- Chile: Monthly GDP (Imacec) expanded 7.2% y/y in March (+1.6% m/m)

- Colombia: Mixed messages from the labour market

CHILE: MONTHLY GDP (IMACEC) EXPANDED 7.2% Y/Y IN MARCH (+1.6% M/M)

Temporary factors and genuine stabilization behind the recovery in economic activity.

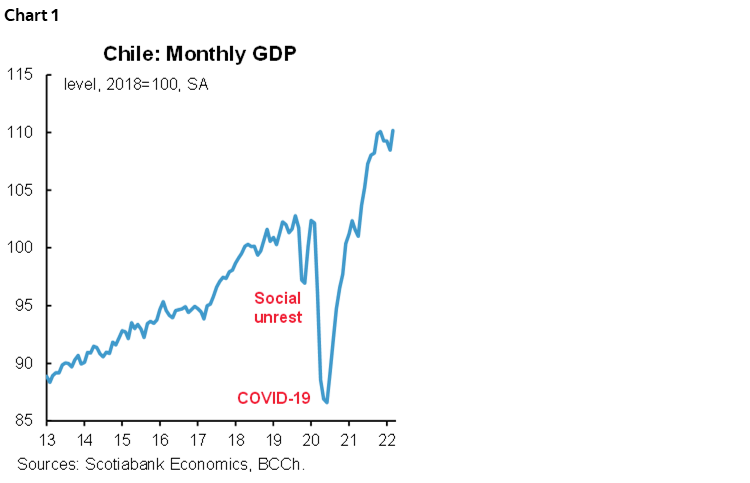

On Monday, May 2, the central bank (BCCh) released data on monthly GDP for March, which expanded 7.2% y/y, above market expectations (Bloomberg: 6.2%) and in line with Scotiabank’s estimate (7.0%). Imacec grew 1.6% m/m (seasonal adjusted), recouping part of the contraction in economic activity observed since December (chart 1), largely owing to faster growth of services and a stabilization in goods production.

Temporary factors linked to the reopening and increased mobility, which we expected, were behind a surprising seasonally adjusted monthly recovery in all economic sectors. Even trade, which has slowed since late 2021, showed indications of stabilizing. While it is too early to say that the economy has returned to its long-term growth trend, there are signs that point in that direction.

In this respect, the quarterly contraction of 0.4% q/q reflects convergence towards trend levels of GDP. However, it also raises the risk of a moderate technical recession should Q2-2022 likewise reveal negative q/q growth. A technical recession would be consistent with our base case scenario, in which the second half of the year is crucial to our higher-than-consensus estimate of annual GDP growth in 2022 of 3%. Risks to our projection include external factors linked to the global slowdown as well as local factors coming from heightened political uncertainty.

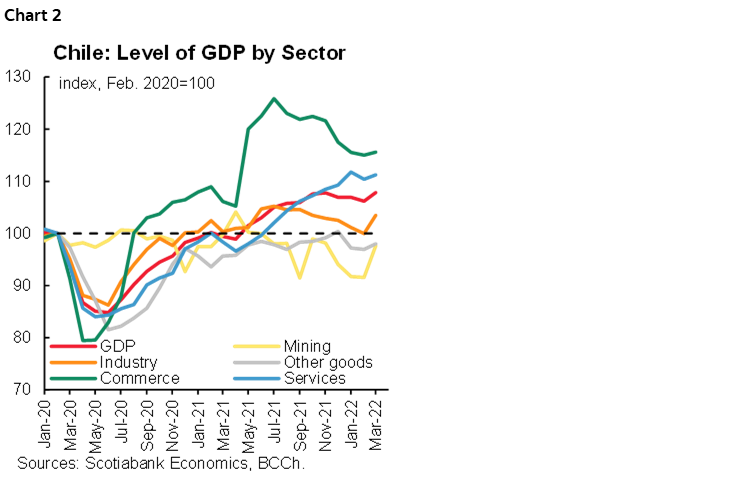

All economic sectors expanded m/m in March, with the contribution of mining and services standing out (chart 2). Mining increased 6.6% m/m, recovering part of the drop in recent months. Despite this performance, prospects for the sector for the balance of the year are limited, given the persistent drop in grades and the drought, which affects production. Services grew 0.7% m/m, supported by personal and business services. As a whole, we estimate that the services sectors will sustain GDP growth this year, mainly thanks to the dynamism projected for investment.

Against these developments, the BBCh’s scenario for 2022 GDP growth of 1.6% is coming under scrutiny, although the external scenario continues to be a challenge for the coming months. In the March Monetary Policy Report, GDP growth of 7.5% y/y was projected for the Q1-2022, compared to the upside surprise of 0.4 ppts with the 7.9% y/y growth for the quarter reported today. However, the international scenario looks worse than just a few months ago and is likely to dampen GDP expectations.

—Jorge Selaive, Anibal Alarcón, & Waldo Riveras

COLOMBIA: MIXED MESSAGES FROM THE LABOUR MARKET

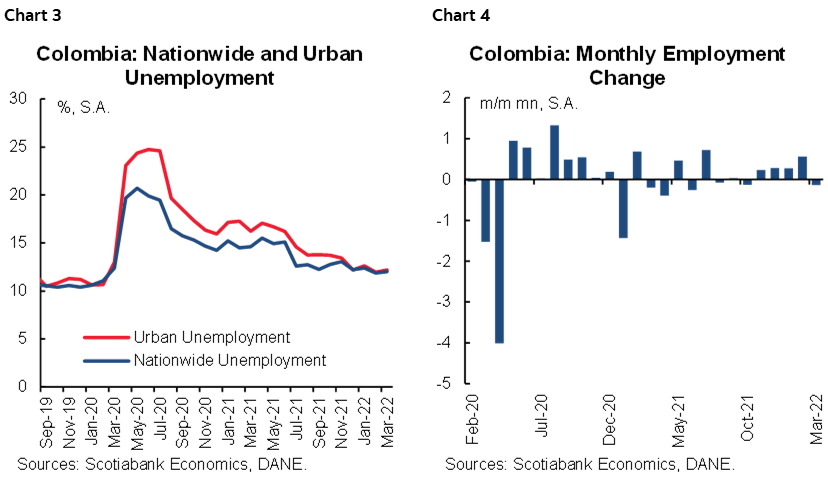

Employment data for March, released on Friday, April 29, show that in-person activities are contributing to job creation compared to one year ago, especially for the female population, though total employment remains 2.2% below pre-pandemic levels, while inactivity is 18.6% above pre-COVID-19.

The nationwide unemployment rate stood at 12.1%, while the rate of urban unemployment (main 13 cities) was 12.6%. Both indicators are lower than March 2021 levels of 14.7% and 16.6%, respectively. The services sector remained the main source of employment gains, especially for women. Job creation is also concentrated in the formal sector, which is absorbing people with technical and professional skills. Despite the gains in employment, there is still a gap relative to pre-pandemic levels.

In seasonally-adjusted terms, the unemployment rate stood at 12.0% nationally and 12.2% in urban areas, both increasing from the previous month’s levels of 11.9% and 12%, respectively (chart 3). In fact, employment contracted by 132 thousand jobs in March (chart 4).

Four sectors accounted for 78% of the 1.59 million y/y increase in employment in the year to March: manufacturing (+466 thousand), education, health, and public sector (+304 thousand), transport and logistics (+264 thousand), and restaurants & hotels (+208 thousand). On the negative side, employment in the construction sector contracted (-199 thousand).

In terms of job quality, informal jobs accounted for 45.5% of national employment, below the March 2021 level of 47.9%, and in urban areas informal jobs fell from 46.8% one year ago to 44.3% in March 2022. It is worth noting that formal jobs contributed 75% of the job gains in March, which explains better employment dynamics for skilled workers.

We also saw further improvements in terms of the gender gap. In February, male unemployment stood at 9.6% (as compared to 11.8% in March 2021), while female unemployment stood at 15.6% (19%). Two out of three new jobs were filled by women, consistent with the trend in terms of the female labour force participation rate. This shows the clear effect of the return of in-person activities, especially schooling, which has allowed women return to the labour market.

Summing up, March’s unemployment rate improved compared with one year ago, reflecting the effects of reopening. However, total employment continues to be 2% below pre-pandemic levels, which together with informality remain key labour market challenges.

—Sergio Olarte, Maria Mejía, & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.