- Chile: President appoints new central bank governor; GDP forecast revised up

- Mexico: Consumer confidence has a lower-than-expected start to the year, recording its second consecutive decline

CHILE: PRESIDENT APPOINTS NEW CENTRAL BANK GOVERNOR; GDP FORECAST REVISED UP

I. President Piñera appointed Rosanna Costa as new Governor of the Central Bank

On Thursday, February 3, President Piñera appointed Rosanna Costa (64) as Governor of the Central Bank, who becomes the first woman to head the BCCh, to a five-year term, to replace Mario Marcel who was appointed Finance Minister by President-elect Gabriel Boric. The appointment, which was announced through a press release, does not require consultation with the Senate. Ms. Costa (right-wing sensibility) held the position of National Budget Director at the Ministry of Finance between 2010 and 2013, in Piñera’s first administration. She has been a board member of the central bank since January 2017.

At the same time, the Board of the Central Bank appointed Pablo García (51) as Vice-President of the Central Bank with a term ending in January 2024 to replace Joaquín Vial, whose tenure as a board member is ending. Mr. García (close to Party for Democracy), has been on the central bank’s board since January 2014.

II. Ministry of Finance revised upward its GDP growth forecast for 2022

On Friday, February 4, the Ministry of Finance (MoF) released its Public Finance quarterly report, corresponding to the fourth quarter of 2021. A key change relative to the last report was the upward revision in the GDP forecast for 2022, which increased from 2.5% in September to 3.5%. According to the MoF, the main drivers behind the projected economic growth this year will be: the robust external impulse and positive terms of trade; the high liquidity in the pockets of households and the Universal Guaranteed Pension; the improvement of the labour market; and the growth of the public investment, which will increase 14.3%. Scotiabank Economics also projects GDP growth of 3.5% this year.

For 2022, the MoF is projecting a structural fiscal deficit of 2.8% of GDP (compared to 3.9% of GDP in the September projection) and an increase in public debt from 37.5% of GDP to 38.6%. In addition, the MoF announced the injection of USD 4 bn to the Economic and Social Stabilization Fund (FEES) in January, which closed 2021 with USD 2.5 bn and with the injection now totals USD 6.5 bn. The MoF also projected positive fiscal slack to 2026. This is another important highlight, one that will influence the fiscal commitment that the new government makes to converge to a structural balance. It should be noted in this regard that, according to the Fiscal Responsibility Law, the new government will have 90 days to define the path of convergence to fiscal balance following its inauguration on March 11.

—Jorge Selaive, Anibal Alarcón, & Waldo Riveras

MEXICO: CONSUMER CONFIDENCE HAS A LOWER-THAN-EXPECTED START TO THE YEAR, RECORDING ITS SECOND CONSECUTIVE DECLINE

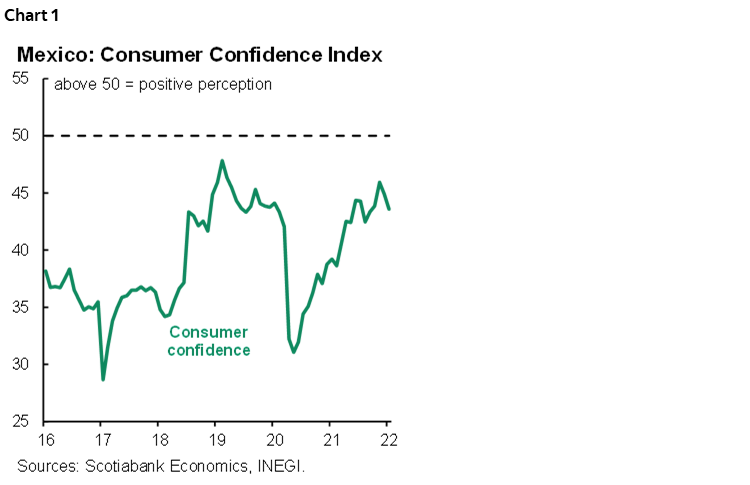

Consumer confidence for January came in below market expectations at 43.4 (43.8 expected) and recorded its second consecutive decline (chart 1). The indicator registered generalized retreats across all its components. It is worth highlighting the decline of 1.8 in the indicator related to the country’s current economic condition and the 1.3 fall in the index of current household members’ purchasing power. Household future economic condition, which is the only indicator in positive territory, at 56.3, registered a monthly drop of 0.6.

Consumer confidence has been hit by a decrease in purchasing power from high inflation and the increase in the number of new omicron variant infections. However, there has been an improvement in consumer confidence from the 2021 average, with the general index 4.4 points higher. In the short term, the main obstacle for private consumption recovery is inflation.

—Luisa Valle & Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.