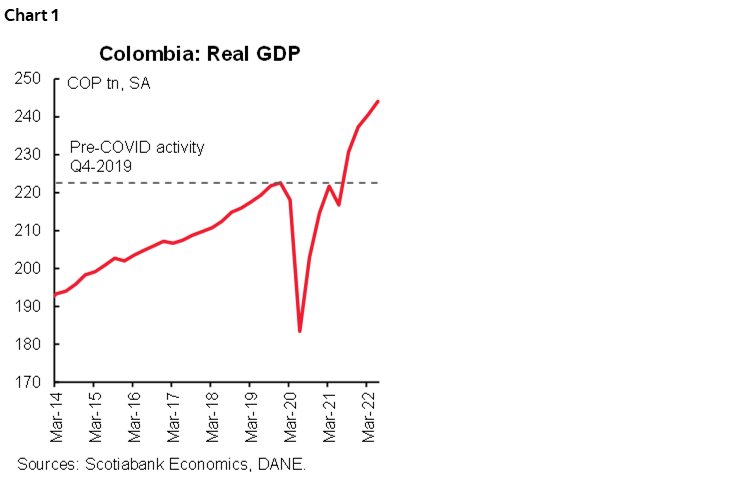

Data released on Tuesday, August 16 by Colombia’s statistical agency, DANE, shows that real GDP grew by 12.6% y/y in Q2-2022, above both the consensus (12% y/y according to Bloomberg) as well as our forecast of 11.7% y/y. Growth was +1.5% Q/Q in seasonally adjusted terms, with positive contributions from services-related sectors. At the end of Q2-2022, Colombia operated 9.7% above pre-pandemic levels (chart 1). It is worth noting that Q1-2022 GDP was also revised upwards from 8.5% to 8.6%.

The solid growth results reflect the economy’s positive response to the total relaxation of mobility restrictions, the return to in-personal activities, added to the realization of cultural, sports and religious events that benefited from favourable y/y dynamics owing to last year’s national strike. On the demand side, the trend of strong private consumption continued, while investment gained some steam, although it still showed some recovery to be seen, especially in civil works. That said, despite the high inflation environment that has implied a further tightening of the monetary policy rate, economic activity remained solid. Looking ahead, we expect consumption to slow down to more sustainable levels in the second half of 2022, while investment is expected to be stronger. For now, risks to our GDP growth forecast of 6.6% for 2022 are skewed to the upside.

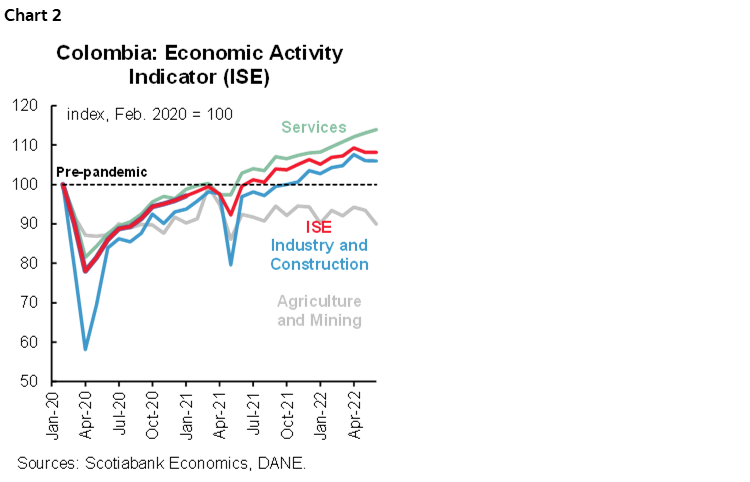

On a monthly basis, economic activity rose by 8.5% y/y in June and 0.04% m/m sa (chart 2). In June, the largest gains compared to a year ago came from commerce, transport and hotels (14% y/y), public administration, defense and health (6.6% y/y) and manufacturing industries (10.6% y/y). In seasonally adjusted monthly terms, trade and transport and hospitality accelerated, growing (+1.65% m/m sa); while on the negative side, construction (-3.3% m/m sa), mining (-4.9% m/m sa) registered the worst contractions.

Regarding the Q2-2022 performance from the supply side we highlight:

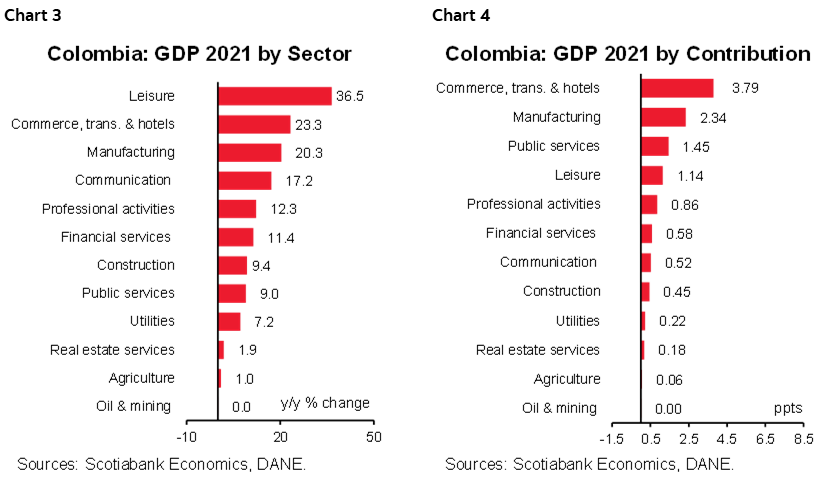

- The sectors that contributed the most to growth in the second quarter of the year were commerce, transport and hospitality (+3.8 ppts), manufacturing (2.34 ppts) and leisure (1.14 ppts), accounting for 60% of total growth.

- All sectors expanded during the second quarter of 2022 (chart 3), with the largest expansions coming from leisure (36.5% y/y), commerce, transport and hotels (+23.3% y/y, chart 4) and manufacturing (+20.3% y/y). The weakest performance during the quarter came from agriculture (1.0% y/y) and mining that did not present contributions to growth. This is explained by the decline in coal production due to the closure of some mines for maintenance during the period.

- The consolidation of normality, the return to in-person activities and the realization of more massive events are reflected in a positive dynamism of the sectors related to services. In seasonally adjusted, commerce activity showed a strong rebound (+1.45% q/q sa), however, on the downside, we are finding less dynamism in the agricultural sector due to higher costs of inputs, fertilizers and winter that have led to less dynamism in the sector, which has increased the risk of inflation in the future.

- The construction sector is also showing a better dynamic. In annual terms, the sector rose by 9.4% y/y but fell by 0.09% q/q sa in relation to the first quarter showed. This is explained by a drop in the construction of new building projects due to high input costs and higher interest rates. On the side of civil works, they have been recovering but at slower rates. That said, construction is expected to continue to show favorable levels and lead to growth so far this year.

Expenditure side GDP Q2-2022:

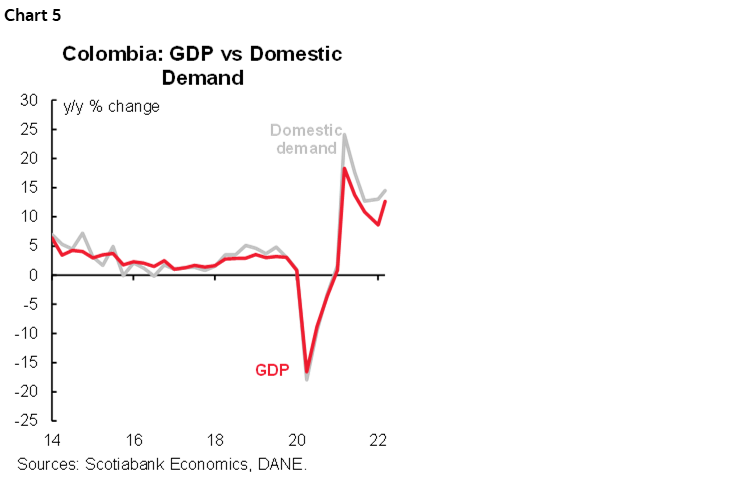

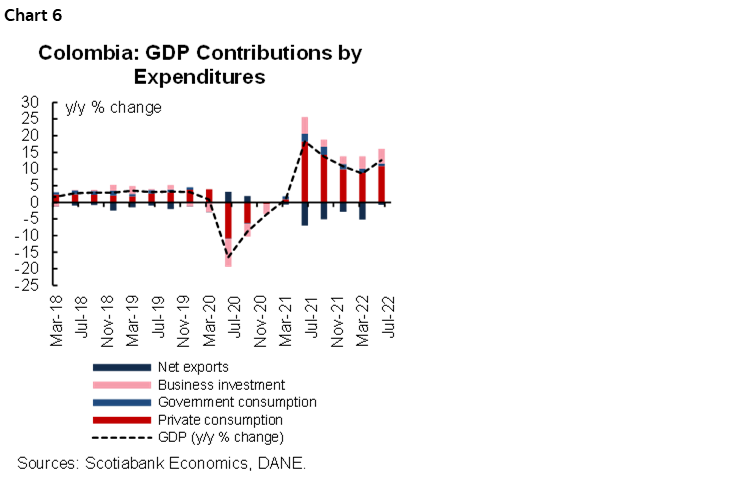

- Domestic demand increased by 14.5% y/y in Q2-2022 (chart 5), well above the total GDP expansion (12.6% y/y), pointing to a widening of the real external deficit. Sequentially, domestic demand expanded by 2.0% q/q sa. In this Q2-2022, we highlight that private consumption remained robust, and was also reflected in higher imports.

- Private consumption (+14.6% y/y) contributed the most to global growth (+10.9 bps) in Q2-2022 (chart 6). In seasonally adjusted quarterly terms, private consumption registered an increased (3.7% q/q sa), which is partly explained by Easter holiday season, mass events and the second VAT holiday in June. Public consumption increased by +4.4% y/y and expanded by 0.5% q/q sa, showing the effect of the election season. Private consumption growth should moderate to more sustainable rates in the second half of 2022, due to persistent inflation pressures and rate adjustments that imply an increase in the price of consumer credit. On the side of public spending, it would be expected to moderate due to the end of the presidential election season.

- Investment expanded by 9.6% y/y and contributed 1.7 bps to total growth, showing a positive performance in the purchases of machinery and equipment. On the other hand, activity fell by -0.3% q/q sa owing to a decline that housing construction and other buildings. We expect a better performance in the second half even though input prices remain high.

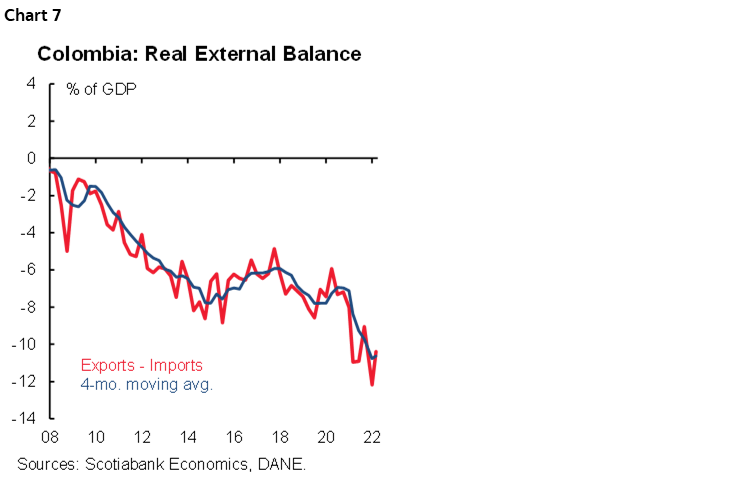

- The real external deficit widened in Q2-2022, which on average represented 10.4% of GDP (chart 7). Exports (+31.8% y/y) expanded at a slightly slower pace than imports (+32% y/y), showing the impact of weaker mining activity and high input costs while imports remain robust due to improved economic activity.

Strong economic activity and problematic inflation expectations support the expectation of an increase of at least 50 bps in the next two BanRep meetings. However, it is also worth noting that the possibility of seeing a more aggressive move by the central bank is also increasing. For now, we anticipate a terminal rate of 10% in the current growth cycle, but there is still a lot of uncertainty.

II. Imports and trade balance stabilized

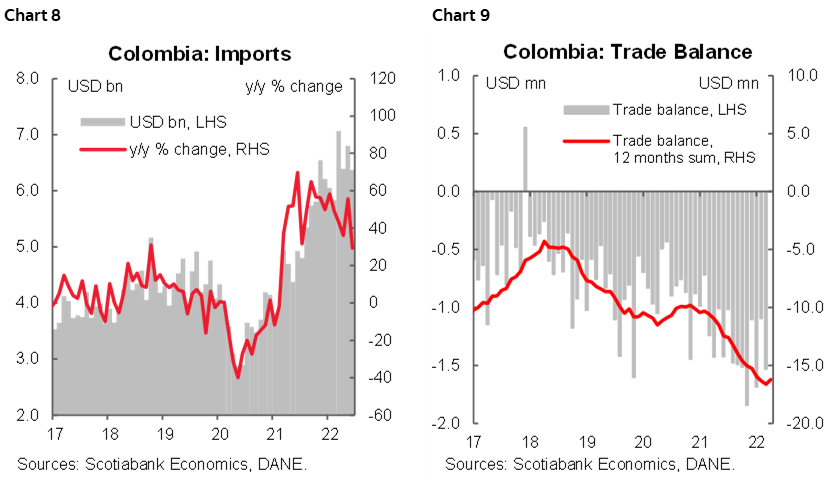

June’s imports data, released by DANE on Tuesday, August 16, came in at USD 6.37 bn (CIF terms), expanding by 29.4% y/y (chart 8), and moderating from the previous month’s figure (USD 6.81 bn). The monthly trade deficit stood at USD 333 mn (chart 9), lower than the June-2021 figure of USD 1.42 bn. The YTD trade deficit was USD 6.71 bn, 1.4% below the same period of 2021, showing that the deficit is stabilizing, as exports are reflecting the impulse of higher commodity prices, while imports reached a ceiling. Previous results affirm our expectation of a 5% of GDP current account deficit in 2022.

July’s purchases of transport equipment continued moderating, and fuel-related imports fell significantly (-41.3% m/m). The other relevant groups remained broadly unchanged. Manufacturing exports grew by 73.1% y/y accounting for the biggest positive contribution to annual imports growth, while agriculture-related imports increased by 16.4% y/y, and oil-related imports rose by 74.3% y/y, and now account for the more moderate contribution to the overall figure.

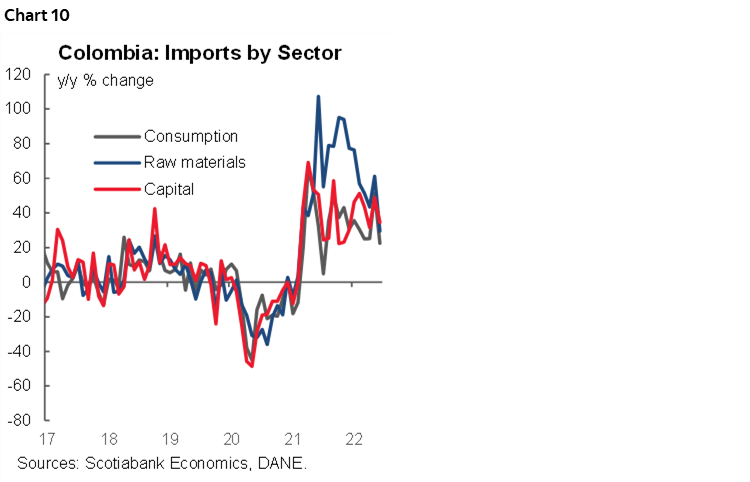

From the perspective of imports by use, the three major segments showed strong increases compared with June 2021 (chart 10):

- Consumption-goods imports increased by +22.4% y/y and stood at USD 6.37 bn. Both, durable and non-durable goods imports remained similar versus previous months. In y/y terms, they expanded by +8.48% y/y and +34.57% y/y respectively. In the case of non-durable goods, food purchases (+58.4% y/y) lead the gains again. In the case of durable goods, it is relevant to note that vehicle purchases contracted by 11.9%, likely as a result of international bottlenecks.

- Raw-materials imports grew by 29.5% y/y to USD 3.32 bn and remained the main contributor to the overall imports increase. Imports of raw materials for industry (+22.2% y/y) became the main contributor, especially due to higher purchases of food-related industries, which is a strong signal of the impact of higher international prices. Raw material imports for agriculture expanded by 27.5%, while fuel oil imports grew by 80.9% y/y, moderating its expansion.

- Capital-goods imports were up by 34.4% y/y to USD 1.81 bn. Purchases of investment-related goods in the industry lead the gains (+34.7% y/y), especially due to purchases of industrial machinery. Transport equipment (+34.6% y/y) is accelerating, which is still a positive sign of economic recovery.

All in all, imports in June are pointing to a stabilization at high levels. In monthly terms, oil-related imports contracted, but investment-related purchases remained strong showing that the economic activity is still robust. The trade deficit also stabilized showing that imports reached a ceiling, while exports are still strongly supported by high commodity prices, but also by non-traditional exports.

We expect the current account deficit would stand around USD 17 bn equivalent to 5% of GDP in 2022. In terms of financing, the prevalence of high capital goods imports points to better FDI. However, we highlight that the external deficit remains one of the main issues of concern in Colombia’s macroeconomic metrics, which would impede the FX to appreciate significantly in the medium-term.

—Sergio Olarte, Maria (Tatiana) Mejía & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.